Data analysis shows USOR does not track U.S. oil reserves or crude prices. Learn how it compares with regulated oil ETFs and discover major tracking failures. | Credit: CCN.com

Share

Key Takeaways

USOR is a Solana-based crypto token, not a regulated commodity or oil-backed asset, despite marketing claims referencing U.S. oil reserves.

Oil ETFs provide regulated exposure to crude prices through futures and custodial structures, with SEC oversight, audits, and investor protections.

USOR price action does not correlate with physical oil prices, behaving more like a political or meme-style token than a commodity proxy.

Tokenizing U.S. strategic oil reserves would require legislation, audits, custody agreements, and regulatory approval, none of which exist for USOR.

Crypto markets have always thrived on narratives, but in early 2026, one story stood out for how aggressively it blurred the line between blockchain speculation, real-world commodities, and political symbolism.

The rise of the U.S. Oil Reserve (USOR) token on Solana reignited debates about whether crypto can truly tokenize physical assets, or whether some projects merely borrow the language of traditional finance to manufacture hype.

At the same time, oil ETFs remain one of the most established, regulated ways to gain exposure to crude prices. Comparing USOR to oil ETFs reveals a stark contrast between on-chain narrative-driven tokens and regulated commodity instruments built on legal and institutional foundations.

Below, CCN breaks down the differences: factually, mechanically, and legally.

What Is the USOR Token and How Does It Claim Exposure to US Oil Reserves?

USOR (U.S. Oil Reserve) is a Solana-based SPL token marketed as a tokenized oil reserve. The project’s messaging suggests that USOR represents exposure to U.S. oil, with claims that reserves are “government-verified” and held under federal custody.

Trading venues: Solana DEXs such as Meteora and aggregators

Custody: Self-custodied via crypto wallets

What USOR does not provide is legal documentation proving ownership, entitlement, or redemption rights tied to physical oil.

Importantly, blockchain data can only verify token transfers, not off-chain assets. Without legally binding attestations, USOR’s oil narrative remains a marketing claim rather than a verified financial structure.

How Do Oil ETFs Provide Exposure to Crude Oil Prices?

Oil ETFs offer exposure to crude oil through regulated financial mechanisms, not physical barrels held for retail investors. Most oil ETFs track oil prices via:

Custodians and clearinghouses operating under financial regulation

Examples include ETFs listed on U.S. exchanges that file prospectuses, disclose risks, publish holdings, and operate under SEC oversight. While ETFs can be affected by issues such as contango or roll costs, their structures are transparent and enforceable.

Crucially, oil ETFs are not ambiguous about what they represent: price exposure, not direct ownership of oil reserves.

Is USOR Actually Backed by Physical Oil or Reserves?

There is no verified evidence that USOR is backed by physical oil or U.S. strategic reserves.

Key facts:

The U.S. Department of Energy (DOE) manages the Strategic Petroleum Reserve.

No DOE or U.S. government statement authorizes tokenization via a private crypto token.

Claims of the Federal Reserve‘s involvement are inaccurate; the Fed does not store oil.

Without legal custody agreements, audits, or redemption mechanisms, USOR cannot be considered oil-backed in any institutional sense. At best, it is an oil-themed crypto token, not a tokenized commodity.

Regulation Comparison: Crypto Tokens vs SEC-Regulated Oil ETFs

The regulatory divide between USOR and oil ETFs is fundamental.

This distinction matters because regulation defines rights, recourse, and accountability. ETFs operate within enforceable legal frameworks; USOR does not.

Liquidity and Market Depth: Can USOR Match ETF Trading Volume?

USOR’s liquidity exists primarily on Solana DEXs, where thin order books can amplify volatility.

Even modest inflows can cause sharp price spikes, while exits can drain liquidity quickly.

Liquidity depth allows ETFs to absorb large trades without extreme price distortion. USOR’s liquidity is fragile by comparison, dependent on sentiment rather than structural demand.

Price Correlation: Does USOR Really Track Oil Prices?

Brent and WTI crude were down double digits year-over-year

This divergence reveals the core issue: USOR trades like a political or narrative-driven token, not a commodity proxy. Traders price headlines, influencer activity, and social momentum, not barrels of oil.

Oil ETFs, while imperfect, show far stronger correlation to underlying crude benchmarks.

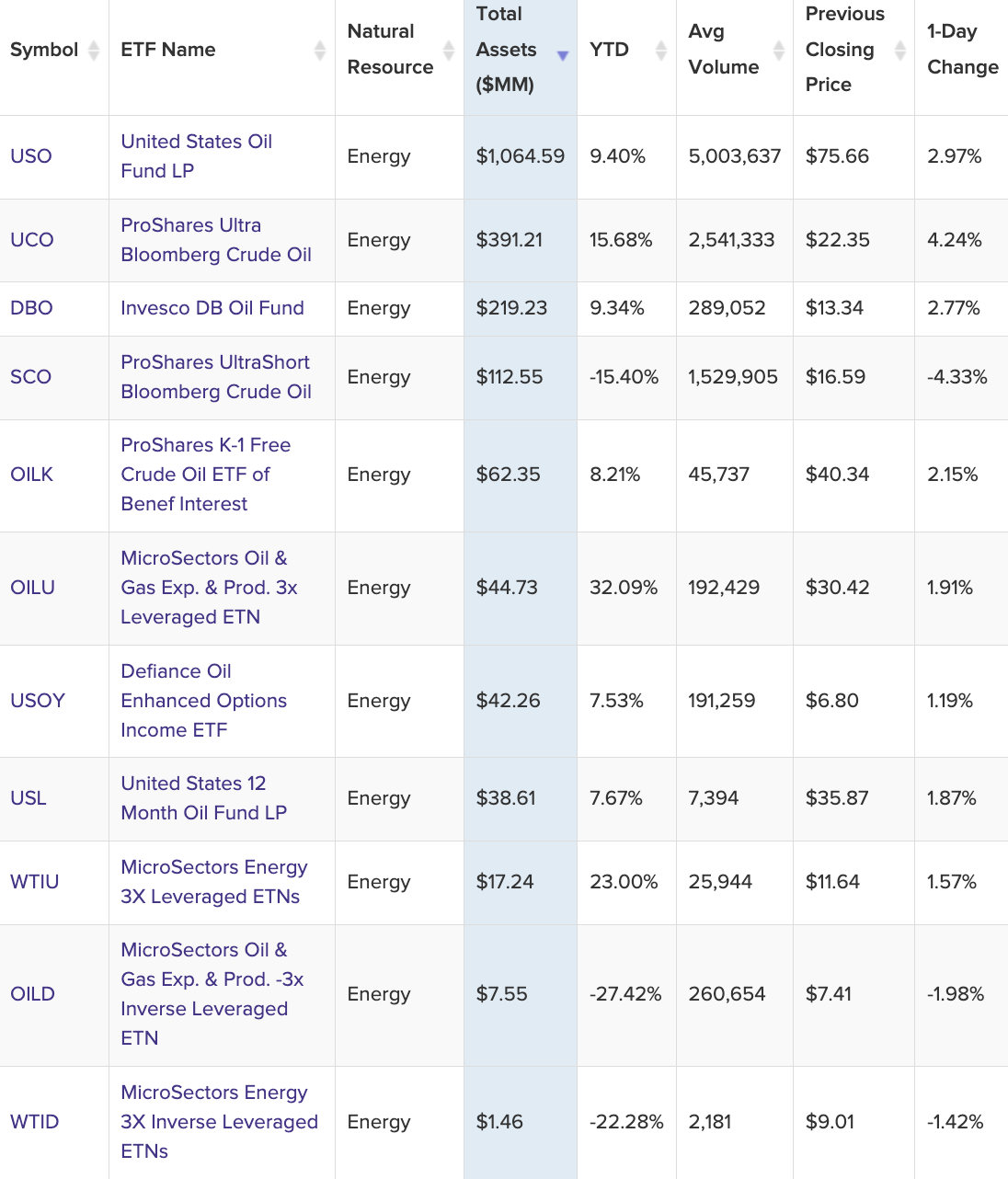

The data shown in the chart below was collected using the CoinGecko API, which provides market prices from cryptocurrency exchanges where USOR is traded. The time range covers January 13 to January 28, 2026, with roughly hourly price observations. This means the chart reflects actual trading prices from crypto markets, not official oil benchmarks or futures settlement prices.

While this is useful for understanding how USOR trades in real conditions, it also means the data is influenced by crypto-specific factors such as exchange liquidity, trader behavior, and short-term speculation.

$USOR price with rolling band and anomalies. | Credit: Python analysis based on CoinGecko data

Stable Phase

During the early part of the period (around Jan 13–19), the data shows a slow and steady upward trend in the blue line (actual hourly USOR price), with relatively small hour-to-hour changes. In this phase, the price remains close to the orange line (rolling 24-hour average) and stays within the green and red bands (±2 standard deviations from the average).

This indicates that trading was relatively calm and that price movements were consistent with recent history. This is the kind of behavior users might expect from an asset that is meant to track something like oil, where prices usually adjust gradually rather than violently.

