Is Aster’s $85.5B in Trading Volume Genuine or Just Wash Trading Illusion?

Share

Key Takeaways

Aster’s trading volume rose from $1.15B to $85.55B in 12 days after its TGE.

The Rh points system and multi-season airdrops encourage heavy trading activity.

The real question is whether traders stay after incentives end, with lower fees, MEV protection, and stock perpetuals as possible reasons.

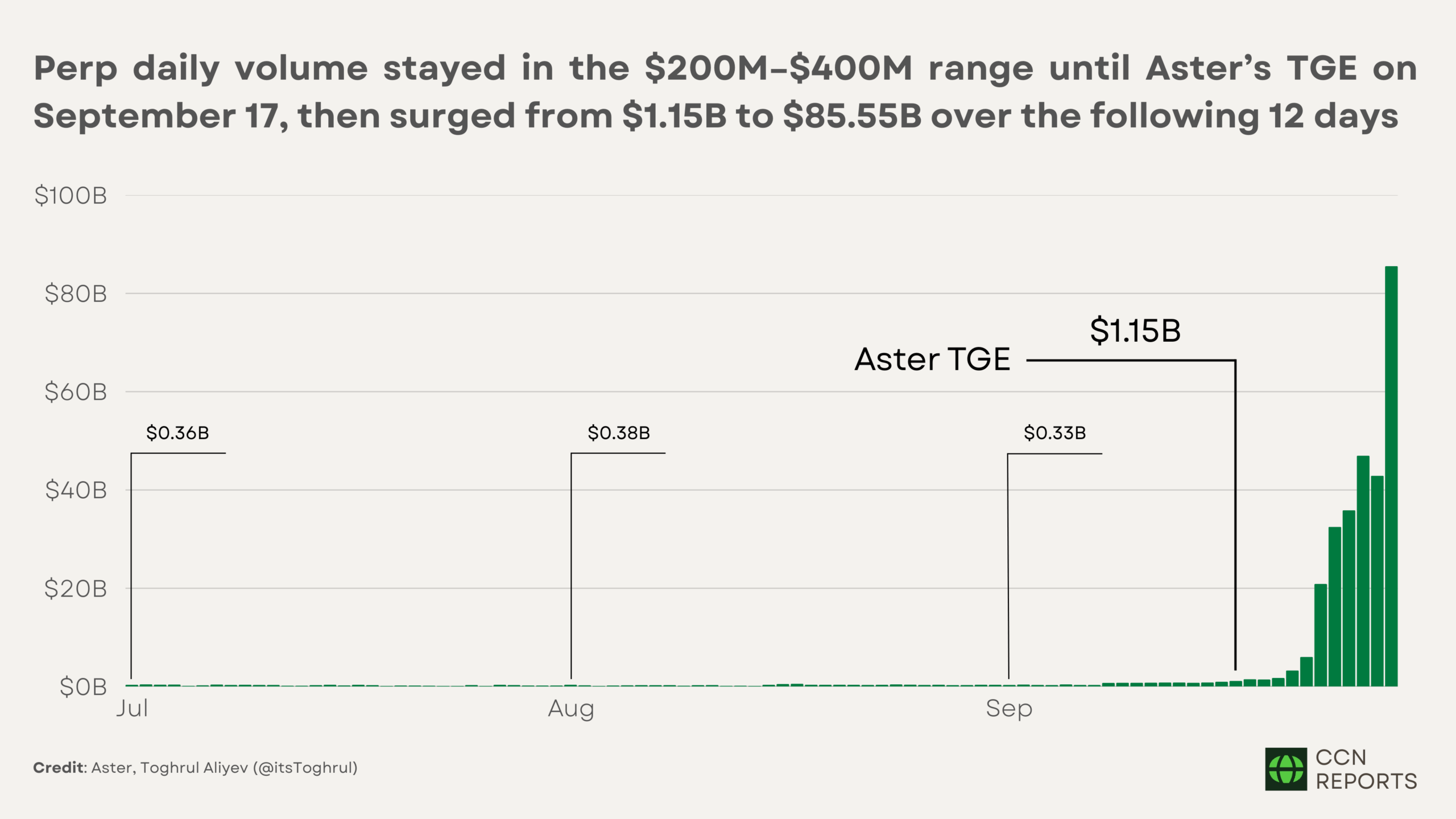

Since its token generation event (TGE) on September 17, 2025, Aster has recorded an unprecedented surge in perpetual futures trading volume, rising from $1.15 billion to $85.55 billion in just 12 days (Figure 1).

