Key Takeaways

- U.K. house prices faced mixed performance in 2024, raising doubts about BoE policy effectiveness.

- House prices started 2025 with a bang but slowed in April.

- High interest rates tackled inflation but negatively affected the British housing market.

- However, analysts expect a busy market in 2025.

The U.K. housing market, long admired for its resilience and upward trajectory, now faces mounting questions about its stability.

Property prices defied economic turmoil and global crises for years, continuing their relentless climb.

However, recent shifts in the Bank of England’s (BoE) interest rate policy have introduced ripples of uncertainty.

With the broader economy under strain, concerns are growing that the era of unshakeable price growth may be nearing its end.

This prompts speculation about whether a long-anticipated market correction is on the horizon.

April Decline Tops Market Expectations

U.K. house price growth eased in April, with monthly prices falling more sharply than expected, according to Nationwide data.

Annual house price growth slowed to 3.4%, down from 3.9% in March. On a monthly basis, prices declined by 0.6%—a larger drop than the 0.1% fall forecast by analysts—bringing the average price down to £270,752 from £271,316.

Nationwide’s monthly index slipped to 539.3 in April from 542.4 the month before.

Chief Economist Robert Gardner attributed the slowdown to changes in stamp duty introduced at the start of the month, which likely prompted buyers to rush transactions in March.

“We saw a surge in activity ahead of the tax changes, and a softer market this month was expected,” Gardner said.

“Looking ahead, activity may remain subdued in the near term, but we expect a gradual rebound as summer approaches. Despite global economic headwinds, underlying conditions for UK homebuyers remain supportive,” he added.

Property Market in “Morning After” Territory

Jonathan Hopper, CEO of Garrington Property Finders, told CCN: “Parts of the property market entered full ‘morning after’ territory in April.”

“With the breathless, distorting effects of the brief ‘Stamp Duty Stampede’ over, the market has reverted to the conventional forces of demand and supply – and together these have started to down average prices,” he added.

According to Hopper, in some parts of the U.K., the supply of homes for sale is now far outstripping demand. This is especially true in more expensive, and often highly desirable, areas where the trickle of supply has turned into a flood.

In these areas, buyers find themselves blessed with both abundant choice and considerable negotiating power, and this is keeping prices flat or even nudging them down.

“At the other end of the scale, in less expensive areas the balance between the two forces is more equal, and prices are still creeping upwards as buyers compete for homes they feel represent strong value,” the analyst said.

Looking ahead, the prospect of interest rate cuts over the coming months will make mortgages more affordable and give buyers a little more leeway in their budgets.

“This should help average house prices inch upwards, but the abundance of supply will ensure that the pace of price rises remains modest,” Hopper added.

House Prices Dip in March

The average U.K. house price fell 0.5% in March to £296,699, a sharper drop than February’s 0.2% decline, according to Halifax. Despite the monthly dip, annual growth held steady at 2.8%.

Halifax’s Head of Mortgages Amanda Bryden noted that buyers are rushing to beat the March stamp duty deadline in January’s price rise. With those deals now complete, demand is easing, and new applications are slowing.

Bryden added that while borrowing costs remain high and supply limited, expected base rate cuts and wage growth should gradually improve affordability, supporting a modest rise in prices over the year.

London remained the most expensive region at £543,370, slowing growth to 1.1%. Northern Ireland led annual gains, up 6.6% to £206,620, while Yorkshire and Humberside saw a 4.2% rise to £215,807.

Market Faces Turning Point

Jonathan Hopper, CEO of Garrington Property Finders, told CCN, “With the brief period of supercharged Stamp Duty-related sales over, the average pace of price rises is coasting in neutral.”

According to the analyst, March’s slight dip in average prices is more likely to be a return to business as usual than the start of a major slide, but it does reflect two things: with buyers no longer racing to meet the Stamp Duty deadline, demand has become more measured; and the surfeit of supply in some areas is keeping a lid firmly on price rises.

“The price-sensitivity of many buyers is leading many to focus their attention on areas where value is perceived as better. This is why average prices in Scotland are rising four times faster than those in London; in Northern Ireland, they’re growing six times faster than in the capital,” Hopper added.

“In coming months, prices will be determined by how the market reacts to the conventional forces of supply and demand and how Donald Trump’s rewriting of the global order plays out.”

“The market is at a turning point, and with so many properties coming up for sale, sellers need to price their homes carefully or risk seeing them stuck unsold on the shelf,” the expert said.

U.K. Records Increased Prices in March

Property prices in the U.K. rose in March, according to Rightmove data, with new buyers facing a record-high selection of properties.

The average asking price for homes listed in March is £371,870, marking a 1.1% increase, or £3,876, compared to the same period last year. This aligns with the typical March price rise, as sellers price competitively amid strong market competition.

Rightmove’s weekly mortgage tracker reports that the average five-year fixed mortgage rate is 4.74%, a slight decrease from 4.84% in 2024 but still significantly lower than last summer’s peak of 6.11%.

Despite this, the firm noted that high mortgage rates are still curbing market activity and dampening overall optimism.

The property market is traditionally active in March, and Rightmove has highlighted that buyers this spring have access to the largest selection of properties since 2015. However, this comes as buyers face the upcoming increase in tax charges from April and lose out on additional stamp duty savings.

While global uncertainty continues, Rightmove reported that the property market has remained steady in 2025, with positive growth anticipated in the spring. Sales have risen 9% year-on-year, and new listings are up by 8%, signaling continued market momentum ahead of the April stamp duty changes.

Global Economic Turbulence Hits U.K. Mortgages

Rightmove’s Matt Smith commented: “We’re still seeing lenders price competitively where they can to secure mortgage business at this typically busy time of year.

“However, the economic turbulence happening globally is impacting mortgage rates, and we’re seeing some small rate fluctuations on a week-by-week basis.”

“Most affected are rates for those with the smallest deposits, which is a double whammy for first-time buyers and those who need to borrow more,” he said.

Looking ahead, Smith continued: “We’ve got the next interest rate decision coming up from the Bank of England, and the current expectation is that we’ll see a hold, followed by a cut in May.”

“However, we’ve already seen this year how quickly things can change, so a lot will depend on other economic news we have between the two Bank of England meetings.”

Economic Activity May Influence the Housing Market

Rightmove said there are currently more than 550,000 sold homes awaiting legal completion, which is 25% higher than the same time last year.

Applications for a mortgage in principle on Rightmove also hit a record high in January, increasing 49% year over year.

However, Rightmove said that “global and economic news could temper this momentum and affect sentiment and outlook for the market, with attention turning to upcoming inflation and earnings figures.”

Matt Smith, mortgage expert at Rightmove, said: “We’ve now had the first Bank Rate cut of the year, and current forecasts suggest there are still two or potentially three more cuts to come, which could see us closing out the year with a Base Rate of 4% or lower.”

“The response from the market to the decision has been positive, and mortgage rates have trickled downwards since the announcement.”

“We hope this is the beginning of a sustained period of rates slowly heading downwards, and while we’re unlikely to see major falls across the board, we’ve already seen the first sub-4% rates of 2025,” Smith added.

Uncertainty Over BoE Rate Cuts

Despite some positive early indicators, experts remain cautious about the future. “It’s important to look at the bigger market picture, despite the positive early lead indicators that we’re seeing,” Rightmove said.

Many buyers are still grappling with affordability issues, as high mortgage rates limit their borrowing power and reduce their affordability.

Colleen Babcock, an analyst at Rightmove, noted that first-time buyers are facing even greater challenges with reduced support schemes and higher stamp duty fees set to kick in next month, “all while contending with record rents and trying to save up for a deposit.”

Matt Smith, a mortgage analyst, added, “news of high government borrowing costs was swiftly followed by better-than-expected inflation figures, highlighting how quickly the mood can change.”

While markets are anticipating a rate cut in February, Smith cautioned that the outlook beyond that is uncertain. “I think we’ll need to get settled into the year a little more before the direction of travel for rates this year becomes clearer.”

BoE Rate Cuts Have Positive Impact on Confidence

Jason Tebb, president of OnTheMarket, said, “Two interest rate reductions in recent months have had a positive knock-on effect on confidence, which the market relies on. The unwelcome news that inflation has edged upwards to 2.6% is not surprising but still a blow as it may well encourage the Bank of England to delay further rate reductions.”

“Affordability remains a challenge but the market continues to tick along, with focused buyers who may have put plans on hold welcoming lower mortgage rates,” he added.

David Hollingworth, associate director at L&C Mortgages, said, “Mortgage borrowers shouldn’t expect to see much change because of today’s figures,” and added:

“Further base rate cuts are expected next year, but the Bank of England has played a consistent line that those reductions are more likely to be slow and steady in pace. The figures today do nothing to suggest that line is about to change.”

Mortgage rates had edged higher in recent months due to concerns over greater inflationary pressure from the measures announced in the budget.

Asking Prices To Rise in 2025

Tim Bannister, Rightmove’s director of Property Science, said, “We are now looking ahead to the traditional Rightmove Boxing Day bounce in home-mover activity, which has increasingly become a key date in the housing market calendar,” adding:

“Each year, our real-time data can pinpoint the exact moment that the turkey is finished, family games run out of steam, mobile devices are picked up, and prospective movers flood onto Rightmove and get their 2025 move started. If this year is anything like recent years, those early birds who get their search started the day after the festivities are over are likely to be rewarded with plenty of fresh property choices to consider.”

Rightmove said prices are holding up best in the first-time buyer sector, especially homes priced below £300,000.

The analyst expects new seller asking prices to grow by 4% next year, as forecast mortgage rates may drop following the Bank of England’s cuts in interest rates:

“Looking at our data and the U.K.’s underlying housing needs, there are lots of reasons to be positive about next year.”

“However, as we’ve seen several times this year, the market is sensitive to unexpected events, and the direction of travel can change. The stamp duty changes are a cloud over the market at the moment, with some groups much more impacted than others, and therefore keen to avoid the additional charges. After the important first three months of the year in 2025, a lot depends on how quickly normal activity is resumed with higher stamp duty in England. A bank rate cut and some mortgage rate falls early on in the year would help to settle the market and provide a boost to sentiment and consumer confidence,” Bannister added.

BoE’s Impact on Estate Market

Laura Suter, Director of Personal Finance at AJ Bell, anticipates a status quo from the Bank of England this week.

Despite the recent rate cut in August, the Bank of England is widely expected to maintain interest rates at 5% during this week’s meeting.

The central bank has been cautious about rapid rate reductions, signaling a preference for a gradual approach. While markets currently favor a hold, a small cut to 4.75% remains a possibility.

The upcoming inflation data could introduce some uncertainty into the Bank’s decision. A deviation from expectations could influence the monetary policy committee’s assessment.

With no meeting scheduled for October, the Bank avoids the potential conflict of making interest rate decisions immediately before the Budget. This allows time to analyze the government’s fiscal plans and inform subsequent policy decisions in November and December.

“Regardless, interest rates are expected to end the year at 4.5% – signaling two successive cuts before Christmas. That would be the best present that wannabe homeowners could get, with a mortgage rates war already hotting up. More interest rate cuts could put fire-starters under the housing market once again, which has already seen activity pick up since last month’s cut. Equally, a hold to interest rates this month might mean that some buyers decide to delay their house buying journey until later this year, in anticipation of lower interest rates,” Suter said.

Mortgages Hit a New Record

The number of mortgages approved for homebuyers surged to its highest level since the mini-budget was introduced under former Prime Minister Liz Truss.

According to the Bank of England, 62,000 mortgage approvals were recorded in July, the highest figure since 65,100 were reported in September 2022.

Mortgage rates spiked following the “growth plan” statement by then-Chancellor Kwasi Kwarteng in September 2022. However, in recent weeks, mortgage rates have been gradually declining, and earlier this month, the Bank of England lowered its base rate by 0.25 percentage points to 5%.

The Bank’s Money & Credit report showed increased house purchase approvals from 60,600 in June. In contrast, remortgaging approvals (which only account for loans with a different lender) dropped to 25,100 in July, down from 27,300 in June.

House Sales Increased

According to HM Revenue & Customs figures, the number of home sales in the U.K. in June was 8% higher than in the same month the previous year.

There were an estimated 91,370 transactions, an 8% increase from June 2023 but slightly lower—less than 1%—than in May 2024. HMRC noted that this slight month-on-month decline marks the first decrease since December 2023.

Iain McKenzie, chief executive of the Guild of Property Professionals, commented, “Transaction numbers have been steadily growing for some time now, and a month-on-month decrease is nothing but a fly in the ointment. The market still shows strength when compared to the previous year, with June’s figures 8% higher than the same time last year.”

He added, “It’s important to consider these figures in the broader context of the market’s recovery. The overall trend for 2024 remains positive, and higher transaction levels than last year suggest that buyer confidence is gradually returning to the market.”

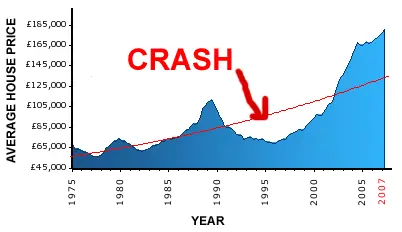

What Is a House Price Crash?

A house price crash, often known as a housing market crash, can evoke anxiety among homeowners, potential buyers, and economists. Fundamentally, a house price crash represents a substantial and abrupt decline in the prices of residential real estate, particularly within the housing market.

It marks the point where the seemingly relentless increase in property values abruptly halts and takes a sharp, often painful turn downward.

During a house price crash, homeowners typically encounter challenging circumstances. The value of their most significant asset, their home, diminishes, making it difficult to sell or refinance. Those who purchased their homes at the market’s peak may find themselves in a state of negative equity, owing more on their mortgage than their home’s current value.

- When does a price crash happen?

For potential buyers, a house price crash can present a mixed picture. On one hand, it makes homes more affordable. However, it can also serve as an indicator of economic instability and the possibility of stricter lending standards, which can complicate the home-buying process.

In summary, a house price crash is a pivotal event within the real estate market, with far-reaching economic and social implications. It signifies a significant and sudden drop in home values, influenced by various factors. Understanding the causes and consequences of such a crash is vital for both current homeowners and those aspiring to enter the property market.

What Causes a Property Market To Crash?

The property market, often considered a pillar of stability in the economy, can sometimes experience dramatic downturns, leading to a property market crash. Such crashes can profoundly affect homeowners, investors, and the broader economy. But what are the factors that can cause a property market to crash?

Economic Downturns

One of the primary triggers of a property market crash is an economic recession. During economic downturns, people tend to have less money to spend, leading to declining demand for properties. As unemployment rises and consumer confidence wanes, homebuyers become scarce, and sellers may lower their prices to attract buyers.

- Prices increase over the years.

Interest Rate Hikes

Central banks control interest rates to manage inflation and economic growth. When interest rates rise, borrowing becomes more expensive. This can lead to reduced demand for homes, particularly in areas where mortgages are the primary means of home purchase. Higher interest rates can also put pressure on homeowners with adjustable-rate mortgages.

Speculative Bubbles

Property markets can experience speculative bubbles, where prices rise significantly above their intrinsic values. This can be fueled by speculative buying, often with the expectation of quick profits. When the bubble bursts, property prices can fall dramatically, leaving investors and speculators with significant losses.

Tightened Lending Standards

Financial institutions often tighten lending standards in response to economic conditions or regulatory changes. When lending standards become more stringent, it can be harder for buyers to secure mortgages, leading to a decline in demand and, subsequently, property prices.

Overbuilding

An excess of new construction projects can lead to an oversupply of properties. This can happen when developers overestimate demand or when market conditions suddenly shift. An oversupply can put downward pressure on property prices as sellers compete for a limited pool of buyers.

Natural Disasters and Local Factors

Local conditions, such as natural disasters or job market fluctuations, can impact property markets. For instance, an area prone to natural disasters like hurricanes or earthquakes may experience property market crashes due to property destruction and a decrease in demand.

Global Economic Crises

Major global economic crises, like the 2008 financial crisis, can substantially impact property markets. These crises can lead to widespread economic uncertainty, job losses, and a lack of confidence in the property market.

Mortgage Lending Set To Fall In 2024

Mortgage lending is anticipated to decline in the coming year, with an expected rise in arrears and repossessions, as outlined by U.K. Finance, a trade association for the U.K. banking and finance industry. Despite ongoing challenges in the mortgage market, U.K. Finance suggests that the primary affordability pressures are currently reaching their peak. ù

While the easing of financial strains may take time, improvement is projected in 2025. U.K. Finance predicts a decrease in lending for house purchases to £120 billion in 2024, down from £130 billion in 2023.

External remortgaging activity is expected to decrease to £60 billion from £65 billion, and the value of internal product transfers is forecasted to fall from £219 billion to £202 billion in 2024.

The report emphasizes that various factors are mitigating payment issues, ensuring that over 99% of the 10.8 million mortgages in the U.K. are currently not in arrears.

New Bank of England data, revealed on May 31, 2024, shows there were 61,100 mortgage approvals for house purchases in April, slightly down from March’s 61,300 and below forecasts of 61,500.

However, mortgage borrowing rose significantly last month, with £2.4 billion borrowed in April compared to £0.5 billion in March.

Mortgage approvals are an indicator of future borrowing.

The remortgaging market also cooled, with net approvals for remortgaging (with a different lender) decreasing to 29,900 from 33,500. This suggests higher mortgage rates deterred people from switching to new deals.

U.K. Homes for Sale Hit a Record High

Britain’s housing market has reached its highest supply of homes for sale in eight years, a trend that experts believe will curb house price increases for the rest of 2024.

According to Zoopla, a leading property website, the average estate agent now has 31 homes for sale—up 20% from the same period last year and the highest number since 2016. This surge in listings translates to approximately GBP 230 billion worth of homes on the market, as more sellers are re-entering the housing market in growing numbers.

Many homeowners postponed their moving decisions in the latter half of last year as higher borrowing costs impacted house prices and buyer demand, dampening confidence. Nearly one-third of the homes currently for sale were also listed in 2023 but failed to find buyers.

However, an anticipated drop in mortgage rates this year and rising sales volumes over the past six months have improved market sentiment. Experts predict that the Bank of England may cut interest rates in the coming months. This may follow a decrease in headline inflation to 2.3% from 12 months to April 2024.

The number of house sales agreed has increased by 13% compared to this time last year, though it still lags behind the supply level, providing buyers with a broader selection of properties. This trend may keep house price inflation in check. Zoopla’s latest index shows an annual house price deflation of 0.1%, indicating a slight price decline over the past year.

Despite a 0.4% increase in house prices over the last quarter, quarterly growth has slowed in the past month. Zoopla anticipates that house price inflation will remain flat for the year.

Can the U.K. Government Stop a House Price Crash?