Extreme Spike

However, around January 20–21, the blue price line shows a sudden and extreme surge followed by a sharp drop. The price increases several times over within a very short period and then rapidly falls.

During this time, the price moves far above the green upper band (+2σ) and later toward or below the red lower band (−2σ), which means it is far outside what recent volatility would consider normal. These moments are highlighted by the blue anomaly markers (points where the price is more than 3 standard deviations away from the rolling average).

Such behavior is highly abnormal for an oil-linked product. Real oil prices, even during major geopolitical or supply shocks, do not typically multiply within hours and then immediately reverse. This strongly suggests that the movement was driven by crypto market dynamics, such as low liquidity, large individual trades, momentum buying, or speculative behavior, rather than by changes in actual oil market fundamentals.

Tracking Failure

This creates a serious disconnect from real oil prices. If USOR were closely tracking oil, large moves would usually be tied to persistent news and would show smoother adjustments over several days, not sharp pump-and-dump-style patterns.

The fact that the spike is brief and followed by a quick correction suggests that the price was temporarily pushed far away from any oil-based reference value and then snapped back once speculative pressure faded. This means users trading during that window could experience large gains or losses that have nothing to do with real oil price movements, undermining confidence in the product as a commodity proxy.

Speculative Drivers

Another concerning aspect is that after the spike and crash, the blue price line does not return to its earlier smooth pattern around the orange rolling mean. Instead, the price continues to swing more widely, often approaching the statistical bands more frequently than before.

This indicates that volatility remains elevated, suggesting a change in market regime. It implies that the event may have altered who is trading the token, how liquid the market is, or how sensitive the price is to trades, further weakening its reliability as a stable oil-tracking asset.

For users, this increases uncertainty because even after the major shock has passed, price behavior remains harder to predict and less connected to underlying commodity dynamics.

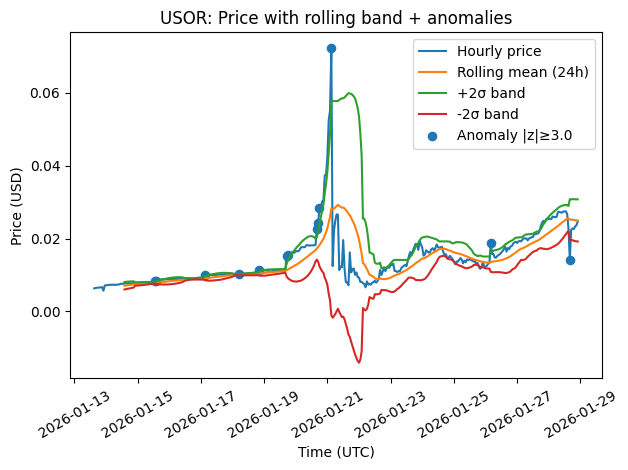

Evidence of Sudden and Severe Market Stress in $USOR Trading

The below chart shows that USOR’s hourly returns are usually close to zero, indicating small, stable price changes, but around January 20-21 there is a cluster of very large positive and negative spikes, meaning the price was jumping up and down violently within hours.

Hourly return shocks. | Credit: Python analysis based on CoinGecko data

The blue dots mark statistically extreme return shocks (|z| ≥ 3), which are rare under normal conditions and signal abnormal market stress or speculative activity. The concentration of these shocks in a short time window suggests a brief but intense period of instability, where traders could experience sudden gains or losses that are not consistent with normal oil-like price behavior.

Overall, the data reveals how USOR actually behaves in live markets rather than how it is supposed to behave in theory. The extreme spike, rapid reversal, and persistent volatility strongly suggest that USOR’s price can become decoupled from real oil prices, exposing users to risks more similar to speculative crypto assets than to traditional commodity instruments.

This is concerning for anyone using USOR for hedging, diversification, or as a substitute for oil ETFs or futures, since the token may fail to provide the stable, oil-linked exposure that users expect.

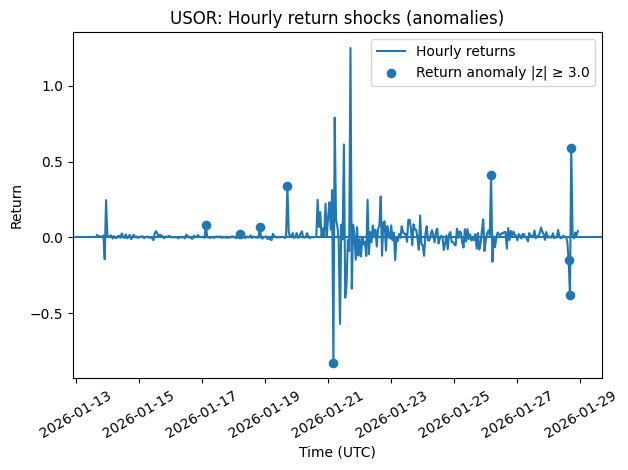

USO Daily Returns and Shock Days Explained

United States Oil Fund LP (USO) is an ETF that tracks oil prices using oil futures contracts, and it usually moves slowly and steadily, not with big sudden spikes like many crypto assets.

The below chart shows how much the USO ETF price changes each day, expressed as a percentage (daily return). Most of the line stays close to zero, which means that on most days, USO moves only a little up or down — this is normal for an oil ETF that tracks commodity futures.

Daily returns and shock days. | Credit: Python analysis based on Yahoo Finance data

The blue dots mark “shock days,” which are days when the return is unusually large compared to recent history. Even on these shock days, the size of the moves is still relatively small (around ±2% to ±4%), showing that USO remains fairly stable and does not experience extreme jumps or crashes within a single day. This reflects how traditional oil markets usually behave: prices change gradually and are influenced by news, supply, and demand rather than sudden speculative spikes.

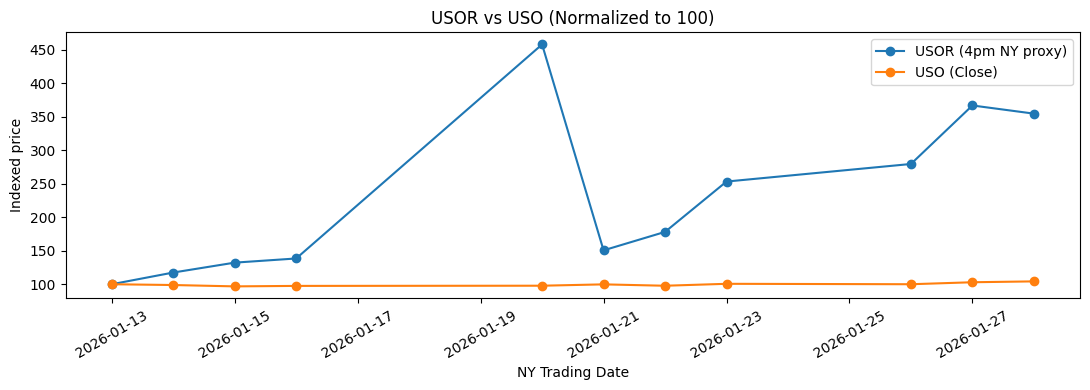

USOR vs USO Performance and Return Behavior Comparison

This analysis compares both the overall price movement and the daily return behavior of USOR and the USO oil ETF.

When both prices are normalized to start at 100, the USO line remains close to that level, showing only small changes over time, which is typical for an oil-tracking ETF.

USOR vs. USO. | Credit: Python analysis based on CoinGecko and Yahoo Finance data

In contrast, USOR rises very sharply to more than four times its starting value, then drops and rises again, indicating extremely high volatility. If USOR were closely tracking oil prices, its performance line would look similar to USO’s, but instead there is a large and persistent gap between them, showing poor tracking of traditional oil markets.

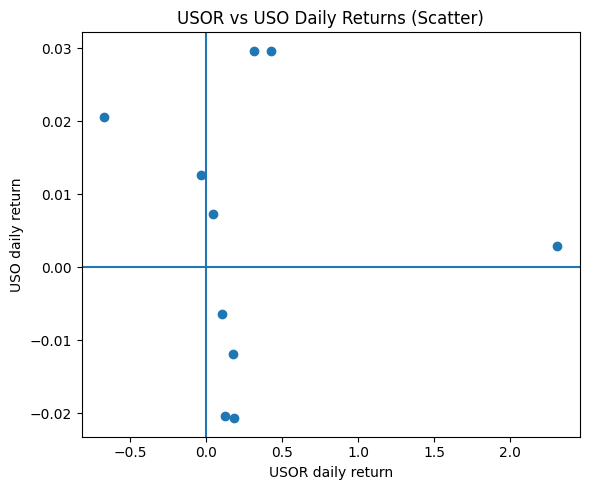

The daily returns comparison reinforces this result. If USOR and USO were driven by the same oil market forces, their daily percentage changes would move together and form a diagonal pattern on the scatter plot.

USOR vs. USO daily returns. | Credit: Python analysis based on CoinGecko and Yahoo Finance data

Instead, the points are widely scattered, meaning that large moves in USOR often happen when USO barely changes. This shows that USOR’s price is influenced more by crypto-specific factors such as liquidity conditions and speculative trading rather than by real oil price movements, making it a much riskier and less reliable proxy for oil exposure.

What Would It Take to Legally Tokenize US Strategic Oil Reserves?

A legitimate tokenization of U.S. oil reserves would require:

Even large institutions struggle to tokenize commodities at this scale. The idea that a sovereign reserve could be tokenized through an anonymous Solana token is structurally implausible.

Smart Contract and Custody Risks in USOR vs Custodial Risks in ETFs

USOR carries smart contract and on-chain custody risks that are fundamentally different from the custodial and regulatory risks of traditional ETFs like USO.

With USOR, users rely on blockchain smart contracts to mint, transfer, and possibly stabilize the token; if there is a bug, exploit, oracle failure, or governance attack, funds can be lost or prices can become distorted with little immediate recourse. Users also self-custody or depend on crypto wallets and exchanges, which adds risks like private-key loss, hacks, or chain outages.

In contrast, ETFs are held through regulated brokers and backed by custodians that store futures contracts or cash under strict financial rules, audits, and investor protections. While ETFs still face risks (such as counterparty exposure and tracking error), they do not face smart-contract exploits or blockchain failures.

This means USOR users are exposed to technical and protocol-level risks on top of market risk, whereas ETF investors mainly face financial and custodial institution risks, which are generally more transparent and regulated.

While ETFs are not risk-free, their risks are disclosed and regulated. USOR concentrates technical, governance, and market risks with no formal safeguards.

Tax Treatment and Reporting Differences Between Crypto Tokens and Oil ETFs

Oil ETFs operate within well-established tax and reporting frameworks, particularly in the U.S. and Europe. Brokerage platforms automatically track cost basis, realized gains, and losses, and provide standardized tax documents to investors. This reduces compliance risk and administrative burden, making ETFs easier to manage for both retail and institutional investors.

In most jurisdictions, the capital gains treatment for ETFs is clearly defined, with long-standing guidance on holding periods, reporting thresholds, and loss offsetting.

Crypto tokens like USOR, by contrast, place far more responsibility on the individual holder:

Self-reporting is required, including tracking every trade, swap, or liquidity interaction.

Tax classification may be unclear, especially for tokens marketed as commodity-linked or real-world asset proxies, creating uncertainty around whether gains are treated as capital gains, income, or something else.

Cross-chain and DeFi activity can complicate record-keeping, increasing the risk of errors or omissions.

Regulatory interpretations are still evolving, meaning past compliance assumptions could change retroactively.

For many investors, especially institutions, funds, and high-net-worth individuals, tax certainty and auditability are non-negotiable. Even if a crypto token offers higher short-term upside, unclear tax treatment and reporting obligations can outweigh potential returns.

In this context, the simplicity and predictability of ETF taxation remain a major structural advantage over on-chain, narrative-driven assets like USOR.

Which Is Better for Investors: USOR or Traditional Oil ETFs?

The answer depends on what the investor seeks.

If the goal is regulated exposure to oil prices, oil ETFs are structurally superior.

If the goal is speculative trading driven by narratives, USOR may offer volatility, but with outsized risk.

According to the on-chain evidence, USOR is not an oil-backed asset. It is a crypto token leveraging oil symbolism. Oil ETFs are not perfect instruments, but they are transparent, regulated, and legally enforceable.

The broader lesson is not about rejecting tokenization, but about demanding evidence, audits, and accountability. Tokenization without legal backing is not innovation; it is storytelling.

In markets where hype travels faster than verification, distinguishing between on-chain activity and real-world exposure has never been more important.

No. There is no legal, governmental, or institutional evidence that USOR is backed by U.S. oil reserves. The U.S. Department of Energy, which manages the Strategic Petroleum Reserve, has issued no authorization or confirmation supporting the token’s claims.

Does USOR give ownership or redemption rights to physical oil?

No. Holding USOR does not grant ownership of oil, rights to barrels, or the ability to redeem tokens for physical crude or cash equivalents.

Why are people comparing USOR to oil ETFs?

Both are marketed as ways to gain exposure to oil-related themes. However, oil ETFs provide regulated price exposure through futures or derivatives, while USOR is an unregulated crypto token driven largely by narrative and speculation.

Is BlackRock involved in USOR?

There is no verified evidence of BlackRock involvement. Claims are based on heuristic wallet labels and social media speculation, not official disclosures or filings. BlackRock’s publicly tracked on-chain holdings do not include USOR.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy