National Crypto Reserves: 2026 Global Policy Tracker

Share

Key Takeaways

National crypto reserves operate as formal policy in a small group of countries, led by the United States through its Strategic Bitcoin Reserve, alongside El Salvador’s treasury holdings and Bhutan’s state-linked bitcoin strategy.

Transparency separates credible reserves from political messaging, with El Salvador publishing on-chain treasury data while most other governments disclose little verifiable information.

Proposed reserves in Brazil, Japan, Poland, and Pakistan remain unresolved, as central banks and monetary authorities continue to resist treating bitcoin as a reserve asset.

Future reserve adoption will depend on custody standards, legal authority, and geopolitical pressure, as seen in U.S. seizure-based reserves and Russia’s crypto use in trade.

Governments used to treat crypto as a private-market experiment. That era ended.

By December 2025, a small group of countries moved from talk to policy, building national crypto reserves or stockpiles.

A larger group floated proposals, sparked debates, or triggered outright pushback from central bankers.

This article separates implemented national crypto reserve frameworks from proposed ones, and explains what changed, what still looks like political theater, and what risks taxpayers now carry.

What Counts as a “National Crypto Reserve” in 2025

A national crypto reserve can mean two different things, and the distinction matters.

A strategic reserve usually implies a long-term posture. Policymakers describe the digital asset as a reserve-like store of value, similar in concept to gold, and place limits on selling.

A stockpile usually implies custody and management of crypto the government already holds, often from seizures or enforcement actions, with fewer ideological claims.

The United States now uses both terms in official policy, which signals how governments try to balance pro-crypto messaging with legal realities.

Implemented National Crypto Reserves

Several governments moved beyond debate and into action by 2025. Instead of testing crypto through pilots or regulatory sandboxes, a small group of states formally integrated digital assets into national balance sheets. The United States set the tone with the most consequential move.

United States: Strategic Bitcoin Reserve And Digital Asset Stockpile

The biggest shift in 2025 came from Washington. On March 6, 2025, the White House issued an executive order establishing a Strategic Bitcoin Reserve (SBR) alongside a broader United States Digital Asset Stockpile.

The order treats Bitcoin (BTC) as a special category and separates it from other digital assets held by the federal government.

Public reporting added clarity on how the plan works in practice. The reserve would hold roughly 200,000 Bitcoin previously seized in criminal and civil cases, with the government ending routine sales of those holdings.

Reuters described the reserve as a “digital Fort Knox” concept and highlighted instructions to pursue budget-neutral acquisition strategies.

The shift signals a clear change in policy direction.

Policy stance: The U.S. moved from liquidating seized Bitcoin to holding it as a long-term strategic asset.

Asset distinction: Bitcoin received separate treatment from other digital assets, reinforcing its status as a reserve-grade instrument.

Global signal: The decision gave other governments political cover to consider similar reserve frameworks without appearing radical.

Key uncertainties remain. The executive order establishes structure, but credibility depends on execution.

Governance: Clear audit standards and public reporting determine whether the reserve functions as policy or symbolism.

Custody: Secure storage and operational controls shape trust in the system.

Transparency: Ongoing disclosures influence how markets and foreign governments interpret the reserve’s role.

While the U.S. framed bitcoin as a strategic reserve asset, another country went further by pairing treasury holdings with real-time public disclosure. El Salvador offers a contrasting model.

El Salvador: Treasury Bitcoin Holdings With A Live Public Tracker

El Salvador remains the clearest example of a small economy that turned bitcoin into a state-led experiment with ongoing accumulation.

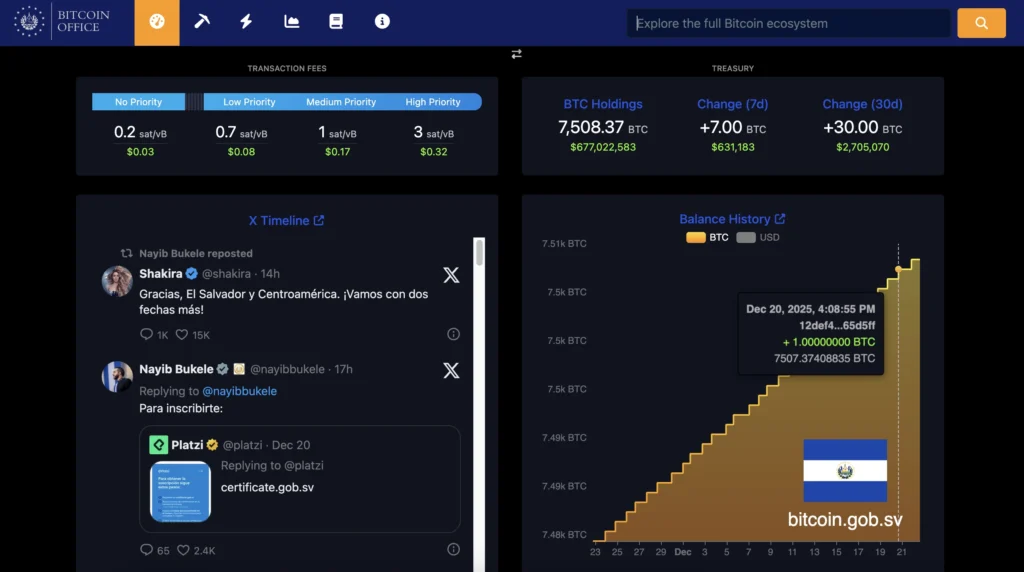

The country’s National Bitcoin Office runs a public “Bitcoin Explorer” that shows Treasury BTC Holdings and recent transactions.

Official Bitcoin portal | Source: National Bitcoin Office

In a snapshot from December 22, 2025, the tracker displayed 7,508.37 BTC in treasury holdings (with USD estimates that change with price).

The International Monetary Fund (IMF) has also documented the policy context, including the 2021 decision to grant bitcoin legal tender status and the broader economic discussion around adoption.

Why it matters: El Salvador moved beyond theory into daily reserve operations, and it publishes a public-facing holdings dashboard. That level of transparency remains rare in sovereign crypto policy.

What remains unclear: A public tracker does not answer the hardest questions. For example, how the government manages drawdown scenarios, how it measures reserve adequacy, and how it handles volatility in a crisis. The IMF has repeatedly highlighted macro and financial stability concerns around the broader adoption push.

El Salvador offers the first clear example of a small state turning bitcoin into public policy, using treasury accumulation and everyday payments to test how a digital asset fits into a national economy.

That experiment shows both the appeal and the limits of bitcoin at the state level. The next section turns to Bhutan, where Bitcoin adoption followed a very different path rooted in energy strategy and state-managed reserves rather than consumer use.

Bhutan: State-Linked Bitcoin Strategy And A New 10,000 BTC Pledge

Bhutan built a reputation in 2025 as the country most comfortable saying the quiet part out loud: crypto can fund the state.

Bhutan has invested in crypto since 2019 and used profits to help pay government salaries, while leaning on hydropower-powered mining as an economic strategy.

Then, as announced in December 2025, Bhutan launched a gold-backed token, TER.

Why it matters: Bhutan links bitcoin to national development finance, not only financial speculation. That framing fits a “reserve” mindset more than a short-term trade.

What remains unclear: Outside observers still struggle to verify full holdings and governance, even when blockchain analytics label wallets. Transparency still depends on what the government chooses to disclose.

Pakistan: Announced Government-Led Strategic Bitcoin Reserve

Pakistan moved from “watching crypto” to publicly signaling a strategic reserve narrative.

Reportedly, Pakistan’s policy conversation around crypto accelerated in 2025 through the Pakistan Crypto Council, with statements that included a national bitcoin reserve concept alongside energy allocation for mining and AI data centers.

A government-led strategic Bitcoin reserve was also announced, but publicly available information still lacks consistent detail on reserve size, custody structure, and reporting cadence.

Why it matters: Pakistan’s move signals that reserve talk no longer stays limited to wealthy countries. States with energy constraints and external financing needs now see bitcoin narratives as a potential strategic lever.

What remains unclear: Without published reserve addresses, audited holdings, and a legal framework, a “reserve” can remain a speech rather than an institution.

Not every government that talks about crypto reserves intends to hold them. Once the discussion moves away from seized assets and treasury balances, the political incentives change.

In many countries, reserve proposals function less as fiscal policy and more as signaling tools aimed at voters, markets, or industry groups.

Proposed National Crypto Reserves And Political Prototypes

Many proposals look serious on paper, but most still sit in early legislative, campaign, or “study phase” territory.

Brazil: A Formal Bill To Create A Sovereign Bitcoin Reserve

Brazil now has one of the most concrete legislative artifacts in the world: PL 4501/2024, which proposes forming a Reserva Estratégica Soberana de Bitcoins (Sovereign Strategic Reserve of Bitcoins) by the federal government.

Brazil’s Chamber of Deputies published explanatory coverage framing the proposal as a plan to diversify international reserve assets through crypto purchases, with discussion centered on allocating up to 5% of Brazil’s $344 billion in reserves to bitcoin.

Why it matters: This is a concrete, traceable bill with a public record and an official legislative trail.

What remains unclear: Central bank alignment and macro guardrails. Reserve policy often lives in the tension between elected officials and monetary technocrats. Brazil’s next steps will show which side holds veto power.

It is important to note that Brazil’s central bank is preparing a comprehensive crypto regulatory framework scheduled for February 2026, which may influence how reserve-related proposals are evaluated and implemented.

Japan: Lawmaker Pushes for A Strategic Bitcoin Reserve Discussion

Japan’s reserve currency exists, but primarily as a form of political signaling.

Japanese Diet member Satoshi Hamada proposed kick-starting discussions around a national bitcoin reserve.

Why it matters: Japan holds one of the world’s largest pools of foreign exchange reserves. Even a symbolic debate moves the global narrative.

What remains unclear: The gap between “proposal to discuss” and “institutional reserve policy” can last years in Japan’s system.

Japan’s case shows how reserve discussions can influence global perception without producing immediate policy. In other countries, however, the line between proposal and practice has already begun to blur.

Russia: Proposal Talk, Plus Real-World Crypto Use In Trade

Russia sits in a unique category: public reserve proposals exist, and actual crypto usage in international trade has also surfaced.

In 2024, a Russian lawmaker proposed creating a strategic Bitcoin reserve.

According to reports, Russia has started using Bitcoin and other cryptocurrencies in foreign trade under an experimental legal regime, driven in part by sanctions pressure.

Why it matters: Russia illustrates a pattern: states under external financial pressure experiment first with payments and settlement, then wrap the narrative in “reserve” language.

What remains unclear: A trade-use regime does not equal a formal reserve. The direction of travel looks real, but reserve governance remains unresolved.

Russia’s experience highlights how external pressure can accelerate real-world crypto use before governance frameworks follow. In Europe, the response to reserve talk moved in the opposite direction.

Czech Republic: A Proposal That Triggered Immediate Central Banker Pushback

If 2025 had a single “red line” moment for Europe, this was it.

Notably, European Central Bank (ECB) President Christine Lagarde rejected the idea of Bitcoin in official reserves after comments tied to Czech National Bank Governor Aleš Michl, emphasizing central bank reserves need liquidity, security, and safety.

Why it matters: Europe’s institutional stance remains broadly hostile to the idea of bitcoin in central bank reserves, even when individual officials test the waters.

What remains unclear: Europe’s position could still evolve through political channels, but the ECB message signals a high barrier.

While European institutions have drawn firm lines, political actors in some countries still use reserve rhetoric as a campaign signal rather than a policy commitment.

Poland: Campaign Promise, Not State Policy

Poland’s “strategic Bitcoin reserve” talk remains tied to political campaign rhetoric.

Presidential candidate Sławomir Mentzen of the Confederation party pledged on social media that he would create a Strategic Bitcoin Reserve if elected in May 2025, describing the idea as part of a broader plan to make Poland a “cryptocurrency haven” with supportive regulation and low taxes.

Poland should create a Strategic Bitcoin Reserve.

If I become the President of Poland, our country will become a cryptocurrency haven, with very friendly regulations, low taxes, and a supportive approach from banks and regulators.

Mentzen’s campaign framing did not translate to an institutional reserve policy, and his bid finished third in the first round with about 14.8 % of the vote.

Why it matters: Political branding can normalize the concept, even when central banks resist.

What remains unclear: Election promises do not automatically translate into reserve mandates, especially in systems with strong central bank independence.

Poland shows how reserve language can circulate through electoral politics without touching state balance sheets. In other cases, however, crypto policy has moved faster than institutions could absorb the risks.

A Warning Case: Central African Republic’s Crypto Politics And State Asset Risk

The Central African Republic (CAR) does not fit neatly into “implemented reserve” versus “proposed reserve,” but it shows what can go wrong when crypto becomes state ideology without credible governance.

A watchdog warned that opaque crypto ventures in CAR could endanger state assets, citing concerns around tokenization ideas and weak transparency.

Why it matters: Reserve policy requires boring, enforceable rules. When a government treats crypto as a political identity project, corruption risk rises and credibility drops.

The Central African Republic highlights what happens when reserve narratives outrun institutional capacity.

Across countries, the same underlying forces keep pushing crypto into reserve debates, even when outcomes diverge sharply.

National Crypto Reserves: Implemented vs. Proposed

The table below summarizes how countries differ in their approach to national crypto reserves. It separates governments that have implemented formal reserve or stockpile frameworks from those where proposals remain political, legislative, or unresolved.

Country

Status

Asset type

Acquisition source

Governance clarity

Transparency level

Key risk

United States

Executive order passed

Bitcoin, other digital assets

Criminal and civil seizures

Executive order framework

Medium

Political reversal

El Salvador

Implemented

Bitcoin

Treasury purchases

Centralized executive control

High

Price volatility

Bhutan

Implemented

Bitcoin

State mining, accumulation

State-linked entities

Medium

Limited disclosure

Pakistan

Announced

Bitcoin

Undisclosed, policy stage

Early institutional setup

Low

Policy uncertainty

Brazil

Proposed (bill)

Bitcoin

Planned market purchases

Legislative process ongoing

Medium

Central bank opposition

Japan

Proposed (discussion)

Bitcoin

Not defined

Political debate only

Low

Institutional resistance

Russia

Proposed plus trade use

Bitcoin

Trade settlement, unclear

Fragmented authority

Low

Sanctions exposure

Czech Republic

Rejected proposal

Bitcoin

Not applicable

Central bank veto

High

Policy deadlock

Poland

Campaign proposal

Bitcoin

Not defined

Electoral rhetoric

Low

Non-binding pledge

Central African Republic

Failed experiments

Tokens, crypto assets

State-backed initiatives

Weak institutional controls

Very low

Asset misuse

The table highlights a clear pattern across jurisdictions: the biggest risks do not come from crypto itself, but from weak governance and political instability around reserve policy.

Countries with implemented frameworks face market and credibility risks, such as price volatility or leadership changes, but they at least operate within defined structures.

In contrast, countries still in the proposal or campaign phase carry higher institutional risk, where reserve narratives can shift quickly, stall indefinitely, or collapse under central bank resistance.

Another takeaway centers on transparency gaps. El Salvador stands out for publishing on-chain treasury data, while most other governments provide limited or no verifiable disclosure.

Low transparency amplifies concerns around asset misuse, off-balance-sheet handling, and public trust, especially in countries with weaker oversight mechanisms.

These risks point to a broader question that goes beyond individual country cases: why are governments even considering crypto reserves now?

What Drives Crypto Reserve Politics in the Future

Future reserve politics will likely center on strategic optionality rather than full monetary transformation. Governments will weigh whether holding digital assets provides flexibility during financial stress, sanctions, or liquidity shocks, without committing to wholesale currency change.

Reserve decisions will reflect risk management logic more than ideology.

Technology and custody maturity will also shape policy. As institutional-grade custody, auditing standards, and on-chain transparency improve, resistance based on operational risk may soften. Governments tend to move once asset management resembles familiar reserve infrastructure.

Finally, domestic political cycles will continue to influence reserve narratives. Crypto reserves already function as signaling tools during elections and policy debates.

Over time, only countries that translate political messaging into durable legal frameworks will treat digital assets as credible components of sovereign reserves.

The shift in 2025 proves that sovereign crypto is no longer an “all-or-nothing” bet on a new world order. Instead, it has become a pragmatic tool for strategic optionality.

Whether it’s the U.S. protecting seized assets or Bhutan tokenizing gold, the goal is the same: building a digital safety net. For 2026, the winners won’t be the countries with the most coins, but those with the clearest laws.

A national crypto reserve refers to crypto assets formally designated for long-term state custody under an explicit legal or policy framework, not assets held incidentally or temporarily.

Can crypto reserves affect a country’s credit rating?

Crypto reserves can influence credit assessments if they increase balance sheet volatility or weaken reserve liquidity, especially in countries with limited fiscal buffers.

Are crypto reserves treated the same as gold reserves?

Crypto reserves differ from gold reserves because they lack universal monetary acceptance, face higher price volatility, and rely on digital custody rather than physical control.

Could international regulators restrict crypto reserves?

International regulators could indirectly limit crypto reserves by tightening capital rules, custody standards, or reserve asset eligibility for central banks and sovereign funds.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Lorena Nessi is an award-winning journalist and media technology expert with 15 years of experience in digital culture and communication. Based in Oxfordshire, UK, she combines academic insight with hands-on media practice.

She holds a PhD in Communication, Sociology, and Digital Cultures, and an MA in Globalization, Identity, and Technology.

Lorena has taught at Fairleigh Dickinson University, Nottingham Trent University, and the University of Oxford. She is a former producer for the BBC in London, with additional experience creating television content in Mexico and Japan.

Her research focuses on digital cultures, social media, technology, capitalism, and the societal impact of blockchain innovation.

She has written extensively on digital media and emerging technologies, with her work featured in both academic and media platforms. Her Web3 expertise explores how blockchain technologies shape culture, economics, and decentralized systems.

Outside of work, Lorena enjoys reading science fiction, playing strategic board games, traveling, and chasing adventures that get her heart racing. A perfect day ends with a relaxing spa and a good family meal.

Easy

Easy