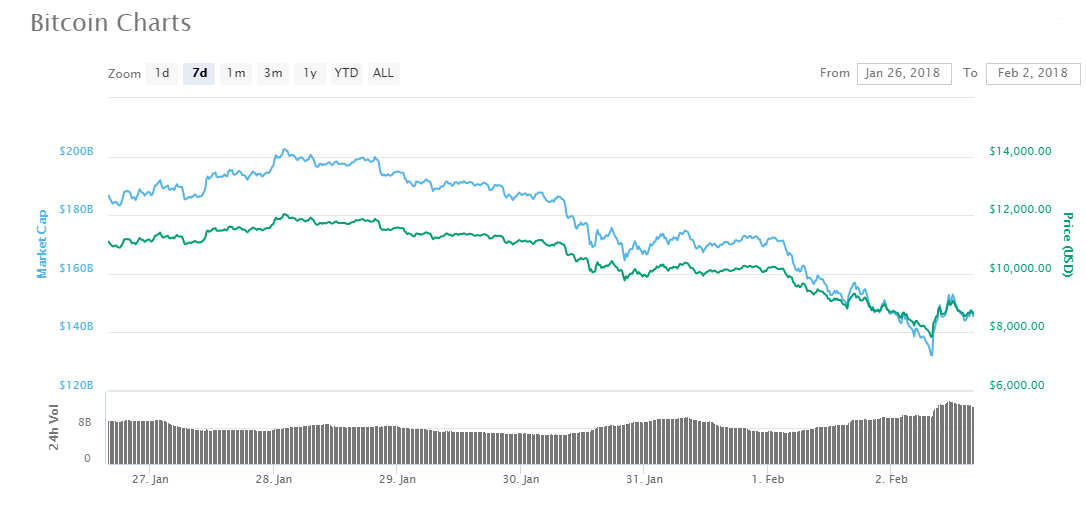

The top two US banks took what little wind was left in investors’ sails today. JPMorgan Chase and Bank of America have both placed a ban on cryptocurrency transactions via credit cards, according to Bloomberg reports. The bitcoin price is holding at about a 5.75% decline, trading at $8,589 in what is shaping up to be a rocky 2018 for cryptocurrency trading so far.

JPMorgan, whose CEO Jamie Dimon famously denounced bitcoin a few months back, doesn’t want to inherit the credit risk given the volatility in the bitcoin price. By speculating on the price of a highly volatile investment like bitcoin, investors are exposing the bank to a higher risk of default, a scenario that may not have been present when the credit was extended in the first place. Meanwhile, banks and regulators are working in tandem to detect signs of fraud, and taking credit cards out of the equation simplifies things somewhat.

JPMorgan’s ban goes into effect on Saturday, Feb. 3, while Bank of America’s ban became effective immediately, with the bank declining credit card transactions with crypto exchanges, as per internal memos obtained by Bloomberg. While personal and business B-of-A credit cards are included in the ban, the bank will continue to honor all debit card transactions with cards issued by the bank.

The move no doubt has investors scrambling, some of whom have automatic buy orders in place at exchanges. And it places an immediate hurdle in bitcoin’s move toward the mainstream, as potential investors who may have been weighing the field now have another hoop to jump through to gain exposure to cryptocurrencies.

But by the same token, if what’s going to move bitcoin and other cryptocurrencies forward is investors “not investing more than they can afford,” than the bank ban becomes less of a hurdle and more of an inconvenience.

Meanwhile, Chase and B-of-A aren’t the first banks to move on bitcoin. Discover and Capital One already ruled out cryptocurrency charges, while Citi appears to be on the fence.

But for Discover’s chief executive David Nelms, there may be some wiggle room. Discover has banned cryptocurrency transactions because the only use cases Nelms is witnessing today are for ransomware and money laundering. But he stopped short of writing bitcoin off, telling Bloomberg that what could inspire a shift is customer demand.

So perhaps in this early stage of loose regulation governing the cryptocurrency space, it’s prudent for banks to take a step back so the industry can move forward.

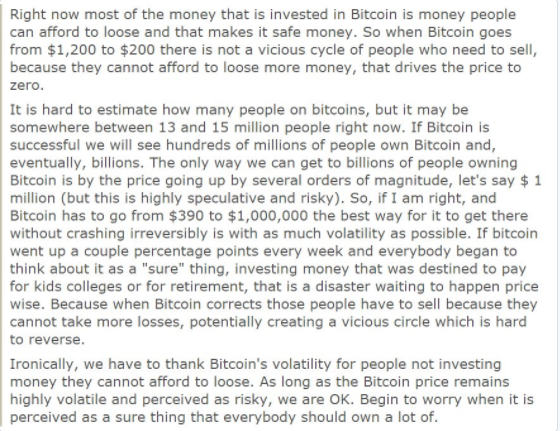

In the words of Wences Casares, chief executive of Xapo –

Featured image from Shutterstock.

Gerelyn is Assistant Editor at CCN. Based in the U.S., she has also covered institutional investing on Wall Street but caught the bitcoin bug soon after. She resides 13 miles outside of New York, close enough but also far enough away to escape it all. Follow her on Twitter or email [email protected].