Strategy halted Bitcoin purchases for the first time in years, choosing to repurchase $1.5 billion in bonds instead. Here’s why Michael Saylor made the move. | Credit: CCN.com

Share

Key Takeaways

Strategy paused Bitcoin purchases for the first time in years and instead repurchased $1.5 billion of its own convertible bonds at a discount.

The bond buyback is aimed at strengthening the company’s balance sheet, reducing future debt pressure, and minimizing potential shareholder dilution.

Michael Saylor framed the move as temporary, posting on X that the company’s “₿itVac is charging,” signaling future Bitcoin purchases could resume later.

Michael Saylor’s Strategy has temporarily stepped away from its aggressive Bitcoin accumulation strategy for the first time in years, opting instead to repurchase $1.5 billion worth of its own convertible bonds.

The move marks a notable shift for the company that became synonymous with corporate Bitcoin adoption and relentless BTC buying.

In a post on X, Saylor acknowledged the unusual move, writing: “This week we bought bonds, not Bitcoin. The ₿itVac is charging.”

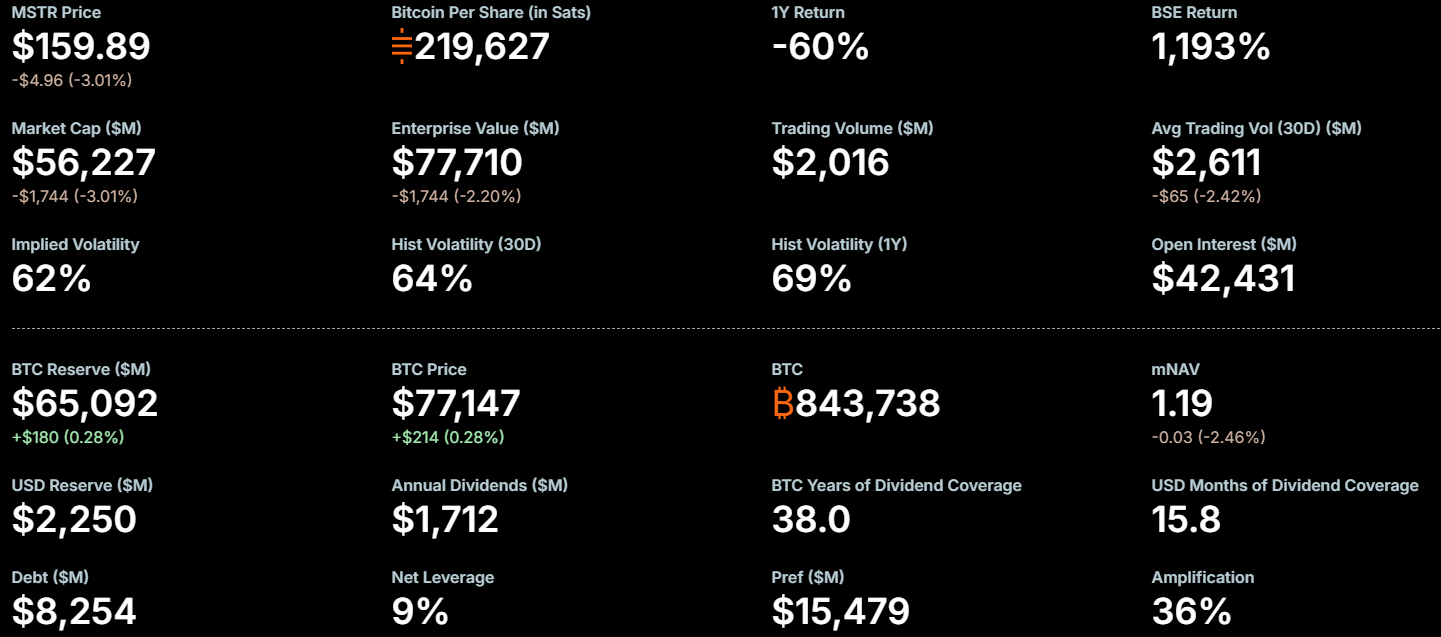

The decision comes as Bitcoin continues to trade steadily near $77,000, while Strategy maintains one of the largest corporate treasuries of Bitcoin in the world. The company currently holds approximately 843,738 BTC valued at more than $65 billion, according to market data shared online.

While some investors view the bond repurchase as a strategic financial maneuver designed to strengthen the company’s balance sheet ahead of future Bitcoin purchases, others see it as a departure from Saylor’s long-standing “never sell your Bitcoin” philosophy.

New Trending Crypto Wallet Offers

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Strategy Prioritizes Balance Sheet Over New Bitcoin Purchases

Rather than deploying capital into fresh Bitcoin acquisitions, Strategy used cash reserves, proceeds from stock sales, and potentially even Bitcoin-related liquidity to buy back its own 0% convertible notes at a discount.

The repurchase helps the company reduce future debt obligations and lower the risk of shareholder dilution tied to the convertible bonds. Analysts following the company say the move could also help Strategy avoid a liquidity crunch ahead of the bonds’ 2027 maturity.

Strategy repurchased $1.5 billion of its own 0% convertible notes at a discount. | Credit: Michael Saylor X profile

Despite the pause in Bitcoin accumulation, Strategy’s crypto holdings remain enormous. The company’s Bitcoin reserve is currently valued at roughly $65.1 billion, while its enterprise value sits near $77.7 billion.

The company’s financial metrics show relatively modest leverage compared to the scale of its Bitcoin treasury. Strategy’s reported debt stands at approximately $8.25 billion, with net leverage near 9%.

Supporters argue that retiring discounted debt now gives the company greater flexibility later, especially if Bitcoin enters another major bull cycle.

Investors Debate Whether Saylor’s Bitcoin Conviction Is Changing

The decision immediately sparked debate across crypto markets, largely because Strategy and Saylor have built their public image around unwavering Bitcoin accumulation.

For years, Saylor repeatedly argued that Bitcoin was superior to cash, bonds, and traditional treasury assets. Strategy routinely issued debt and equity to fund additional Bitcoin purchases, becoming one of the most closely watched institutional Bitcoin proxies on Wall Street.

This latest move, however, suggests the company may be entering a more defensive phase as macroeconomic conditions remain uncertain and Bitcoin price momentum cools.

Bitcoin has largely traded sideways around the $77,000 range in recent weeks, limiting the explosive upside momentum that fueled previous Strategy buying sprees.

Critics argue that using capital to repurchase bonds instead of accumulating more BTC may indicate management is becoming more cautious about short-term market conditions.

Others questioned whether the company may have indirectly reduced some Bitcoin exposure to help finance the transaction, although no direct evidence has confirmed any significant BTC sales.

Still, Saylor’s public messaging remains firmly pro-Bitcoin, and the company continues to market itself as the world’s leading Bitcoin treasury firm.

Why the Bond Buyback Could Position Strategy for Bigger Future Moves

Many analysts on X believe the move ultimately reflects financial discipline rather than weakening conviction in Bitcoin.

By reducing debt pressure early, Strategy potentially improves its ability to raise fresh capital in the future under more favorable conditions. The repurchase also reduces the threat of future share dilution, an issue that has concerned some investors as the company repeatedly issued convertible securities to fund BTC purchases.

Meanwhile, Strategy’s market structure continues to give investors leveraged exposure to Bitcoin. The company’s amplification ratio remains high, while its mNAV ratio of 1.19 suggests the stock still trades at a premium relative to the value of its BTC reserves.

For now, Saylor’s Bitcoin buying machine may be paused, but few investors believe it has stopped entirely.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.