Tom Lee’s BitMine (BMNR) Falls 81% Despite Holding 3% of ETH Supply — What Went Wrong?

Share

Key Takeaways

BitMine holds about 3.63 million ETH, nearly 3% of Ethereum’s supply, making it the largest corporate holder of ETH.

As ETH prices dropped, the company recorded over $4 billion in unrealized losses, and dilution eroded investor confidence.

Low staking yields, reliance on equity funding, and the collapse of the NAV premium exposed flaws in BitMine’s “digital asset treasury” strategy.

Analysts say BitMine’s future depends on Ethereum’s rebound and its ability to build real, diversified revenue streams.

In early 2025, BitMine Immersion Technologies (NASDAQ: BMNR) transformed from a small immersion-cooling crypto-mining company into one of the most aggressive corporate buyers of Ethereum (ETH) in history.

Under the leadership of Tom Lee, the well-known Fundstrat co-founder and crypto strategist, BitMine aimed to create an “Ethereum super-treasury,” mirroring the Bitcoin-centric playbooks of Strategy (MSTR).

However, by late November 2025, BitMine’s stock had collapsed over 81% from its peak, even as the firm continued to acquire ETH. The story of this rise and fall reflects the risks of concentration, timing, and investor sentiment in the digital-asset market.

Timeline: How BitMine’s 2025 Ethereum Treasury Strategy Unfolded

BitMine’s Ethereum-centric pivot happened quickly, capturing early market excitement before macro and crypto-specific headwinds turned sentiment.

Here’s a concise timeline of the company’s major 2025 milestones and market reactions:

Date (2025)

Event

Details & Impact

March 2025

Strategic Pivot Announced

BitMine announced plans to build a massive Ethereum treasury, targeting up to 5 % of total ETH supply. Stock surged >200 % in two weeks as investors welcomed the shift.

April – June 2025

Aggressive ETH Accumulation

Acquired 1.5 million ETH using equity financing. Average cost estimated $2,800–$3,000 per ETH.

July 2025

Tom Lee Appointed Chairman

Lee formally took leadership, signaling institutional ambition. Investor optimism peaked.

August 2025

ETH Holdings Cross 3 Million

Holdings reached 3.2 million ETH (2.7 % of supply). ETH price fell $3,400 → $2,600; BMNR dropped 35 %.

September 2025

Unrealized Losses Surface

Estimated paper losses > $2.8 billion as ETH traded below cost basis. Analysts urged caution.

October 2025

Stock Plunges > 70%

Continued ETH buying (300 k ETH) brought the total to > 3.5 million. Market value collapsed.

November 2025

81% Stock Decline Confirmed

With ETH near $2,250 and holdings 3.63 million ETH, BitMine’s market cap hit yearly lows; concerns over sustainability intensified.

BitMine’s rapid asset accumulation created unprecedented exposure: a single-asset treasury tied almost entirely to Ethereum’s price. When the market corrected, that exposure translated directly into stock losses.

BitMine’s (BMNR) Under-performance Vs. Ethereum — What the Data Shows

Holding nearly 3% of Ethereum’s total supply gives BitMine immense exposure, but also immense risk. The company’s stock has fallen far more than Ethereum itself because investors are accounting for execution risk, financial structure, and market psychology, not just crypto price movements.

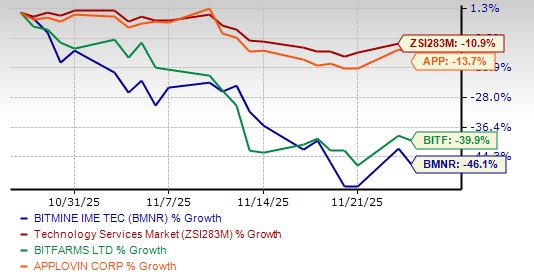

BNMR stock is down 81%. | Source: Zacks Investment Research

BitMine remains the largest publicly disclosed corporate treasury holder of ETH, positioning itself as a leading institutional player in the Ethereum ecosystem. This holding makes the company one of the most concentrated corporate investors in a single digital asset globally.

Still — BMNR Stock Has Fallen More Than ETH

Even while Ethereum’s price has fluctuated throughout the year, BitMine’s stock (BMNR) has significantly under-performed ETH. Over comparable periods, analysts have noted that a modest decline in ETH’s market price has corresponded to a much larger decline in BMNR’s share price.

As of late November 2025, despite its massive ETH holdings, BMNR shares are down around 81% from their peak earlier in the year.

This sharp disconnect suggests that investors no longer view BitMine purely as a proxy for Ethereum’s price. Instead, the market is pricing in additional risks, including the timing of ETH purchases, the high concentration of assets, dilution from share issuances, and structural weaknesses within the company’s “digital asset treasury” model.

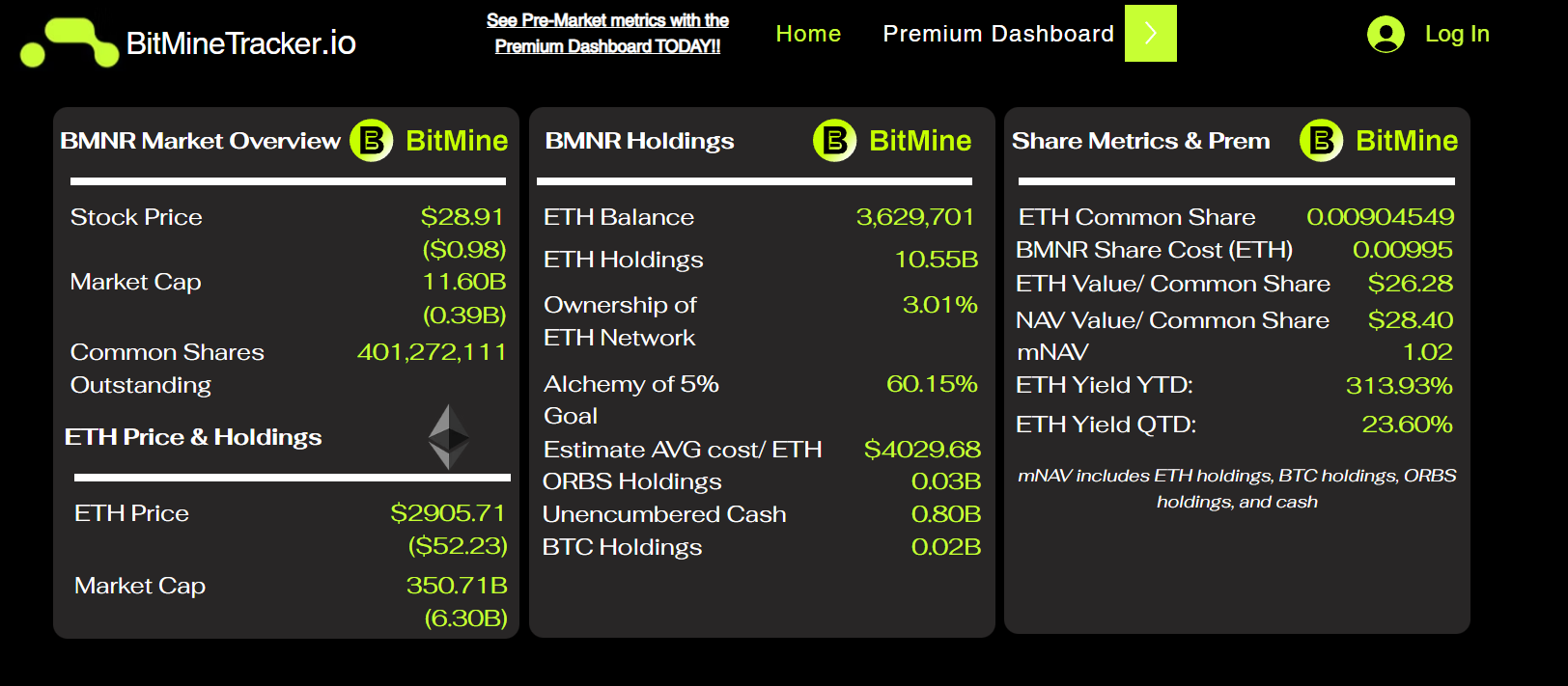

BitMine Tracker. | Source: BitMine

Why the Under-performance Happens — Key Factors

Purchase timing and price basis: Much of BitMine’s ETH accumulation occurred when Ethereum traded at higher levels. As ETH declined, the company’s unrealized losses expanded, and those losses translated almost directly into lower equity value for BMNR shareholders.

Market sentiment and risk premium: The valuation of crypto-treasury firms like BitMine depends not only on the underlying assets but also on investor confidence and liquidity conditions across the broader crypto market. When sentiment weakens, stocks with leveraged exposure to digital assets tend to suffer outsized declines, even beyond the underlying crypto’s performance.

Concentration in one asset (ETH) vs. diversified holdings: BitMine’s strategy is heavily centered on Ethereum, unlike other firms that combine Bitcoin holdings with operational businesses or diversified digital assets. This single-asset concentration magnifies volatility: when ETH prices fall, BitMine’s equity value declines even faster due to the absence of other revenue streams or hedges.

What Caused the Downturn of BitMine’s BMNR?

The collapse in BitMine’s share price reflects more than just a drop in Ethereum’s price. According to digital treasury analysts, stems from structural flaws in the business model: heavy single-asset concentration, equity dilution, low yield on holdings, and aggressive financing – all under a now-shrinking NAV premium.

Even if ETH recovers, BitMine could face an uphill battle: restoring investor confidence requires proving that its model can survive periods of crypto downturn – either through yield generation (staking / validator business), diversification, or more transparent, sustainable financing.

Markus Thielen of 10x Research warned that DAT firms like BitMine face a “Hotel California” scenario: once the NAV premium collapses, shareholders could be “trapped,” with no easy exit without taking heavy losses.

TREASURY COMPANIES – One Liners

MicroStrategy plunged on NAV premium compression and index-delisting concerns, despite management defending long-term balance sheet durability.

Metaplanet raised capital via a preferred issuance to accelerate Bitcoin purchases, tying its…

The decline followed a significant fall in Ethereum’s market price from earlier peaks, while BitMine’s average purchase cost remained high. This mismatch between acquisition cost and current market value has become a major drag on the company’s balance sheet.

Although BitMine continues to hold one of the world’s largest corporate ETH treasuries, the market now values those holdings far below the price paid, eroding shareholder equity and raising questions about capital allocation discipline.

Structural Weaknesses in the “Digital Asset Treasury” (DAT) Model

Analysts at 10x Research, led by Markus Thielen, have pointed to deep structural issues within BitMine’s digital-asset treasury approach. These include high embedded fees, relatively low staking yields, and the collapse of the premium investors once paid above NAV.

ETH staking yields, a core component of BitMine’s expected revenue, have remained modest at around 3% annually. When adjusted for operational and custody costs, the effective return is even lower. This weakens the rationale for holding ETH as a yield-generating treasury asset.

As the market’s NAV premium narrowed, BitMine’s model of “issuing equity to buy crypto” became far less viable. Once the premium disappeared, the company was left exposed to pure downside in the underlying asset.

ETH prices and BNMR purchases. | Source: BitMine Tracker

Frequent Share Issuances Leading to Dilution and Investor Fatigue

Short-seller analyses in October 2025 criticized BitMine’s ongoing share issuances to fund additional ETH purchases. The repeated capital raises diluted existing shareholders and signaled that the strategy relied heavily on favorable market sentiment.

As investor enthusiasm faded and the NAV premium evaporated, each new issuance further eroded shareholder value. Analysts described this as a cycle of dilution and diminishing confidence, a pattern that deepened the sell-off in BitMine’s stock during the latter half of the year.

ETH Price Decline and Broader Market Weakness

BitMine’s stock performance has sharply under-performed Ethereum itself. While ETH declined through the year, BitMine’s shares fell even faster, indicating that investors were discounting not only the lower asset value but also perceived structural flaws in the company’s strategy.

This reaction shows that markets view BitMine’s equity not merely as a proxy for Ethereum’s price, but as a leveraged bet with additional execution and financing risks attached.

Matthew Sigel’s View: The Fragile Foundation of Digital Asset Treasury Firms

According to Sigel, the success of DATs is tightly linked to bullish crypto market cycles and investor sentiment, not steady business fundamentals. He warned that a significant market correction, especially in Bitcoin or Ethereum, could “completely halt the formation of new DATs” and leave existing ones struggling to maintain valuations or liquidity.

No public BTC treasury company has traded below its Bitcoin NAV for a sustained period.

But at least one is now approaching parity.

As some of these companies raise capital through large at-the-market (ATM) programs to buy BTC, a risk is emerging: If the stock trades at or near…

— matthew sigel, recovering CFA (@matthew_sigel) June 16, 2025

Sigel has highlighted several structural weaknesses in the DAT model:

Dependence on market momentum: He noted that crypto asset prices are still “driven 90% by flows and only 10% by fundamentals.” That means most DAT valuations rise or fall with capital inflows rather than with productive cash-flow performance, exposing them to sharp reversals when liquidity dries up.

Dilution trap when trading near NAV: Sigel described the scenario where DATs issue new shares while trading close to their NAV as a “dilution trap.” In this phase, new equity issuances may destroy shareholder value instead of creating it, as the marginal cost of acquiring additional crypto outweighs any perceived premium in the market.

Vulnerability to low volatility: He added that if crypto volatility decreases, DATs lose one of their few operational advantages, the ability to expand holdings during market swings. In low-volatility or flat markets, DATs relying solely on treasury appreciation may find it increasingly difficult to grow or justify their valuations.

Need for sustainable revenue: Sigel emphasized that DATs must develop real, recurring revenue streams, such as staking, infrastructure services, or technology licensing, to survive in future market conditions. Without such diversification, these firms remain overly exposed to sentiment-driven cycles.

In Sigel’s assessment, the digital-asset-treasury model is powerful during bull markets but structurally fragile in bear or sideways phases. His perspective aligns with broader analyst warnings that companies like BitMine, which rely on crypto accumulation rather than operational performance, face serious risks if digital asset prices remain subdued or volatile.

Why Owning 3% of ETH Supply Doesn’t Guarantee Stock Success

As mentioned above, BitMine’s large Ethereum treasury, roughly 3% of the total ETH supply, worth about $3.6 billion, doesn’t automatically translate into higher stock value. That’s because a company’s market performance depends on how efficiently it manages and monetizes those assets, not just how much crypto it holds.

Crypto holdings can boost balance sheets, but they also expose firms to volatility, liquidity limits, and poor capital allocation risks. If those assets aren’t generating sustainable revenue, through staking, lending, or operations, investors may still view the company as overvalued or vulnerable to market swings. In short, owning crypto doesn’t equal profitability, especially when sentiment or execution falters.

BitMine’s Outlook for 2026

Analysts note that BitMine’s path forward hinges on Ethereum’s recovery and the company’s ability to diversify revenue.

Potential positive catalysts include:

ETH surpassing $3,000, narrowing unrealized losses;

Strategic partnerships in data-center infrastructure or energy-efficient computing.

However, without diversification, BMNR remains a high-beta proxy for Ethereum itself. In contrast, MSTR demonstrates that blending digital-asset treasuries with strong cash-flow operations provides greater resilience during market corrections.

Because it bought large amounts of ETH at high prices using share sales, leading to big unrealized losses, dilution, and weak investor confidence as sentiment toward crypto cooled.

How much Ethereum does BitMine hold?

BitMine holds about 3.63 million ETH, roughly 3% of Ethereum’s total supply, making it the biggest public corporate holder of ETH.

What are BitMine’s main weaknesses?

Low staking yields (3%), repeated equity dilution, and reliance on a shrinking NAV premium made its “buy-crypto-with-stock” model risky.

Can BitMine recover?

Only if ETH prices rebound and the firm diversifies revenue through staking, partnerships, or infrastructure projects; otherwise, BMNR stays a volatile ETH proxy.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.

Easy

Easy