Investors betting on a swift economic recovery have lost their minds. The coronacrisis will leave ripples for years to come. | Image: Spencer Platt/Getty Images/AFP

Share

The U.S. jobs report showed a decline of 20.5 million jobs in April while the unemployment rate rose to 14.7%.

The “real” unemployment rate surged to 22.8%, some say more, which reflects the worst of the Great Depression.

Many of those jobs are not returning for a long time; many others, never at all.

The Dow Jones ignored the worst U.S. jobs report in history as if it were of no concern because investors hope the coronavirus crisis is here on a short-term stay.

All Investors Do Is Ignore

Some say the Dow has already discounted bad jobs reports. I say it has not even begun to factor them in fully. Investors are running on testosterone, and pretending these historically savage reports will quickly fade.

The latest rise in unemployment is nothing new–it is old news that has mostly been denied.

For example, the Dow initially began to recover because the crisis was supposed to go away in May. The number of new Covid-19 cases was supposed to be way down by now, and jobs were supposed to return.

That was nonsense at the time, and it has been proven wrong now.

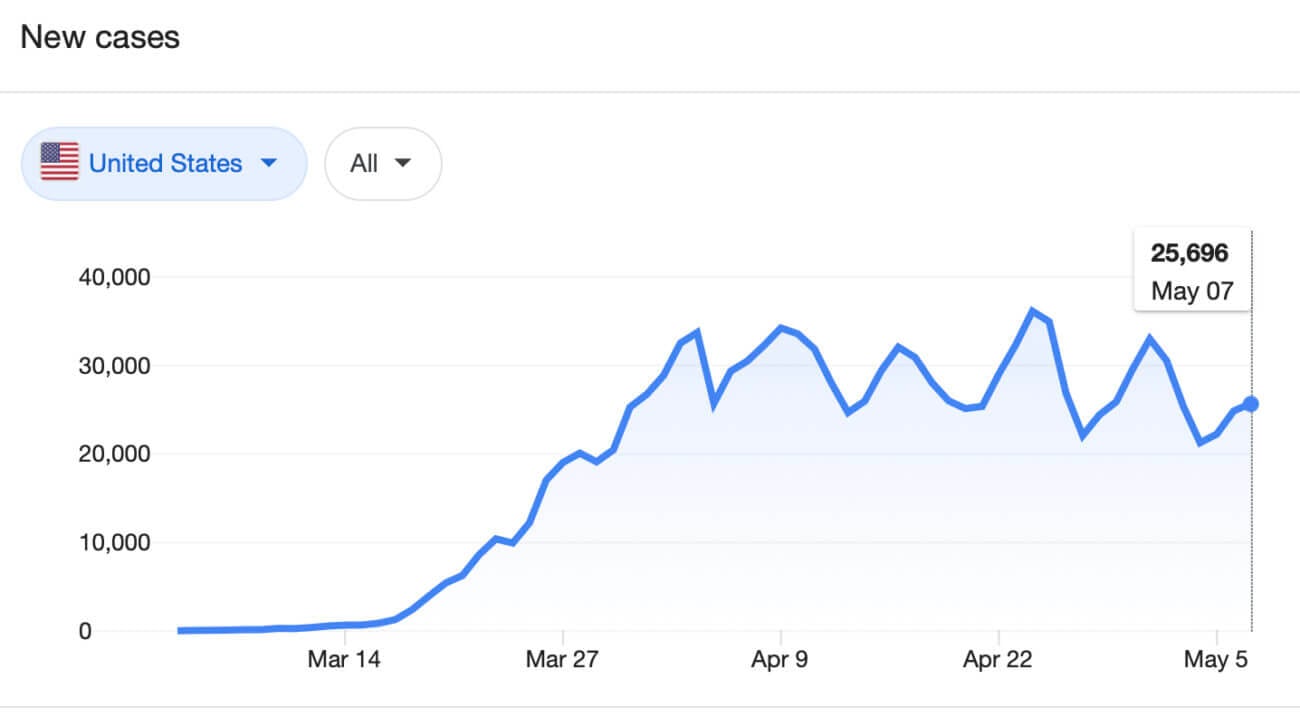

This graph shows the coronavirus has barely slowed its assault on the U.S. That means re-opening risks rampant new infections that could send the U.S. through this whole unemployment cycle all over again.

It’s unwise to simply ignore that strong possibility. Even Dr. Anthony Fauci says it is “inevitable” the virus will return in the fall, and it may not even go away in the summer:

Instead of dropping when that reality became apparent, however, the Dow rose because investors chose to believe the coronacrisis has merely postponed its departure until June. After all, it’s hard to catch a flight out these days.

It only took Credit Suisse Chief Economist James Sweeney one sentence to explicate what this says about the U.S. economy: “This might be the worst macroeconomic data report in U.S. history.“

The Dow shot up because investors are choosing to believe that unemployment will soon improve. But the unemployment rate will have to improve to be as good as it was before the coronacrisis to justify valuations that were already overpriced before the virus slaughtered American jobs.

Besides ignoring the worst job report in history, investors have chosen to ignore a full week of the worst earnings reports in history and the most dismal forward guidance on earnings. Forward expectations are so gloomy most companies are not giving any guidance, which is also historic.

The Dow rose despite rapidly rising bankruptcies, rapidly falling corporate credit ratings, rising mortgage defaults, etc. based on hopes in a phantom vaccine that may not even be possible to achieve.

If investors are going to tune out all of that as mere noise, what does the most giant flush of a jobs report in history matter? Just more noise that would spoil the party.

Nonfarm payrolls fell by 20.5 million in April and the unemployment rate rose to 14.7%, both post-World War II records. Economists had been expecting a loss of 21.5 million jobs and the unemployment rate to surge to 16%. The “real” unemployment rate, which includes workers not looking for jobs and the underemployed, surged to 22.8%.

Records were not kept during the Great Depression by the same measures used now, and present records leave many out. That makes an exact comparison in employment statistics impossible…. Unemployment remained above 14% from 1931 to 1940…. During the Great Recession, unemployment reached 10% in October 2009.

Unemployment that is “greater than the Great Depression” ought to be worth greater consideration. Astonishingly, the latest jobs report doesn’t even count the last half of April.

As Dreadful as the Jobs Report Was, the Truth Is Far Worse

Real unemployment is far more distressing than this report reveals and direr than the Dow is willing to believe. And it is far from being temporary.

First of all, unemployment numbers would be worse then they were during the Great Depression if calculated as they were during the Great Depression.

At its peak, the Great Depression hit a 25% unemployment rate:

Shadowstats, a site that recalculates unemployment as it was historically measured (without the government’s goal-seeking adjustments), states that the unemployment rate is actually around 35.7% if calculated by historical methods:

To be counted among the U.S. government’s headline unemployed (U.3), an individual has to have looked actively for work within the four weeks prior to the unemployment survey conducted for the Bureau of Labor Statistic (BLS). If the active search for work was in the last year, but not in the last four weeks, the individual is considered a “discouraged worker” by the BLS, and not counted in the headline labor force…..

Re-opening the economy is going to happen incrementally. Since New York started re-opening, the number of new coronavirus cases has begun creeping back up.

Many communities have canceled all public events throughout the summer. That’s a lot of lost summer jobs. Theaters are not re-opening this summer. Sports events aren’t coming back this summer. All of those events help juice surrounding businesses like restaurants.

Many colleges are not planning to fully re-open even in the fall. That will be a job hit for college towns.

With all that local tax revenue lost, governments will have to restructure to balance their budgets. That will result in new losses in government jobs.

This has to be the most heartbreaking day in the history of the job market … We could get back to the same level … by 2021 or 2022 … The market is willing to bet it will get lucky:

Disclaimer: The opinions expressed in this article do not necessarily reflect the views of CCN.com.

David Haggith lives in the Pacific Northwest and is the publisher of The Great Recession Blog for eight years, from which his articles about the economy are carried on over fifty economic news websites. He writes exclusives for CCN and is a regular contributor at Seeking Alpha, TalkMarkets, and Zero Hedge. His Twitter page of occasional economic humor is @EconomicRecess. WritelyYours (@) gmail.com