Could a Bitcoin Collapse Trigger the Next Financial Crisis? The Answer Is Scarier Than ‘Yes’ or ‘No’

Share

Key Takeaways

A Bitcoin crash can spill into broader markets, especially tech and high-risk assets.

Leverage magnifies losses, making downturns far more dangerous for investors.

Stablecoins are not risk-free, and major de-pegs can disrupt crypto liquidity.

Diversification and trustworthy platforms remain essential for managing crypto exposure.

The question is everywhere: If Bitcoin suddenly crashes, could it actually unleash the next global financial crisis?

ChatGPT’s answer: It’s more complicated, and more worrying, than a simple yes or no.

ChatGPT’s response to Bitcoin causing financial crisis.

Below is a clear breakdown of how big Bitcoin really is, where the real risks hide, and why the next crisis might have a crypto fingerprint even if Bitcoin isn’t the main culprit.

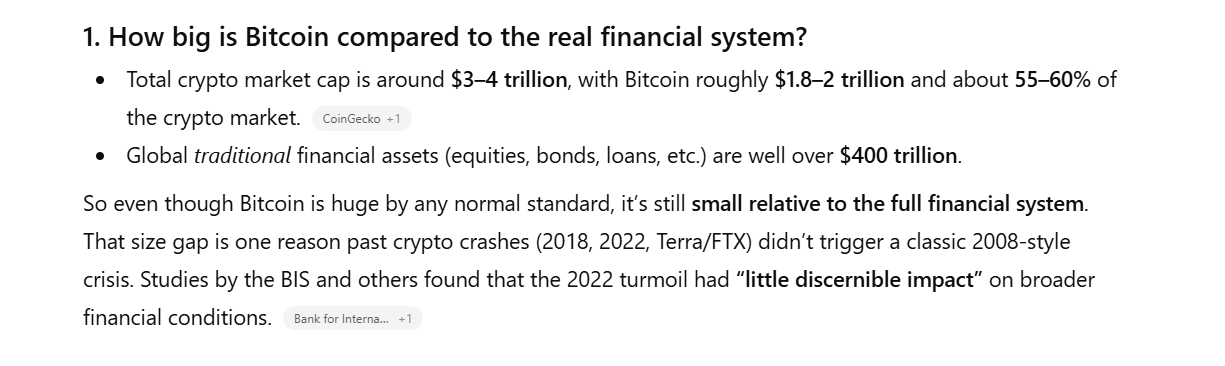

How Big Is Bitcoin Compared to the Real Financial System?

Crypto feels massive and it is. The total crypto market now sits around $3–4 trillion, with Bitcoin alone making up roughly half of that.

But zoom out, and the picture changes completely:

Global traditional financial assets exceed $400 trillion.

This is why past crypto crashes, from the 2018 wipeout to Terra and FTX, didn’t spark anything close to a 2008-style meltdown. Bitcoin is big, but the global system is still much bigger.

ChatGPT’s response to how Bitcoin is compared to the real financial system.

What Actually Causes Financial Crises?

Crises rarely start because one asset’s price falls.

They start because of leverage, interconnections, and panic:

Institutions borrow short-term money to fund long-term risky bets

Prices fall

Collateral evaporates

Margin calls hit

Funds fire-sell everything

Credit freezes

This is the “doom loop” that takes down entire economies.

So the real question becomes:

Is Bitcoin now woven deeply enough into banking, funds, and payment systems that a crash could freeze credit or trigger runs?

Where a Bitcoin Crash Could Actually Threaten the Global Financial System

Institutional Investors & Bitcoin ETFs: The New Wild Card

As a result, Bitcoin’s correlation with stock markets has surged. Research finds that after ETFs and index inclusion, Bitcoin’s correlation with major equity indices (e.g., Nasdaq 100, S&P 500) increased sharply, sometimes above 0.8.

Sudden losses can spill over into stocks and bonds.

Regulators acknowledge the risk is not a crisis-level threat yet, but growing fast.

Stablecoins: The $300 Billion Shadow Money System

Stablecoins now sit at the center of crypto trading and liquidity. Many are backed by short-term government bonds – the same instruments traditional money markets rely on.

Billions of dollars in Treasuries could be sold off fast

That kind of fire-sale pressure has broken funding markets before

The Terra collapse showed how quickly confidence can evaporate – and next time, the stakes will be larger.

Banks, Brokers, and Shadow Leverage

The nightmare scenario isn’t about Bitcoin’s price.

It’s about who is exposed to Bitcoin behind the scenes.

The real danger is if:

Major institutions start lending heavily against Bitcoin

Hedge funds use extreme leverage in crypto derivatives

Synthetic Bitcoin exposure grows in the shadows

Today, most leverage is still outside the core banking system.

But that wall is getting thinner.

A Bitcoin crash could absolutely destroy certain funds, exchanges, and lenders and one day, one of those failures could matter far more than expected.

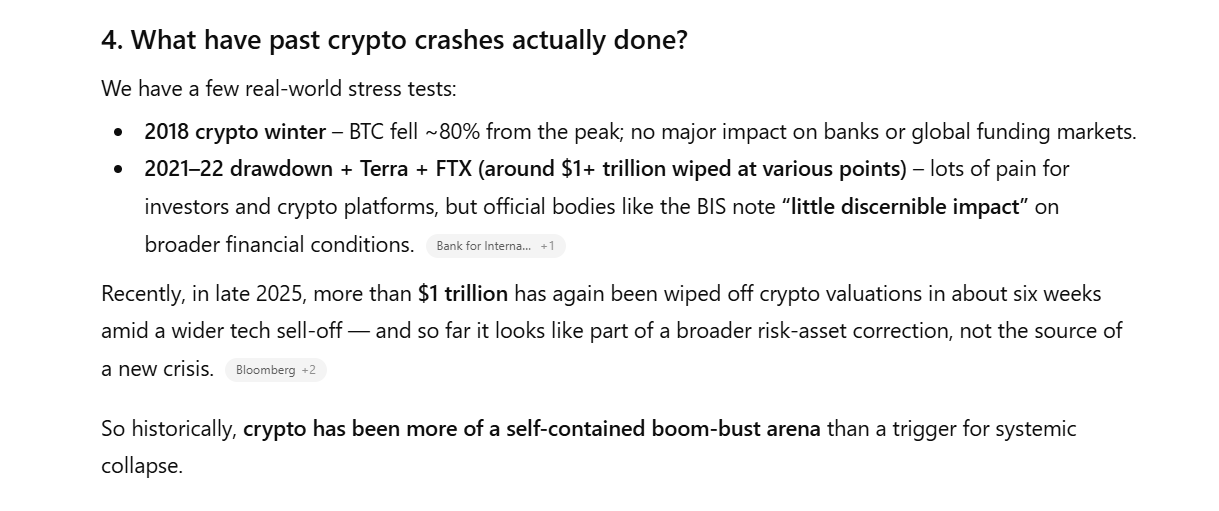

What Past Crypto Crashes Reveal

Crypto users have already seen several stress tests:

2018: Bitcoin fell 80% – no systemic crisis

2021–22: $1+ trillion evaporated – pain in crypto, minimal impact elsewhere. Also, official bodies like the BIS note “little discernible impact” on broader financial conditions.

Historically, crypto has been mostly self-contained.

But every cycle, the walls between crypto and traditional finance get a little lower.

What past crypto crashes reveal, according to ChatGPT.

Could a Bitcoin Crash Ever Trigger an Economic Crisis?

A Bitcoin crash is not likely to trigger a global economic crisis today, but the possibility increases if certain structural trends continue to develop.

The first major factor is scale. If the crypto market grows to around $10–15 trillion and becomes more deeply embedded in pension funds, corporate treasuries, and exchange-traded products, its impact on the broader financial system would expand significantly. At that size, a sharp price collapse would affect a much wider range of institutions and households.

A second factor is interconnection. As banks, insurers, asset managers, and large investment funds adopt Bitcoin-related products, the lines between crypto markets and traditional finance could blur. If these institutions begin using Bitcoin for collateral, liquidity, or short-term funding needs, any major price shock would transmit more easily into mainstream markets.

The third risk comes from leverage. If borrowing against Bitcoin becomes common, whether through structured products, margin loans, or derivatives, losses during a downturn could be amplified. High leverage has historically been a key driver of systemic crises because it forces rapid asset sales and drains liquidity when markets are already stressed.

Finally, broader economic fragility matters. A period of elevated interest rates, slowing growth, or inflated asset valuations would make the financial system more vulnerable. In such an environment, even a shock that starts in crypto could escalate quickly if investors are already nervous or liquidity is scarce.

Taken together, these factors show that a Bitcoin crash would not necessarily be the root cause of a future crisis, but in the wrong conditions, it could become the spark that ignites one.

A major drop in Bitcoin’s price can still create serious financial impacts, even without triggering a global crisis. Investors should understand how a sharp decline can affect their holdings and the broader market.

If Bitcoin Crashes: What You Could Face and Key Lessons for Investors

If Bitcoin Crashes, You Could See:

Portfolio losses, as Bitcoin and related cryptocurrencies move sharply lower.

Exchange disruptions or failures if platforms face liquidity problems or operational stress.

Stablecoin de-pegs, especially for coins heavily used in trading or backed by volatile assets.

Spillover into tech stocks and other risk assets, as investor sentiment weakens and correlations increase.

Key Lessons for Investors

Avoid heavy leverage, which can magnify losses during fast market drops.

Diversify your investments, rather than relying solely on Bitcoin for long-term returns.

Choose reputable, secure trading platforms to reduce counterparty and custody risks.

Use stablecoins cautiously, understanding that they can lose their peg during stress.

Prepare for expanding regulation, which may reshape how exchanges, stablecoins, and crypto products operate.

And remember that today, a Bitcoin crash alone probably won’t trigger a global financial crisis, but tomorrow, if Bitcoin’s integration with banks, ETFs, and stablecoins keeps accelerating, the next big crypto meltdown could become far more than a “crypto problem.”

The scary part?

You may not know when that line has been crossed, until it’s already too late.

Could a Bitcoin crash trigger a global financial crisis?

Not under current conditions. According to economist Nouriel Roubini, Bitcoin’s size remains too small to destabilize the entire global financial system today. However, he warns that as crypto becomes more intertwined with banks, ETFs, and institutional portfolios, the potential for contagion grows.

Why do analysts like Peter Schiff believe Bitcoin is dangerous?

Peter Schiff argues that Bitcoin has no intrinsic value, is driven mainly by speculation, and could collapse sharply, hurting investors and exposing excessive risk-taking in the financial system.

Who decides the price of Bitcoin?

No single person, company, or government decides Bitcoin’s price. Instead, its value is determined entirely by open-market supply and demand across thousands of global exchanges. Prices move based on how much buyers are willing to pay and how much sellers are willing to accept. Market sentiment, institutional activity, macroeconomic trends, and liquidity all play major roles, but there is no central authority controlling or setting Bitcoin’s price.

How can Bitcoin investors protect themselves from extreme volatility?

Avoid heavy leverage, diversify outside crypto, use regulated platforms, and understand that stablecoins, exchanges, and derivatives carry real counterparty risk.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy