From prison, the former CEO has put forward a striking claim.

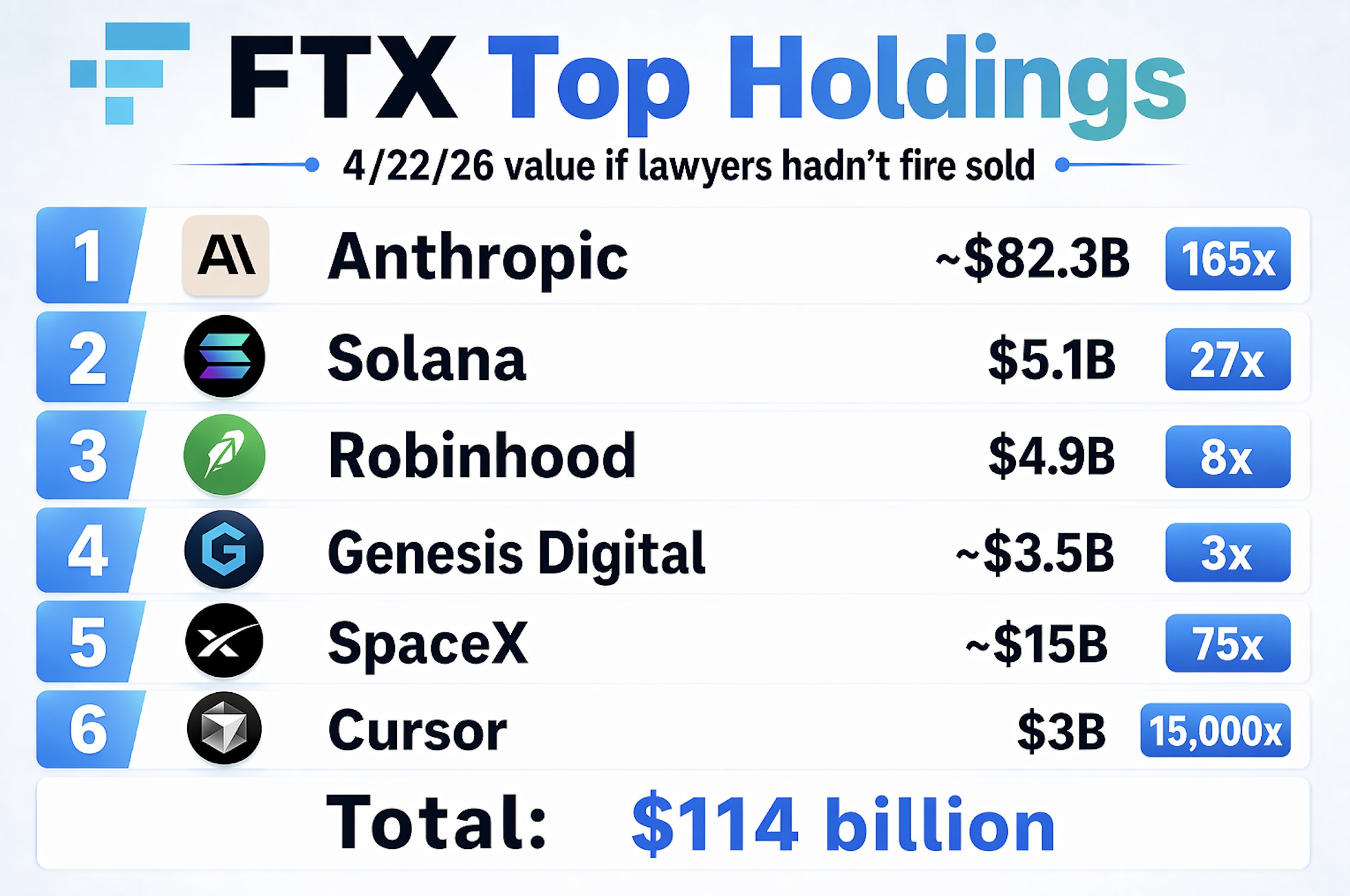

If FTX’s bankruptcy team had simply held onto its venture bets and crypto positions instead of selling them, the estate could now be worth as much as $114 billion.

It’s a headline-grabbing number—and one that taps into a familiar frustration in crypto markets: selling too early.

But behind the claim lies a more complicated story about risk, timing, and the original decisions that brought FTX down in the first place.

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

SBF’s argument hinges on a simple idea: FTX’s early investments proved extraordinarily valuable, yet the bankruptcy process failed to capture that upside.

He points to a portfolio that included stakes in Anthropic, Solana, Robinhood, Genesis Digital Assets, SpaceX, and the AI coding startup Cursor.

Using current valuations, the combined total reaches roughly $114 billion.

FTX investments in startups early in 2022-23. Credit: SBF on X.

The numbers, on paper, are striking.

Anthropic alone accounts for the bulk, now valued at about $82.3 billion—representing a roughly 165x return on FTX’s original investment.

SpaceX, based on updated private-market valuations, contributes an estimated $15 billion.

Solana’s recovery pushes its position to around $5.1 billion, while Robinhood and Genesis Digital add several billion more.

Even smaller bets tell the same story. Cursor, once a negligible seed investment, now carries a multi-billion-dollar valuation.

Taken together, the figures suggest enormous upside—if, and only if, those assets had been held through years of volatility.

The new leadership team, led by restructuring veteran John J. Ray III, faced a clear mandate: stabilize the estate, reduce risk, and return funds to creditors as quickly as possible.

That meant selling.

Major holdings were gradually liquidated throughout 2023 and 2024.

The Anthropic stake, originally around $500 million for an 8% position, was sold in two stages for a total of roughly $1.3 billion to $1.4 billion.

At the time, it represented a solid return—well before the AI boom dramatically inflated valuations.

Solana holdings followed a structured over-the-counter process.

More than 41 million locked tokens were sold in tranches, often at discounted prices to avoid disrupting the market.

During those sales, SOL traded between $20 and $60—far below today’s levels.

Other positions, including Robinhood shares, Genesis Digital Assets exposure, and smaller venture bets, were also liquidated at prevailing market prices.

By mid-2024, most of the estate’s volatile assets had been converted into cash.

SBF’s $114 billion figure relies on a version of events where everything goes right.

Markets recover. Private valuations surge. Illiquid assets become liquid at peak prices. And, crucially, creditors are willing to wait through years of uncertainty.

That wasn’t the situation facing the bankruptcy team.

At the time of the collapse, crypto markets were still falling.

Confidence was low, regulatory pressure was high, and holding large, concentrated positions in volatile or illiquid assets posed significant risks.

A prolonged downturn could have erased much of the estate’s value.

Bankruptcy law doesn’t reward speculation. It prioritizes certainty.

Advisors are tasked with preserving value, not chasing it.

Selling early may have capped potential upside, but it also avoided the possibility of deeper losses.

In that context, the liquidation strategy followed standard practice.

FTX’s Deeper Issue

The debate over missed gains risks overlooking a more fundamental point.

Prashant Jha is a seasoned crypto journalist based in Delhi, India, with a Bachelor’s Degree in Computer Science Engineering. Passionate about the evolving world of blockchain and cryptocurrencies, he has been a dedicated voice in the industry since 2018. Prashant’s expertise lies in regulatory reporting, where he unravels complex legal and financial developments with clarity and precision. Before joining CCN in 2024, he honed his craft at Cointelegraph, establishing himself as a trusted name in crypto journalism.

His coverage spans major industry events, including the high-profile collapses of FTX, Three Arrows Capital (3AC), and LUNA, offering readers insightful analyses of their regulatory and market implications. Prashant’s technical background enables him to bridge the gap between intricate blockchain technology and its real-world applications, making his work accessible to novices and experts.

Beyond his professional pursuits, Prashant is an avid music enthusiast, often exploring diverse genres to unwind. A sports lover, he has a particular passion for cricket and frequently engages in discussions about the game. His multifaceted interests and sharp journalistic instincts make him a valuable contributor to CCN, where he continues shaping the crypto landscape's narrative.