It's difficult to be an aggressive buyer with a 32% GDP contraction on the horizon. But given that Goldman expects the downturn to be extraordinarily brief, investors don't want to miss out on the start of the recovery either. | Source: AP Photo/Richard Drew

Share

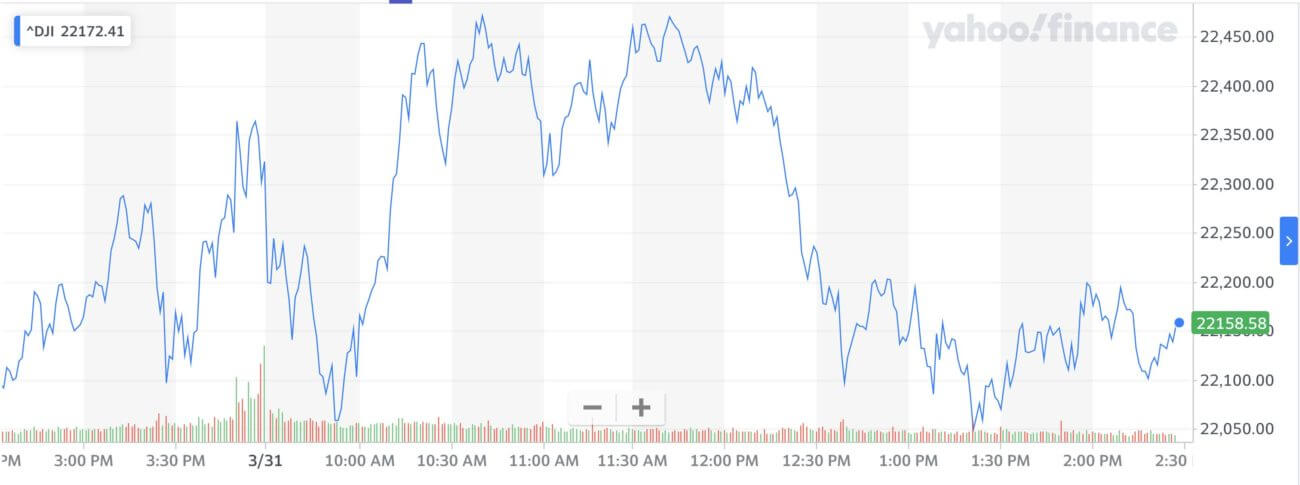

The Dow Jones suffered a reversal on Tuesday during the last trading day of the first quarter.

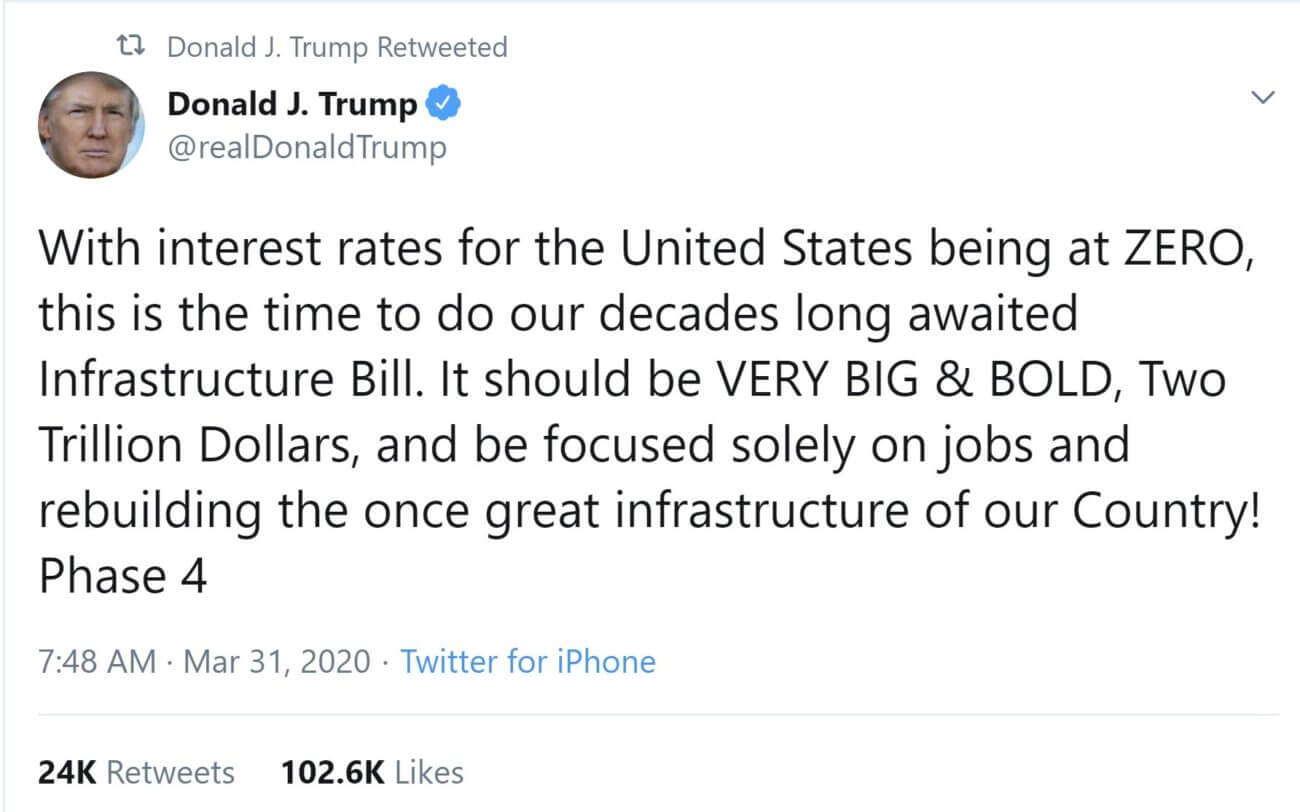

Goldman Sachs’ dire GDP update erased some of the optimism around Trump’s talk of a $2 trillion infrastructure package.

While overall U.S. coronavirus cases continue to surge, there are some bright spots in Europe and San Francisco.

The Dow Jones and broader stock market fought to extend their recovery on Tuesday, but an incredibly pessimistic GDP forecast from Goldman Sachs bludgeoned that bout of risk-on sentiment.

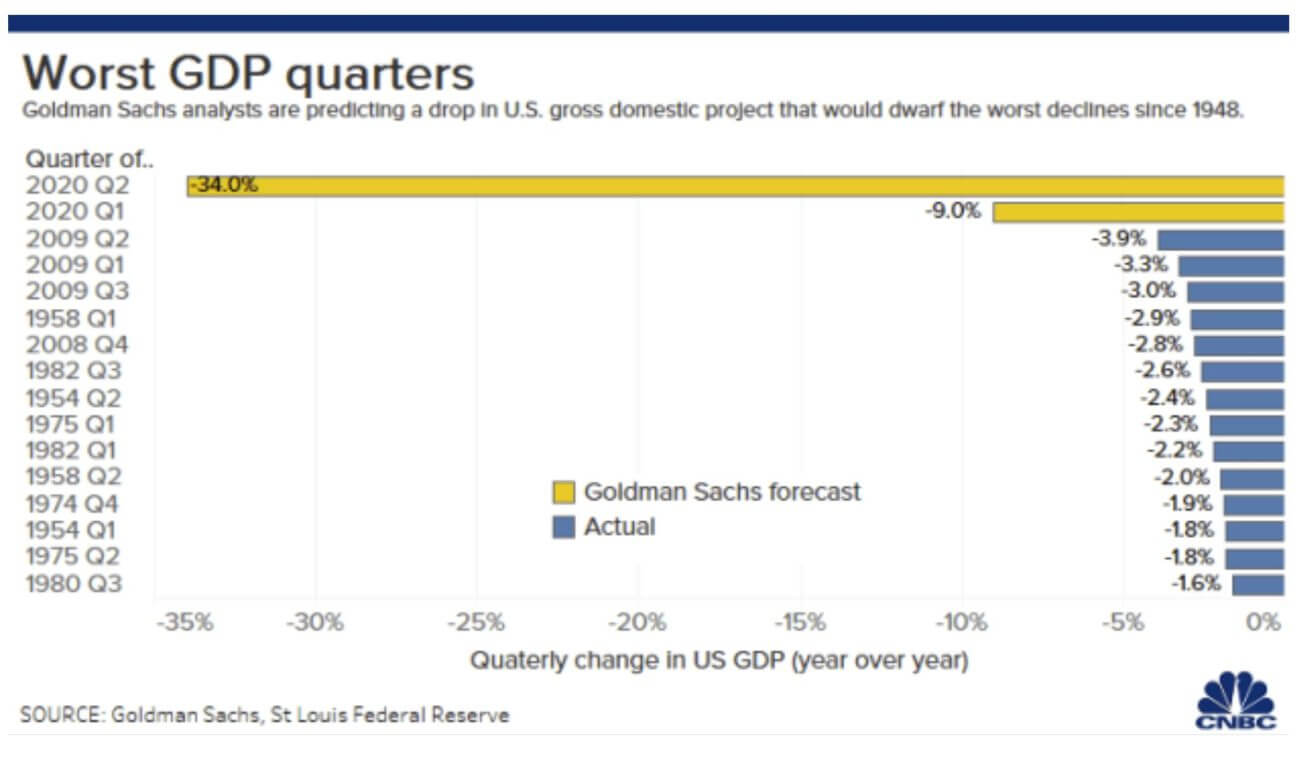

The investment bank predicts that U.S. GDP could collapse by a staggering 32% in the second quarter, and not even President Trump’s plans for a massive infrastructure spending plan could stop the Dow from careening to its worst first-quarter performance in history.

Dow Rally Fades After Trump Infrastructure Tweet Bumps Stocks

The Dow Jones slipped on Tuesday as Goldman Sachs’ dire GDP prediction knocked stock market sentiment. | Source: Yahoo Finance

All three of the stock market’s major indices swung lower in late afternoon trading:

The Dow fell 337.19 points or 1.51% to 21,990.29.

The S&P 500 dropped 1.55% to 2,585.93.

The Nasdaq slid 1.12% to 7,687.29.

In the commodity sector, the price of oil (+1.49%) hovered around $20 per barrel. The supply-demand curve continues to lurch in the wrong direction, but bulls are fighting to push crude above this vital psychological support.

A rally in the U.S. dollar hit the price of gold hard, and XAU/USD fell more than 2.8% to $1,597.

Consumer Confidence Defies Pressure from Coronavirus

On the economic data front, U.S. consumer confidence plunged in March, but the 120 reading (down from 136) was not actually as bad as economists feared (consensus forecast: 110).

Stock market bulls will be desperate to see the strong U.S. consumer hold up throughout the coronavirus pandemic. But the massive wave of unemployment puts households under severe pressure.

Unfortunately, the same cannot be said for the United States, where officials have confirmed more than 177,000 total cases. New York continues to bear the brunt of the impact, reporting more than 75,000 cases and nearly 1,000 deaths.

This could breed some confidence that it’s possible to get the outbreak under control. Unfortunately, the proactive measures in California were not taken in Louisiana, where a dramatic spike in cases leaves one of the United States’ most vulnerable regions uniquely exposed to the coronavirus.

Trump Teases $2 Trillion Infrastructure Plan

Donald Trump also sparked some buying from Dow bulls when he teased plans for a monster infrastructure spending plan that could top $2 trillion.

Unfortunately, this “VERY BIG & BOLD” spending plan may be difficult to push through Congress, given the enormous fiscal package legislators just approved.

Goldman Sachs’ Dire GDP Forecast Knocks Stock Market Rally

Unfortunately, the early Dow Jones rally faded as Goldman Sachs continued to one-up its own brutal U.S. economic forecasts.

Despite this, they still bank on a dramatic surge in demand to close the year, which could spark an extraordinary recovery:

Our estimates imply that a bit more than half of the near-term output decline is made up by year-end and that real GDP falls 6.2% in 2020 on an annual-average basis (vs. 3.7% in our previous forecast)[.]

Goldman Sachs predicts the U.S. economy will suffer its worst two quarters ever in 2020. | Source: CNBC

This kind of forecasting shows why the Dow is moving in such a hesitant manner. It’s difficult to be an aggressive buyer with a 32% contraction on the horizon. But given that Goldman expects the downturn to be extraordinarily brief, investors don’t want to miss out on the start of the recovery either.

Dow Stocks: Apple Steady, Caterpillar Crawls Higher

It was a cagey day in the Dow 30, where breakneck volatility has begun to cool.

Apple stock gave up its earlier gains to trade 0.69% lower, and moderate losses were the norm throughout the index.

The Dow’s top performer was Caterpillar stock, which rallied 3.8%. Helping to drive this bellwether growth stock was a surprisingly rosy Chinese manufacturing PMI figure. This is good news for CAT, which has a vital business interest in the Chinese construction industry.

Goldman Sachs (-3.5%) and JPMorgan Chase (-4.1%) were both under pressure as short term bond yields fell.

Financial speculator & author living in the hills in Los Angeles. J.D. but very much not a lawyer. Favorite trading books are anything written by Jack Schwager. | Follow Me On Twitter | Email Me