How High Can Bitcoin Price Go in 2026? BTC Holds $68K as Jane Street’s 10 AM Manipulation Pattern Allegedly Stops

Share

Key Takeaways

A $100 Bitcoin buy in 2009 at $0.001 would equal about 100,000 BTC, which is billionaire territory at today’s prices.

Even “late” buyers from 2010–2011 could have turned $100 into multi-million-dollar positions if they held.

By 2016, $100 still had 100x+ potential, but the easy, world-changing upside was mostly gone.

Bitcoin’s hard cap, halvings, rising adoption, and “digital gold” narrative all helped small early bets explode in value.

If you got into crypto within the past five years, you’re likely to have one wish: that you bought Bitcoin back when it was a few dollars.

Satoshi Nakamoto published the Bitcoin whitepaper on October 31, 2008. The network went live in 2009, and people started trading it a bit later.

If you weren’t around, it’s fun to speculate on what would have happened if you had bought, say, $100 around that time.

This article will answer that exact question, and then skip to late 2025 and ask what that $100 would look like today, factoring in what would happen if some current price forecasts turn out to be true. To give you the most accurate picture, this article uses the current market price of $86,600 (as of December 17, 2025) as the primary benchmark.

For all the numbers, this article uses rough math and round them so you can track everything more easily.

Top Crypto Tax Accounting Software

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Bitcoin’s first recorded trade (for US dollars, that is) was on October 12, 2009. It involved developer Martti “Sirius” Malmi, who traded 5,050 Bitcoins for around $5.02. This would make one Bitcoin worth $0.000994, or $0.001 when rounded, or about one-tenth of a cent per Bitcoin.

Source: @CryptosR_Us on X

If you purchased $100 in Bitcoin at $0.001 and held it, you’d have about 100,000 BTC. Notably, in 2009, Bitcoin had no centralized exchanges.The first recorded exchange rate was established by New Liberty Standard on October 5, 2009.

Price per BTC:$0.00076$ (less than 1/10th of a cent).

By the end of this article, you will know how much your Bitcoin is worth by late 2025.

For now, just image if Bitcoin pushes up to something like $150,000 in 2026, like what Standard Chartered predicts, you’d have $150 billion in Bitcoin. That’s generational wealth. You’d be entering a new tier of life with its own set of problems unrecognizable from your current ones. And by the way, that’s far more than Strategy’s current holdings.

How Much a $100 Bitcoin Investment in 2010 Is Worth Today

Let’s say you didn’t touch Bitcoin until December 2010, when it was trading for roughly $0.10.

If you bought $100 in Bitcoin at that $0.10 price, you’d have walked away with 1,000 BTC.

At the current price of $86,600 (as of December 17, 2025), that stash is worth $86.6 million.

Even with the current market pullback to $86,600, you’re sitting on enough wealth to never work another day in your life. If Bitcoin rallies to hit $150,000 in 2026, your portfolio would soar to $150 million.

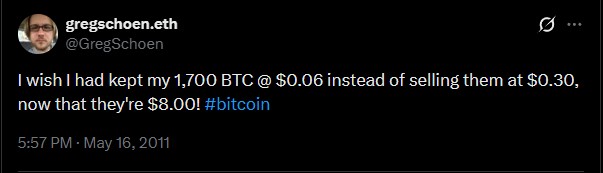

If You Invested in Bitcoin in 2011, Here’s What It’s Worth in Late 2025 or Early 2026

Now let’s skip to 2011, when Bitcoin finally broke above $1.

At the time, you might have rolled your eyes at a friend who wouldn’t stop talking about Bitcoin, and threw $100 in just in case. That $100 is 100 Bitcoin.

Source: @GregSchoen on X

Today, that 100 Bitcoin would be worth $86,600 each, totaling an $8,660,000 return on your investment. Your annoying friend made you a multi-millionaire.

If Bitcoin were to hit $150,000, you’d have $15 million. That doesn’t just pay for a college education, it allows you to buy a dream home, travel the world, and secure your financial freedom forever.

It is important to be aware that while current prices are impressive, Bitcoin actually reached a staggering all-time high of approximately $126,277 in early October 2025. At that peak, your 100 BTC would have been worth over $12.6 million.

Bitcoin 2016 vs 2025: What Early Investors Would Have Today

Jumping to 2016, the year before Bitcoin’s big 2017 breakout, some people believed it was already too late to buy Bitcoin and that the digital asset wouldn’t amount to much.

At the time, Bitcoin was trading in the mid-$400 range. For simplicity, this example rounds the price to $450.

Buying $100 worth of Bitcoin at $450 per BTC would get you about 0.22 BTC. Compared to earlier examples, that may seem small, but at the current price of $86,600, that investment would be worth roughly $19,052.

Even with the current price sitting at $86,600, should Bitcoin rally to hit $150,000, that 0.22 BTC would be worth $33,000. While that’s not “overnight millionaire” money, turning $100 into a substantial house deposit is a financial win by any standard.

How Bitcoin Turned $100 Into Millions?

So how did a $100 random investment turn into a building’s worth of money?

A few core reasons:

1. Hard Cap on Supply

Bitcoin has a maximum supply of 21 million coins. No central bank can come in and print another 21 million just because. That scarcity matters when it comes to supply and demand.

2. Halvings

Around every four years or so, the Bitcoin network cuts miner block rewards in half. This is by design, to slow the supply pouring into the market. Typically, these halvings have led to bull runs due to their effect on supply and demand.

3. Adoption Increase

Of course, when Bitcoin was in the dollar or even hundreds range, only enthusiasts were getting involved. Then exchanges, payment companies, fintech, and entities like Strategy added Bitcoin to their balance sheets which increased its price even more, and this isn’t even to mention ETFs. All this to say, the more “normal” Bitcoin appeared, the more money came in.

4. Macro Fear and “Digital Gold”

As fear of inflation and money-printing to counter it grows, more people begin to treat Bitcoin as a type of “digital gold” alternative investment. In their eyes, Bitcoin is a hedge against central banks and other fiat issues. That potential brings in a ton of serious money.

Put all of these reasons together, and it’s straightforward to understand why world’s first cryptocurrency gained the following it did.

So What a $100 Bitcoin Investment in 2009 Is Worth by Late 2025

If you had actually been able to find a seller for $100 worth of Bitcoin in late 2009 (which would have been difficult given the low liquidity), the numbers look like this:

Total Value Today: $11.34 billion (130,903 BTC * $86,600 = $11,336,199,800)

So your $100 would have grown over 113 million times its original value.

If you had sold 99% of your holdings during the many “all-time highs” over the last 16 years and only kept 1% (approx. $1,309$ BTC) until today:

1,309 BTC * $86, 600 = $113,359,400

Even after selling almost everything, you would still be a centi-millionaire with over $$113$ million in the bank.

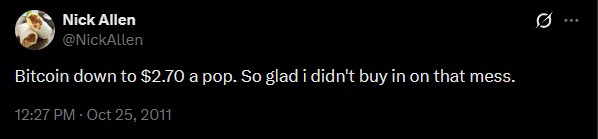

Why Most Early Bitcoin Investors Wouldn’t Have Held Until 2026

Of course, it’s fun to imagine how much money you’d have if you invested all that time ago. But all of that said, you probably wouldn’t have held all the way to 2026.

Source: @NickAllen on X

Along the way you’d have to deal with:

Many, many crashes

Exchange hacks

Governments going back and forth regarding regulation

Friends and family calling Bitcoin a scam

So much more…

It’s much more likely you’d have sold when Bitcoin 10x’d due to what feels like an absurd return on investment.

The funniest part is, even if you’d sold 90% of your holdings somewhere along the way and held the rest, you’d still have insane returns.

Navigating the Shadows: Understanding the Risks of Bitcoin

While the potential for life-changing gains is undeniable, Bitcoin remains one of the most volatile and complex financial assets in existence. As you head into 2026, the “digital gold” narrative is stronger than ever, but so are the pitfalls. Before imagining your $150 million retirement, you must account for these three primary risk categories.

1. Extreme Volatility & The “October Cliff”

Bitcoin is famous for its “boom and bust” cycles. As seen in late 2025, the price can reach a historic peak (like the $126,272 high in October) only to retract by 30% or more within weeks.

The emotional trap: Investors often buy during the “hype” phase at the top and panic-sell during corrections.

The reality: At today’s price of $86,600, you are still up significantly from 2016, but if you bought at the October peak, you are currently “underwater.” Only those with “diamond hands,” the ability to ignore short-term crashes, historically survive these swings.

2. The Self-Custody Burden: “Not Your Keys, Not Your Coins”

If you hold 100 BTC, you aren’t just an investor; you are your own bank. This comes with immense responsibility.

Exchange risks: Keeping large amounts on centralized exchanges (like the now-defunct FTX or Mt. Gox) exposes you to platform insolvency or hacks.

Irreversibility: Unlike a credit card, Bitcoin transactions cannot be reversed. If you send 1 BTC to the wrong address or lose your 12-word recovery phrase, those funds are gone forever. There is no “Forgot Password” button for a hardware wallet.

Sophisticated scams: 2025 has seen a record rise in “deepfake phishing” and AI-driven malware. Scammers now use high-tech tools to mimic official support teams or exchange CEOs to steal private keys.

3. The Shifting Regulatory Landscape

The “Wild West” days of crypto are ending. As of late 2025, major economies like the UK (via the FCA) and the US are finalizing strict market-structure bills.

Taxation: Governments are becoming highly efficient at tracking on-chain movements. Failing to report capital gains on your $8.66 million fortune can lead to severe legal penalties and asset seizures.

Compliance: New “Market Abuse” regulations arriving in 2026 aim to stop insider trading and manipulation. While this makes the market safer for institutions, it may temporarily dampen the explosive, “irrational” price surges that retail investors love.

The golden rule of 2026: Never invest money that you cannot afford to lose entirely. While the upside could lead to a $150 million portfolio, the path there is paved with 80% drawdowns, regulatory hurdles, and constant security threats.

Don’t spend more than you can afford to lose: As with all investing, never put more in Bitcoin than you’re willing to lose.

Spread buys over time: Dollar-cost averaging, or buying a set amount of Bitcoin on a schedule, such as weekly, daily, or monthly, helps avoid the “bought at the top” issue.

Diversify: Make sure Bitcoin is far from your only investment avenue. Keep it alongside your other investments, as you never know what can happen.

Not on a big exchange, but the first known Bitcoin to USD trade (5,050 BTC for $5.02) implies a price just under $0.001 per coin based on that private deal.

Could Bitcoin really hit $150,000 by 2026?

Banks like Standard Chartered and other analysts have floated six-figure targets, but they remain speculative and depend on macro conditions and adoption.

Why did early Bitcoin gains get so extreme?

The price started near zero, supply was capped, halvings slowed new issuance, and demand exploded as exchanges, ETFs, and companies piled in.

Would I realistically have held from 2009 to 2026?

Almost nobody would. Multiple 70–80% crashes and negative headlines would have shaken most investors out long before.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Max Moeller is a Chicago‑based writer and video editor passionate about games, tech, and crypto. Whether it’s crafting clear, insightful articles or piecing together engaging video retrospectives, he’s driven by curiosity and takes pride in keeping things human. Since 2017, Max has been published in a variety of notable crypto magazines.

Easy

Easy