JPMorgan’s new deposit token, JPMD, brings regulated bank money onto public blockchains. Learn how it differs from stablecoins. | Credit: CCN.com

Share

Key Takeaways

JPMorgan’s deposit token project (JPMD) is part of a broader push to digitize bank money.

The new JPMD pilot on Coinbase’s Base (a public chain) marks one of the first moves by a global bank to test regulated deposit tokens on a public blockchain.

Unlike USDC or USDT, deposit tokens are issued by banks, may be insured, can earn interest, and are fully integrated with banking systems.

Deposit tokens could become a core layer of institutional on-chain finance, merging the trust of banking with the efficiency of blockchain.

Banks are adapting to the digital age. One of the clearest examples is JPMorgan’s token projects, an effort to put bank money onto blockchains so payments can be faster, cheaper, and available 24/7.

This article explains the history, how these tokens work, why they matter, and what risks and limits to watch for.

JPMorgan’s Blockchain Push: How Banks Are Bringing Money On-Chain

JPMorgan first built a token system for clients years ago. Its private token, JPM Coin, was used within the bank’s own network to enable corporate customers to transfer money instantly between accounts on a permissioned (closed) ledger.

That system has processed large daily volumes, demonstrating that banks can utilize tokenized deposits for real-time settlement.

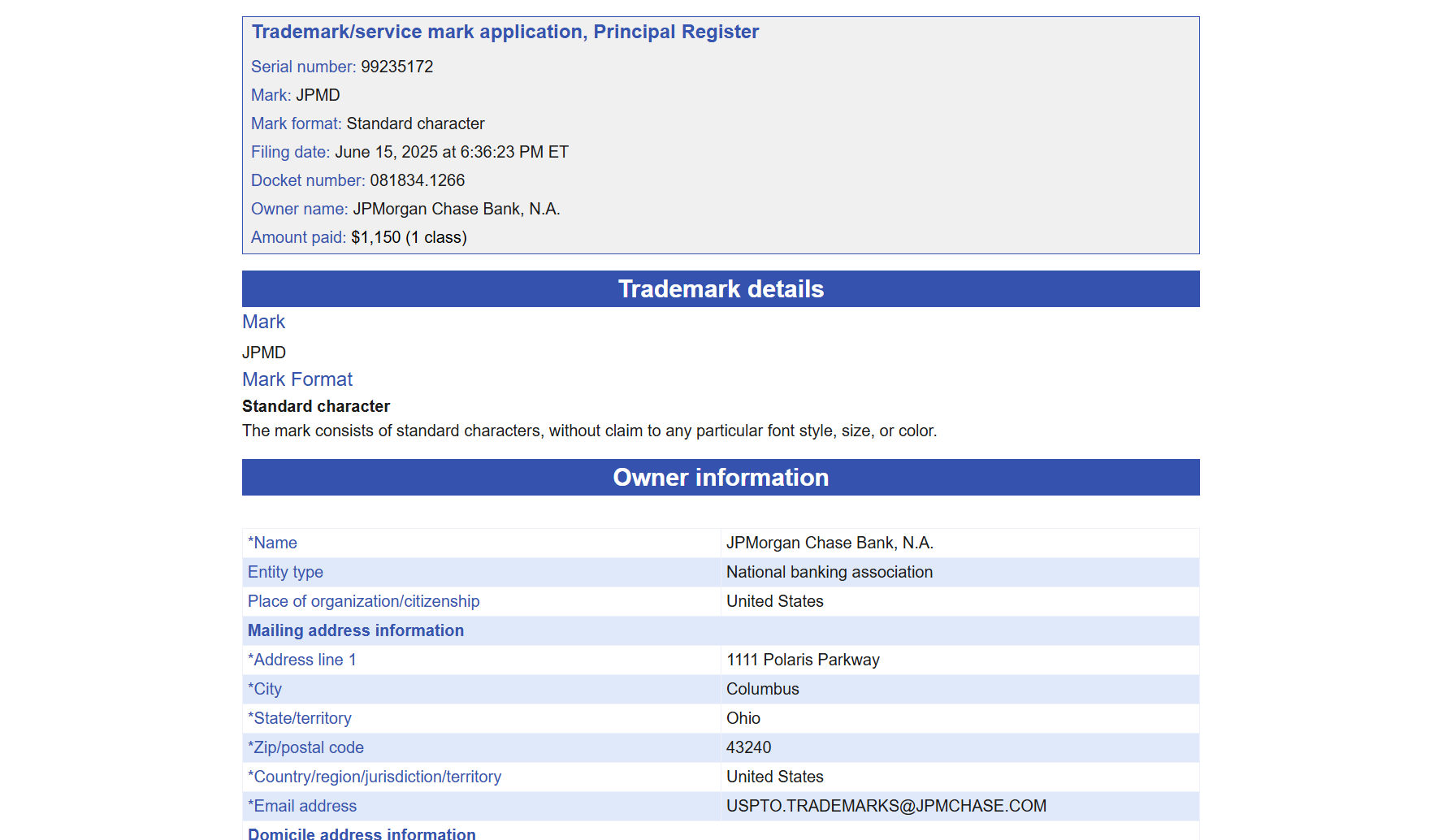

JPMorgan application for JPMD. | Credit: JPMorgan

This year, JPMorgan broadened the idea. It launched a pilot for a deposit token named JPM Coin, whose ticker is JPMD, and transferred a controlled amount onto Base, a public Layer 2 blockchain tied to Coinbase.

This is notable because it is one of the first instances where a central commercial bank has issued deposit-based tokens on a public blockchain, rather than keeping them exclusively on private networks.

What Are Deposit Tokens and How Does JPMD Work?

A deposit token is a digital token that represents a claim on a real bank deposit. Think of it as a digital IOU from the bank, but built and moved using blockchain technology.

Key points include:

Backing: Each token equals a deposit held at the bank (dollars in a JPMorgan account).

Permissioning: JPMD is currently permissioned, as it is only accessible to specific institutional clients. It’s not a public coin anyone can buy.

Settlement: Tokens move instantly on-chain, so payments can clear any time of day without waiting for bank hours.

Denominations and yield: JPMorgan’s deposit tokens can be interest-bearing and may be covered by deposit insurance in the future, thereby gaining features similar to those of banks.

These tokens aim to combine the legal and regulatory comfort of bank deposits with the speed and programmability of blockchains.

Why Banks and Institutions Are Exploring Deposit Tokens

There are real benefits for big companies and banks:

Speed and liquidity: On-chain transfers can settle in seconds, not days. This helps corporate treasuries and fund managers transfer money more efficiently.

24/7 operations: Blockchains operate continuously, so settlements do not need to wait for business hours to be open.

Programmability: Tokens can be linked to smart contracts to automate payments, collateral movements, and other financial logic.

Cleaner rails for tokenized assets: Tokenized securities and funds require an on-chain “cash” to settle against; bank-backed deposit tokens can serve this role, reducing reliance on private stablecoins. Industry research stresses tokenized cash as a crucial infrastructure for next-gen payments.

JPMorgan’s crypto initiatives. | Credit: LKZ_Hyper X profile

JPMD vs. Stablecoins: How Bank Deposit Tokens Stand Apart

Stablecoins like USDC or USDT are widely used on public blockchains and backed by reserves (cash, short-term Treasuries, etc.). However, they are issued by non-bank firms and are generally not covered by deposit insurance.

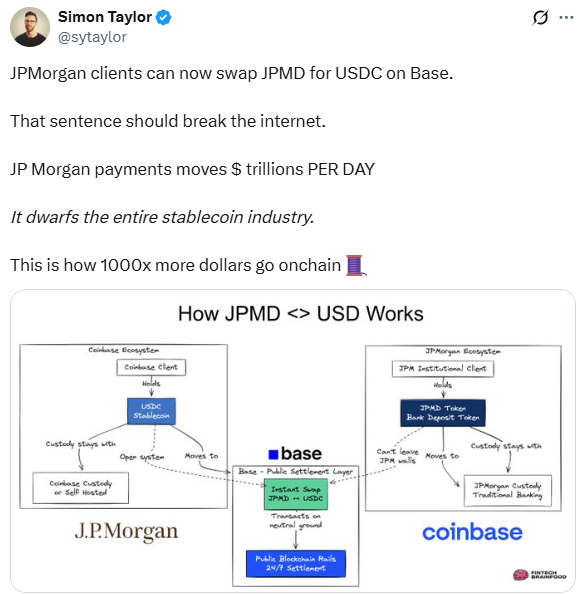

User reactions to the JPMD news. | Credit: styalor X profile

Deposit tokens from banks aim to offer similar on-chain usability while retaining bank features (deposit insurance, possibility of interest, stronger integration with bank accounting).

That makes them attractive to institutions that need regulatory clarity and balance-sheet treatment consistent with banking rules.

Comparing JPMD and Stablecoins

Features

JPMD (deposit token on Base)

Public stablecoins (USDC/USDT)

Who issues it

JPMorgan

Private companies (Circle, Tether)

Backing

Bank deposits

Cash, Treasuries or equivalents

Where it runs

Public chain (Base), permissioned use

Public blockchains (Ethereum, others)

Who can use it

Institutional clients (permissioned)

Anyone with crypto wallet

Potential interest / insurance

Possible (bank product)

Usually non-yielding; not deposit-insured

Use case

Instant institutional payments, settlement

Retail and institutional payments, DeFi

Regulatory clarity

Higher (bank product), evolving

Varies by jurisdiction; regulatory scrutiny high

Real-World Use Cases for Deposit Tokens

JPMorgan and others are targeting several use cases:

Corporate treasury flows: Multinational firms can instantly move cash between subsidiaries or trading partners.

Tokenized fund redemptions: Asset managers can settle fund redemptions on-chain without converting to off-chain cash.

Collateral management: Tokenized collateral and repo markets can settle faster with on-chain cash.

Aspect

Mainstream Stablecoins (e.g., USDC, USDT)

Bank Deposit Tokens (e.g., JPMD)

Issuer Type

Non-bank fintech firms

Regulated banks

Backing Assets

Cash, short-term Treasuries, other reserves

Actual bank deposits

Deposit Insurance

Not covered by FDIC or equivalent insurance

Covered by bank deposit insurance (where applicable)

Integration with Banking System

Limited; operates outside traditional banking infrastructure

Fully integrated with bank ledgers and accounting systems

Interest Possibility

Typically non–interest-bearing

May accrue interest like traditional deposits

Regulatory Clarity

Varies; under evolving frameworks

Clearer alignment with existing banking regulations

Target Users

Retail users, crypto-native institutions

Regulated financial institutions and corporates

Use Case Focus

On-chain payments, DeFi, and trading

Institutional settlements, tokenized assets, and treasury operations

Key Risks and Challenges for Tokenized Bank Money

Deposit tokens are promising, but they’re not a magic fix.

Key caveats include:

Permissioning limits reach: If only a few banks issue tokens and only their clients can use them, cross-bank interoperability remains a challenge. That limits global settlement benefits unless more banks adopt common standards.

Regulation and accounting: Legal, prudential, and accounting rules must be clear for banks to scale these products, as regulators are still catching up.

Fragmentation risk: The use of multiple tokenized “bank monies” across different chains and banks could lead to liquidity fragmentation unless bridges and standard rails emerge.

Public perception and access: Retail users generally cannot access JPMD today, as the product is primarily intended for institutional use. Broader retail use would require additional approvals and safeguards.

What’s Next for Deposit Tokens and On-Chain Banking

Deposit tokens are emerging as one of the most promising bridges between traditional banking and blockchain-based finance. Unlike stablecoins, which fintech firms typically issue, deposit tokens represent actual bank deposits recorded on-chain, offering regulated, secure, and programmable money for institutional use.

As major players like JPMorgan lead early experiments, attention is turning to how other banks, regulators, and public blockchain infrastructure will shape the next phase of adoption.

Adoption by other banks: If more global banks issue deposit tokens and agree on interoperability, the utility of these tokens will increase. Recent industry moves suggest interest from other big banks and collaborations (e.g., inter-bank links).

Regulatory action: U.S. and global regulatory clarity on tokenized deposits and stablecoins will determine the pace of expansion for these products.

Public chain experiments:JPMorgan’s pilot on Base demonstrates that banks can utilize public chains in a permissioned manner. How that balance evolves will be necessary.

JPMorgan’s token efforts, from the bank’s private JPM Coin systems to the recent JPMD pilot on Coinbase’s Base, show how traditional banking tools are being reimagined for the blockchain era.

For institutions, deposit tokens offer faster settlement, improved integration with tokenized assets, and bank-grade security. For the broader market, success depends on interoperability, regulatory clarity, and whether multiple banks and platforms can work together to avoid fragmentation.

If you’re new to this space, think of deposit tokens as bank money, but digital and programmable. They aren’t yet a replacement for cash in everyday life, but they could become the backbone for institutional on-chain finance if regulators and banks move carefully and in step.

JPMD is a deposit token, a digital representation of money held in a JPMorgan bank account. Each token is equivalent to one U.S. dollar deposited at the bank. It’s designed for institutional use and operates on a blockchain, allowing instant settlement between approved participants.

Who can use JPMD right now?

Currently, JPMD is accessible only to JPMorgan’s institutional clients and partners. Retail users and the general public cannot hold or transact JPMD at this stage.

Does JPMD pay interest or have deposit insurance?

In principle, as deposit tokens could earn interest and qualify for deposit insurance, as they represent bank deposits. However, these features depend on regulatory treatment and specific product design, which are still evolving.

Why does this matter for the future of finance?

Deposit tokens like JPMD could become the foundation of institutional on-chain finance, offering bank-grade safety and blockchain-level efficiency. If successful, they may replace many slow or manual interbank payment processes, bringing traditional finance closer to the speed and flexibility of cryptocurrency systems.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy