Home / Education / Crypto / Blockchain / Google Cloud Universal Ledger (GCUL) Explained: Will Google’s Blockchain Rival Ethereum or Redefine Global Finance?

Google Cloud Universal Ledger (GCUL) Explained: Will Google’s Blockchain Rival Ethereum or Redefine Global Finance?

Share

Key Takeaways

Google Cloud is developing GCUL (Google Cloud Universal Ledger), a new permissioned layer-1 blockchain aimed at global finance.

Unlike Stripe’s Tempo (merchants) or Circle’s Arc (USDC-focused), GCUL aims to serve all institutions.

Ethereum remains the credibly neutral public blockchain for settlement, hosting the majority of on-chain dollars (stablecoins) and tokenized assets today.

Most firms won’t build blockchains; Google is banking on demand for a neutral, turnkey ledger.

When Google decides to build its own blockchain, the entire financial world pays attention.

After years of experiments from banks, tech giants, and fintech startups, Google Cloud has unveiled the Universal Ledger (GCUL), a layer-1 network aimed at payments and tokenized assets.

Unlike the failed corporate chains of the past, GCUL arrives at a moment when stablecoins settle trillions annually and institutions are actively searching for faster, neutral rails.

What Is Google’s GCUL and What Problem Does It Aim to Solve?

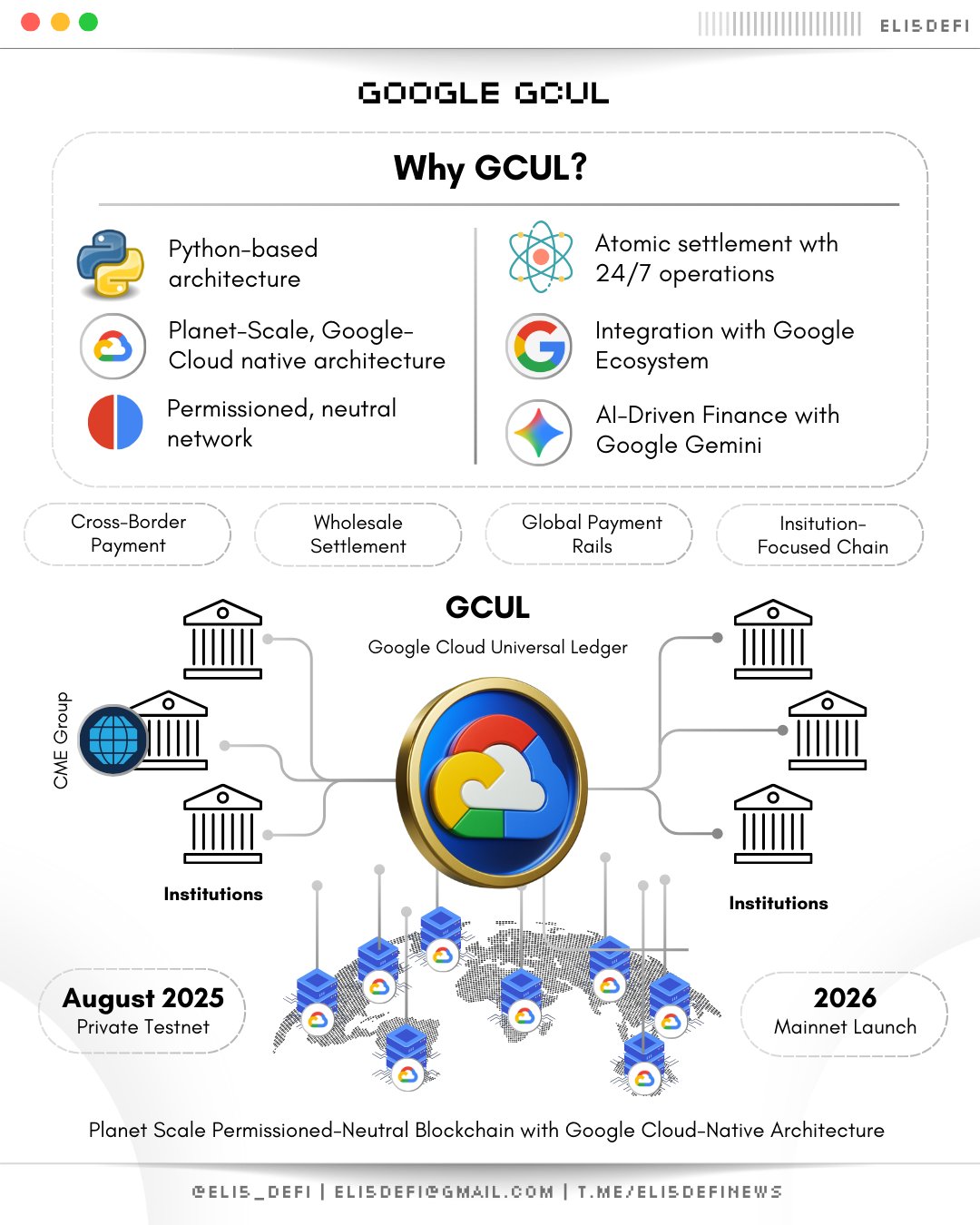

Google Cloud’s Universal Ledger (GCUL) is an upcoming layer-1 blockchain platform designed for payments and asset tokenization in the traditional finance world. In essence, GCUL serves as a distributed ledger service that financial institutions can plug into without having to build or maintain their own blockchain.

Top Crypto Tax Accounting Software

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

The goal is to provide a global, always-on network for money and asset transfers that is “simple, flexible, and safe”, according to Google.

The problem GCUL addresses is the outdated and fragmented nature of today’s payment infrastructure.

Traditional cross-border payments are slow, complex, and rely on siloed banking systems built decades ago.

Fragmented payment networks add significant friction and cost to global finance, an estimated $2.8 trillion (2.6% of global GDP) could be lost by 2030 due to payment system fragmentation. Banks also spend tens of billions annually maintaining aging payment systems. This fragmentation means transactions often take days to settle, requiring redundant ledgers and reconciliation between institutions.

By introducing a universal ledger, Google aims to upgrade the financial system’s “plumbing” rather than replace currencies. GCUL would allow multi-currency, multi-asset transactions on a single shared ledger that all participants trust.

Google Cloud is cooking up a new L1 blockchain for banks called Universal Ledger (GCUL). Runs Python smart contracts (not Vyper? 👀), in private testnet, aiming to be a neutral payments network. First pilot already live with CME Group https://t.co/p63XA7Lj0mpic.twitter.com/2a2YNPXZpB

For example, banks could represent customer deposit balances on GCUL and exchange value instantly with atomic (simultaneous) settlement. This promises to eliminate slow batch processing and costly intermediaries.

As Google describes it, GCUL brings the advantages of blockchain (transparency, immutability, 24/7 availability) while integrating compliance features like KYC and stable, predictable fees. In short, GCUL is pitched as an evolution of payments infrastructure, retaining the stability and legal clarity of traditional bank money, but delivered on a modern, programmable ledger.

The timing is notable too.

In recent years, stablecoins (crypto tokens pegged to fiat currency) exploded in use because they offer near-instant, low-cost transfers globally.

In 2024, stablecoins facilitated over $35 trillion in on-chain transactions, more than double Visa’s annual payment volume. However, public blockchain usage in finance brings challenges around regulation, compliance, and fragmentation across many blockchains.

Google appears to be positioning GCUL as a “best of both worlds” solution: blockchain-based efficiency with the trust safeguards of regulated banking. The platform is currently in private beta, with pilots (such as with the CME Group) already exploring tokenized asset settlement and payments on GCUL.

From Libra to Hyperledger: A Brief History of Corporate Blockchains

Google’s foray with GCUL follows a history of tech and finance giants experimenting with their own blockchains.

The Fate of Libra

A few years ago, Facebook (now Meta) launched an ambitious corporate blockchain project called Libra (later renamed Diem). Libra aimed to create a global stablecoin and payment network governed by a consortium of companies.

Regulators swiftly pushed back, fearing a private company could undermine monetary sovereignty. The project was ultimately abandoned, Meta sold off Diem’s assets in early 2022 for about $200 million.

Libra/Diem’s fate illustrated the challenge of a single corporation running a global currency network, especially without clear regulatory approval.

Hyperledger: The Leading Framework for Enterprise Blockchains?

Around the same time, enterprises were exploring permissioned blockchains for business use-cases. IBM, for instance, championed the Hyperledger project under the Linux Foundation.

Hyperledger Fabric, an open-source private ledger framework, became one of the most adopted enterprise blockchain platforms by the late 2010s. It allowed companies to build consortium networks with controlled access, suitable for supply chains, banking, and other use cases requiring privacy.

By 2025, Hyperledger’s ecosystem had grown substantially, with tens of thousands of nodes and even trillions of dollars in assets tracked on Fabric-based networks.

Approximately 78% of Fortune 100 companies have implemented a Hyperledger solution as part of their systems. This shows that enterprise blockchains can gain traction, but typically within industry silos or consortia, not as globally shared networks open to all.

Beyond Hyperledger: Banking and Fintech Experiments with Private Ledgers

Besides Hyperledger, many banks and fintech firms experimented with their own ledgers.

JPMorgan’s Quorum (a private Ethereum variant), R3’s Corda, and Ripple’s XRP Ledger (though semi-public) all sought to provide faster settlement networks for institutional use.

These permissioned layer-1s delivered technical innovation but often struggled to achieve network effects beyond their initial sponsors.

In other words, a bank might use a private ledger internally or with select partners, but that ledger wouldn’t necessarily be adopted by competitors or the broader market.

This context sets the stage for Google’s GCUL. Unlike Libra, which tried to create a new global currency, GCUL is focusing on the infrastructure layer (a ledger for existing currencies).

And unlike Hyperledger Fabric which each consortium deploys separately, GCUL aspires to be a single, shared network that many institutions collectively use (hosted by Google Cloud).

The big question is whether Google’s brand and neutrality claims can avoid Libra’s fate and overcome the hesitancy many had toward earlier corporate blockchains.

Stripe’s Tempo vs. Circle’s Arc: New Private Blockchains for Payments

Google isn’t the only major player building a payments-focused blockchain. Stripe and Circle, two heavyweights in digital payments and fintech, are developing their own proprietary ledgers, each with a different focus:

Stripe’s “Tempo”: Stripe, which processes over $1 trillion in payments annually, is quietly building a blockchain called Tempo. Developed with input from crypto VC firm Paradigm, Tempo is designed to integrate directly with Stripe’s vast merchant network. The project focuses on scalability and seamless settlement, likely using stablecoins, rather than supporting general-purpose DeFi or complex smart contracts. Expected to be a permissioned chain under Stripe’s control, Tempo could bring millions of businesses on-chain, with reports suggesting a launch timeline in 2025 or 2026.

Circle’s “Arc”: Circle, the issuer of USDC, is developing Arc, a layer-1 blockchain purpose-built for stablecoin finance. Unlike permissioned corporate chains, Arc is designed as a public or semi-public network with compliance and identity features to attract institutional adoption. USDC sits at the core, serving as the native currency for payments and transaction fees. Arc aims to enable fast payments, built-in FX between stablecoins, and cross-border remittances. Following its 2025 pilot programs, Circle plans to launch Arc with banks and fintechs acting as validators.

How does Google’s GCUL compare to these?

Google’s approach is more neutral and broad-based. As Google’s head of Web3 strategy Rich Widmann pointed out, both Stripe’s and Circle’s blockchains are tied to their creators’ ecosystems (Stripe’s merchant base and Circle’s USDC stablecoin).

That could deter competitors from using those networks, for example, a rival payments processor might be reluctant to settle on Stripe’s chain, and Tether (USDT’s issuer) is unlikely to use Circle’s Arc for its transactions.

Google is positioning GCUL as a neutral ground instead: a ledger not owned by a direct competitor in finance, where banks, fintechs, stablecoin issuers, and even exchanges could participate without feeling they are boosting a rival’s platform.

In terms of features, Stripe Tempo vs Circle Arc vs GCUL can be contrasted as follows:

Tempo is an EVM-compatible chain tied to Stripe’s $1.4T merchant payments ecosystem, focusing on wallets, onboarding, and off-ramps.

Arc is also an EVM L1, positioning USDC as native gas, offering sub-second finality, FX integration, and aiming to counter Tether’s dominance.

GCUL differs as a Google-built, planet-scale L1, currently in private testnet, targeting finance with Python smart contracts, native commercial bank money, and vast distribution via billions of Google users. Unlike rivals, GCUL stresses neutrality and institutional trust.

How does the GCUL stand out from other L1s? | Source: @eli5_defi on X

GCUL vs Ethereum: Neutral Settlement Layers and Network Scale

Google’s messaging around GCUL repeatedly uses the term “credibly neutral”, which draws an implicit comparison to Ethereum. Ethereum is currently the world’s largest public programmable blockchain and has become the de facto neutral settlement layer for many in crypto.

It’s credibly neutral in that no single company controls it, its consensus and governance are distributed among thousands of independent validators worldwide.

@Google is launching its own layer-1 blockchain, GCUL. 🤯 here’s what everyone is missing:

Ethereum’s neutrality and security have led to widespread adoption for settling digital dollars and assets. For instance, Ethereum hosts the majority of the stablecoin ecosystem by value; as of mid-2025, Ethereum’s network (including its layer-2 rollups) carried about 50% of all stablecoin value in circulation and handled a large share of the $35 trillion in stablecoin transactions noted earlier.

Ethereum is also the leader in tokenized real-world assets (RWA): roughly 72% of all tokenized real-world assets are issued on Ethereum (over $7.5 billion worth, including $5.3 billion in tokenized U.S. Treasury bonds).

This “network effect”, where stablecoin issuers, asset tokenization platforms, and DeFi applications all coalesce around Ethereum, makes it a global settlement hub that is hard to displace.

So, how might GCUL fit into a world where Ethereum already provides a neutral public blockchain for settlement?

One distinction is permissioning and control:

Ethereum is permissionless: anyone can use it, and it’s secured by a decentralized validator set.

GCUL, at least initially, is a permissioned ledger operated as a Google Cloud service. Google has signaled that GCUL could “become more open as regulations evolve”, but in the near term its validators and users will be vetted (e.g. KYC-verified institutional accounts on the network).

This could limit GCUL’s credibility as a neutral platform in the eyes of some crypto purists, after all, if Google and a few partners can theoretically censor or control transactions, it’s not neutral in the same way Ethereum is.

On the other hand, institutions might prefer a ledger with known governance and compliance controls, which GCUL offers, whereas transacting on Ethereum’s fully open network can raise questions about privacy, regulatory risk, and unpredictable fees.

Scale is another differentiator:

Google touts that GCUL will run on its highly scalable infrastructure and could support “billions of users” and hundreds of institutions from day one. This is leveraging Google’s unmatched reach, consider that Android alone has over 3 billion active users, and services like Google Pay, Gmail, and YouTube have massive user bases.

In theory, Google could integrate GCUL under the hood of consumer-facing products, rapidly onboarding users (even if they’re unaware a blockchain is being used).

In contrast, Ethereum’s active user base is orders of magnitude smaller: the network averages around 380,000–420,000 daily active addresses in 2025 (even counting power users and bots). Even including layer-2 networks, the number of distinct human users interacting with Ethereum regularly is likely in the low millions.

Google’s potential user reach is a compelling advantage for GCUL, it hints at a future where billions could be transacting on-chain via everyday apps, if GCUL succeeds.

However, adoption is about more than raw user counts.

Ethereum’s strength is the rich ecosystem of applications and assets already running on it. It’s credibly neutral in that USDC, USDT (Tether), DAI, and other stablecoins all coexist on Ethereum; competitors and partners alike leverage it because it’s an open standard.

If each company tried to bring those assets onto their own chain, the liquidity and interoperability could fragment. This is precisely why Google is stressing GCUL’s neutrality: “Tether won’t use Circle’s blockchain — and Adyen probably won’t use Stripe’s blockchain. But any financial institution can build with GCUL,” Widmann noted, implying that an impartial platform is needed to unite different players.

Ethereum today plays that unifying role to an extent (e.g., both USDC and USDT transact heavily on Ethereum, and multiple banks have piloted tokenization on Ethereum or its layer-2s).

GCUL aspires to be an alternative neutral zone, potentially appealing to institutions that are hesitant to use a completely public network like Ethereum for regulatory or performance reasons, but who also don’t want to depend on a competitor’s private chain.

Why Most Enterprises Won’t Build Their Own Blockchains

With so many custom blockchains emerging, one might ask: will every big company need to build its own chain?

The likely answer is no, as noted by Marc Baumann, Founder & CEO of 51 Group.

Most enterprises will not end up developing their own L1 blockchain from scratch, and there are several reasons why:

Network effects: Proprietary chains struggle to gain adoption; partners and rivals won’t join competitors’ networks.

High costs: Building and maintaining a secure, scalable blockchain is expensive and distracts from core business.

Regulatory burden: Running your own chain means handling KYC/AML, sanctions, and compliance in-house.

Interoperability issues: Too many closed chains create silos; industry is consolidating around shared platforms.

Preferred approach: Enterprises would prefer neutral ledgers (e.g., GCUL) or public blockchains (e.g., Ethereum) instead of isolated, proprietary chains.

But GCUL’s success will depend on whether organizations trust Google’s assurances of neutrality. If they do, many may prefer to build on GCUL or Ethereum or other major networks, rather than reinvent the wheel.

Despite its promise, GCUL faces several open issues:

Governance & control: Currently Google Cloud leads the project, but it’s unclear if governance will expand to banks and partners or remain centralized under Google. Trust hinges on whether it becomes a multi-stakeholder or stays Google-run.

Decentralization vs. permissioning: At launch, GCUL is expected to be a permissioned system, likely limited to banks and fintechs. The roadmap for broader decentralization is uncertain, raising questions about neutrality.

Interoperability: It’s not yet clear how GCUL will connect with Ethereum or other chains. Without strong interoperability, assets may remain siloed within GCUL, limiting liquidity and usefulness.

Tokens & assets: GCUL is expected to tokenize fiat (bank deposits or central bank reserves) rather than create a new native coin. Details on representation, regulation, and reserves management remain unresolved.

Competitive landscape:GCUL must compete with public chains like Ethereum and other private financial ledgers. Adoption will depend on whether banks trust Google as a neutral backbone for digital finance.

Each of these uncertainties will be watched closely. Google will likely release more technical whitepapers and governance frameworks in the coming months to address concerns.

As of now, GCUL represents a bold bet that a tech giant can provide the neutral, scalable backbone for digital finance that neither fragmented public chains nor isolated private ledgers have fully delivered.

It’s a high-stakes endeavor that could accelerate blockchain adoption in banking or, if misexecuted, underscore why truly neutral public blockchains like Ethereum are hard to replicate.

Conclusion

Google’s GCUL marks a bold step into blockchain by one of the world’s largest tech firms, promising a universal, programmable ledger for finance. With pilots underway and billions of potential users in Google’s orbit, GCUL could reshape payments and asset tokenization.

Yet, history shows corporate blockchains often struggle without credible neutrality, interoperability, and broad trust. Ethereum remains the benchmark settlement layer, with unmatched liquidity and decentralized governance.

GCUL may complement rather than replace public chains, serving institutions that value compliance and scale. Ultimately, its success will hinge on adoption beyond Google’s ecosystem and genuine neutrality in practice.

How is GCUL “credibly neutral” compared to other corporate chains?

Unlike Stripe’s Tempo or Circle’s Arc, GCUL isn’t tied to a single company’s core product. Google positions it as a neutral ledger for all institutions. This makes it easier for rivals to adopt without empowering a direct competitor.

Will GCUL replace banks’ internal ledgers?

No, banks will still maintain their own ledgers. GCUL is designed as a shared settlement layer between institutions. Think of it like SWIFT or ACH, but programmable and always on.

Can everyday users interact with GCUL directly?

Not at launch, GCUL is built for banks and enterprises. Consumers may use it indirectly through apps like Google Pay or partner banks. To most people, it will remain invisible infrastructure.

What risks could limit GCUL’s success?

Regulators may fear Google’s influence over finance. Banks might hesitate to trust a single tech giant for settlements. Lack of interoperability with public blockchains could also limit adoption.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy