Dow Futures Rally as Treasury Yield Spread Approaches Dangerous Level

Bond markets are telling us that recession fears are still driving investor behavior. | Image: Johannes EISELE / AFP

Futures on the Dow Jones Industrial Average (DJIA) rose in overnight trading Monday, as China trade optimism caused investors to look beyond a breakdown in U.S. Treasury yields.

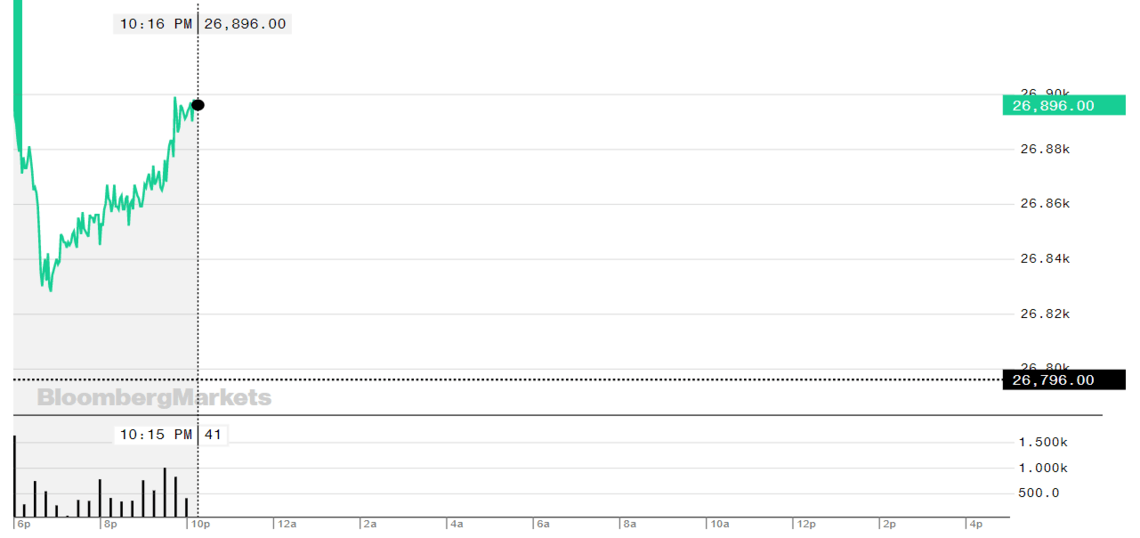

Dow Futures Rally; S&P 500, Nasdaq Follow

The three main U.S. futures contracts reported gains Monday, with the Dow Jones Industrial Average climbing 98 points, or 0.4.%, to 26,894.00. The futures contract was up by as much as 144 points.

S&P 500 futures climbed 0.4% to 2,975.50. The Nasdaq 100 futures contract jumped 0.5% to 7,739.74.

U.S. equities recoiled Friday amid reports that the Trump administration was looking to implement new constraints on Chinese investments – a move that would mark a dramatic escalation in the ongoing trade war. Although the U.S. Treasury has since denied the reports, plans for further escalation have apparently been discussed within the Trump administration.

Bond Markets Come Close to Flashing Warning Signal

The spread between 10-year and 2-year Treasurys – the stock market’s most trusted barometer for recession – has narrowed in recent weeks, sending a strong signal that another inversion was on the horizon.

A yield curve inversion happens when bonds with shorter maturities yield more than their long-term counterparts, a phenomenon that effectively negates the value of time in the monetary system. Inverted yield curves have predicted the past seven recessions with razor accuracy.

At the time of writing, the yield spread between 10-year and 2-year Treasury notes was around 6 basis points. A narrowing of the spread to zero or below would trigger another recession warning like the one we saw in August.

At the time, safe-haven buying drove investors into fixed-income securities, which dragged the 10-year yield toward record lows.

Inverted yield curves usually predict recession – i.e., back-to-back quarters of negative growth – 22 months later.