This leap propelled Aster ahead of Hyperliquid, the previous market leader, whose all-time peak was $27.19 billion, achieved on August 14, 2025.

Figure 1: Daily Trading Volume of Perpetual Futures on Aster | Credit: Aster, Toghrul Aliyev (@itsToghrul)

Of course, such rapid growth has fueled skepticism. Critics argue that part of the activity is not organic and that Aster inflates its volumes through wash trading.

$ASTER might be the most blatant market manipulation I’ve come across lately:

– 96% of tokens sit in just 6 wallets (likely one group behind them) – No functioning product, with barely $500k daily volume on its $BTC spot pair & half of it wash trading

In this issue of CCN Reports, I aim to examine the evidence directly. By applying data-driven heuristics to Aster’s trade records, I assess how much of its reported volume shows signs of wash trading and whether the concerns hold merit.

What is Aster?

Aster is a decentralized exchange focused on perpetual futures and spot trading. Its roots trace back to Astherus, a liquidity and yield platform that received backing from YZi Labs, the rebranded venture arm of Binance Labs, on November 28, 2024.

The investment provided both early capital for growth and the credibility of having direct backing from a fund with deep ties to Binance.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

A week later, on December 5, 2024, Astherus merged with APX Finance, a platform for decentralized perpetual trading. The merger opened the door to a rebrand, and on March 31, 2025, the exchange adopted the Aster name.

With the rebrand complete, the exchange slowly gained momentum through its user-friendly features.

Among them was multichain support, as Aster operates across BNB Chain, Ethereum, Solana, and Arbitrum, aggregating liquidity to remove the need for manual bridging or chain switching (Figure 2).

Figure 2: Chains Available on Aster | Credit: Aster

On top of this infrastructure, the platform provides two trading environments:

Simple Mode, which offers MEV-protected one-click execution with leverage up to 1001x, and

Pro Mode, which includes order book trading, hidden orders, and advanced analytics for professional use.

In addition to crypto markets, Aster lists stock perpetuals that trade 24/7 on assets such as AAPL, TSLA, MSFT, NVDA, and AMZN. It further supports yield-bearing collateral through asBNB and USDF, grid trading automation, hedge mode, and flexible margin systems that accommodate both single-asset and multi-asset positions.

Why Is Aster’s Trading Volume So High?

Aster’s rapid growth can be traced to a gamified incentive system introduced at launch. The exchange rolled out a multi-stage campaign, where participants earned “Rh points” for trading activity, position duration, and other behaviors.

Accumulated Rh points serve as the basis for receiving ASTER token rewards through periodic airdrops.

Stage 1 (Spectra) covered the initial trading days, and Stage 2 (Genesis) will run until early October 2025, with a significant portion of the token supply reserved as incentives. Stage 2 alone allocates 4% of the total supply, equal to 320 million tokens.

Each week, traders compete to accumulate Rh points, with multipliers applied to actions such as using leverage, taking liquidity instead of creating it, or holding positions longer.

At the end of a stage, points convert into token drops, turning trading activity into a contest. Referral bonuses and team-based boosts add further layers of gamification, pushing users to increase both their activity and consistency.

The effect has been striking. On-chain data show that Aster’s user base expanded from roughly 1 million to more than 3 million, while trading volume increased by more than 70-fold. Within weeks of launch, the exchange had overtaken its competitors to become the industry leader by volume.

And it worked. On-chain data show that Aster’s user base expanded from roughly 1 million to more than 3 million, while trading volume increased by more than 70-fold.

Within weeks of launch, the exchange had overtaken its competitors to become the industry leader by volume.

Concerns About Wash Trading on Aster

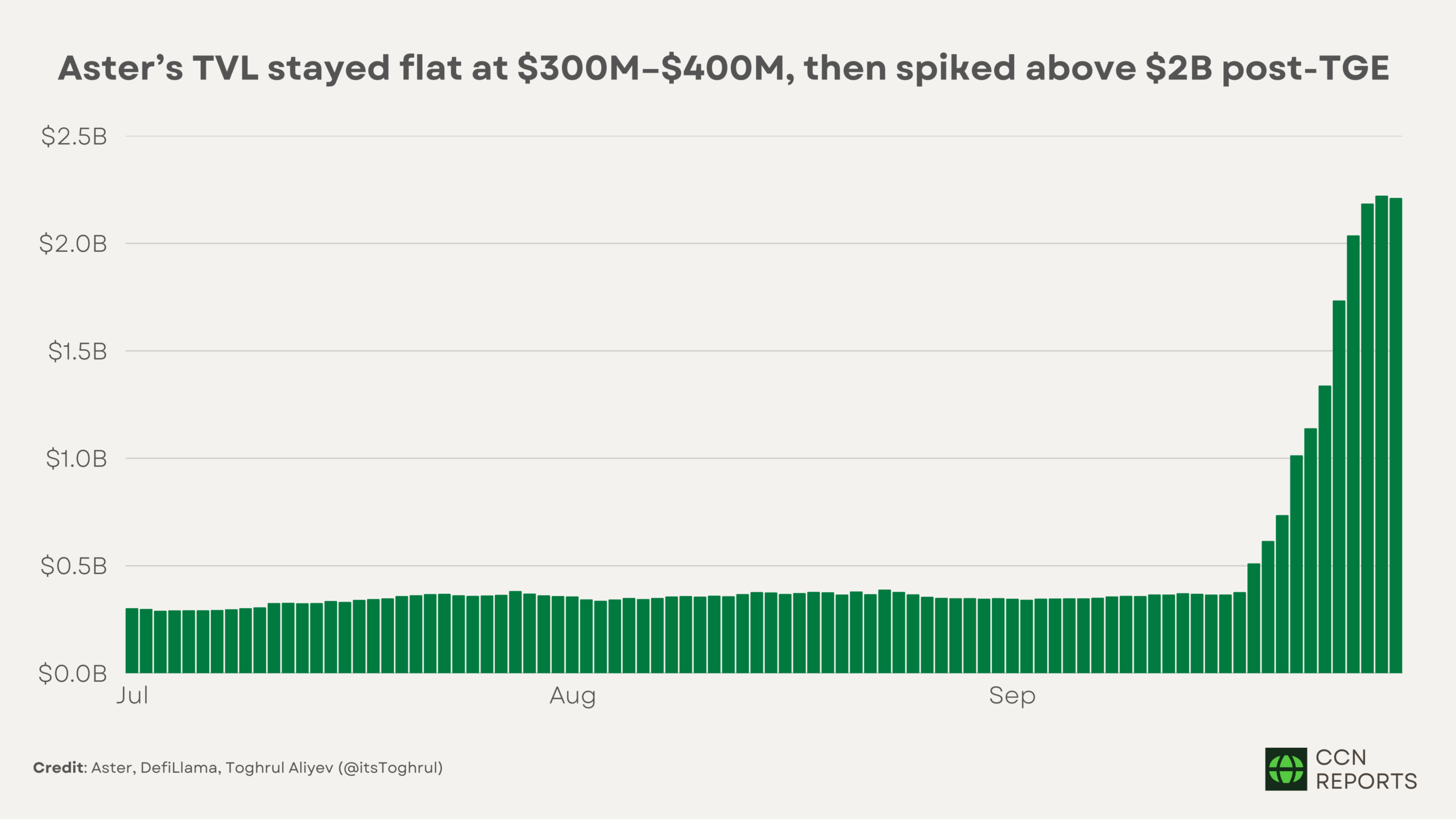

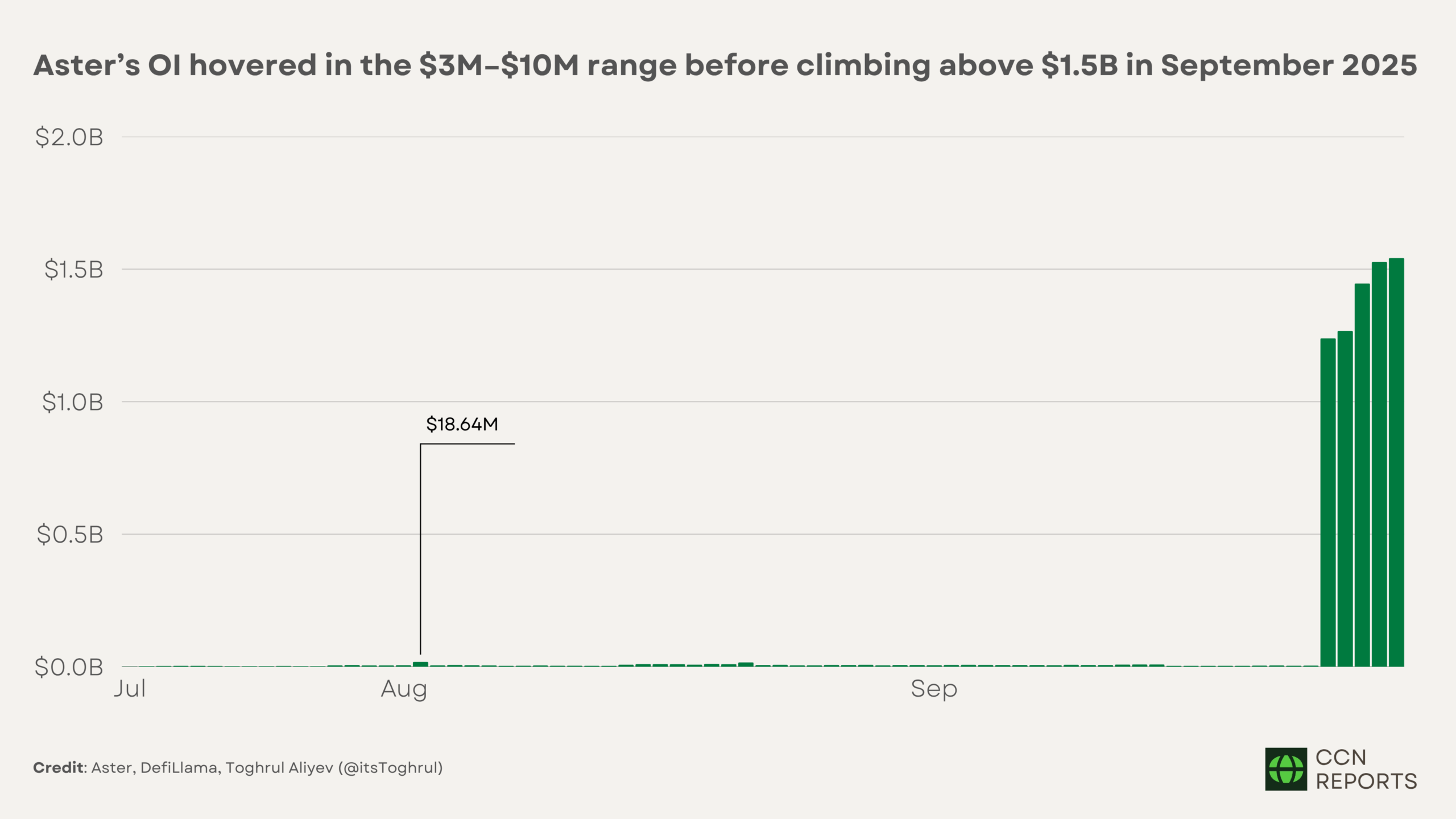

However, the surge in trading activity and user growth has not been matched by a proportional rise in open interest (OI) or Total Value Locked (TVL).

High trading volume without corresponding growth in OI or TVL signals that contracts are being opened and closed rapidly rather than reflecting sustained directional bets.

Such a pattern raises the possibility that a portion of the reported activity may be artificial trading designed to inflate the numbers.

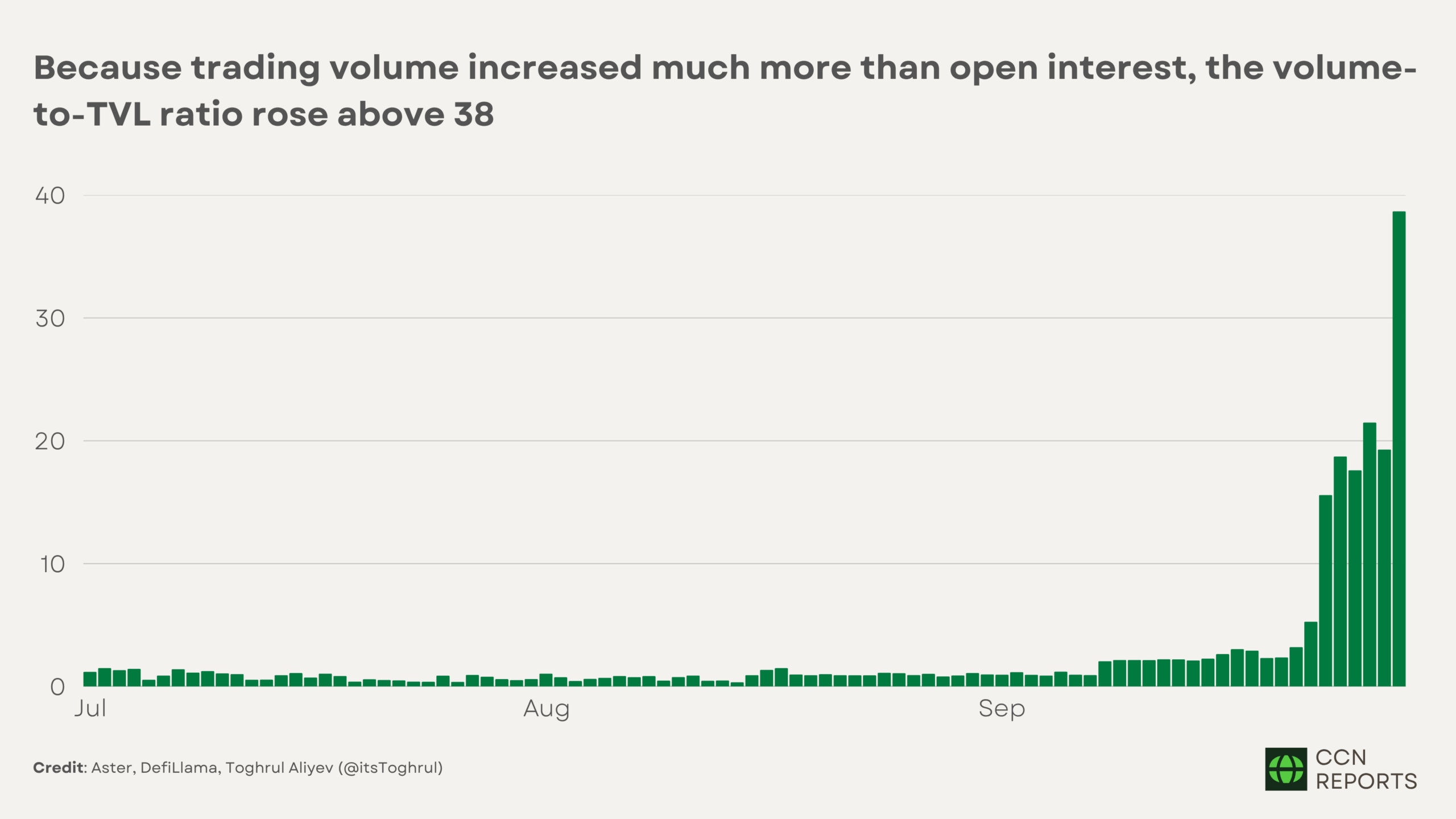

For much of 2025, Aster’s TVL ranged between $300 million and $400 million (Figure 3), with daily trading volume in a similar $200 million to $400 million band (Figure 1). This produced a roughly 1:1 ratio between the two metrics.

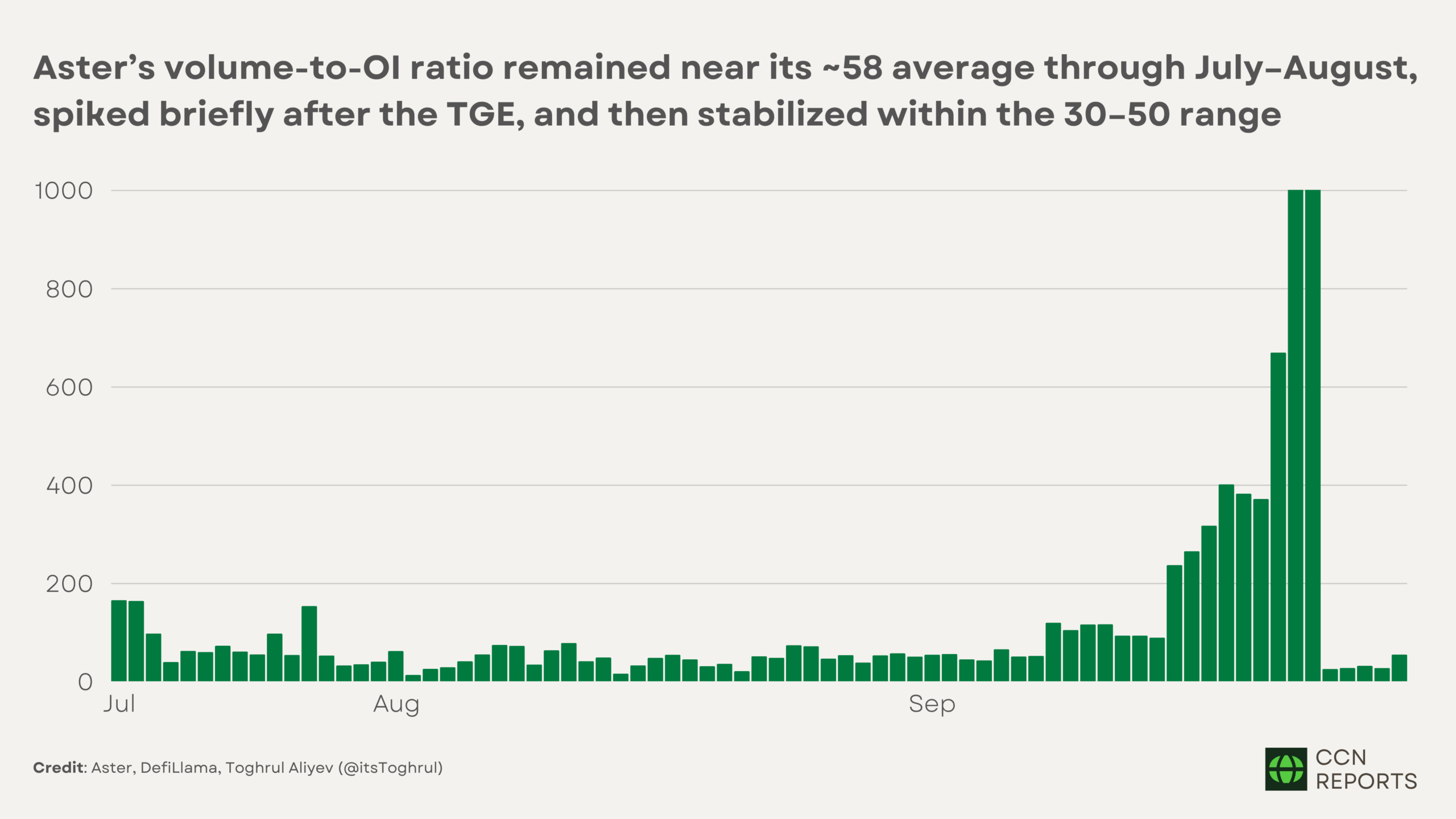

Open interest remained modest, typically ranging between $3 million and $10 million (Figure 4). After the token generation event, however, TVL climbed above $2 billion while reported volume jumped to more than $85 billion, pushing the volume-to-TVL ratio above 38:1 (Figure 5). Over the same period, OI spiked to more than $1.5 billion, creating a volume-to-OI ratio of 55.48 (Figure 6).

What stands out is that, despite the euphoria surrounding Aster after its token generation event, the volume-to-open interest (OI) ratio has not broken new ground.

Apart from brief surges, it has essentially returned to the same band seen in July and August, when the ratio averaged around 58.

On one hand, that stability suggests the current figures may represent a continuation of Aster’s established trading dynamics.

On the other hand, it could indicate that inflated activity has been present for much longer, with the post-launch spike reflecting an acceleration of existing practices.

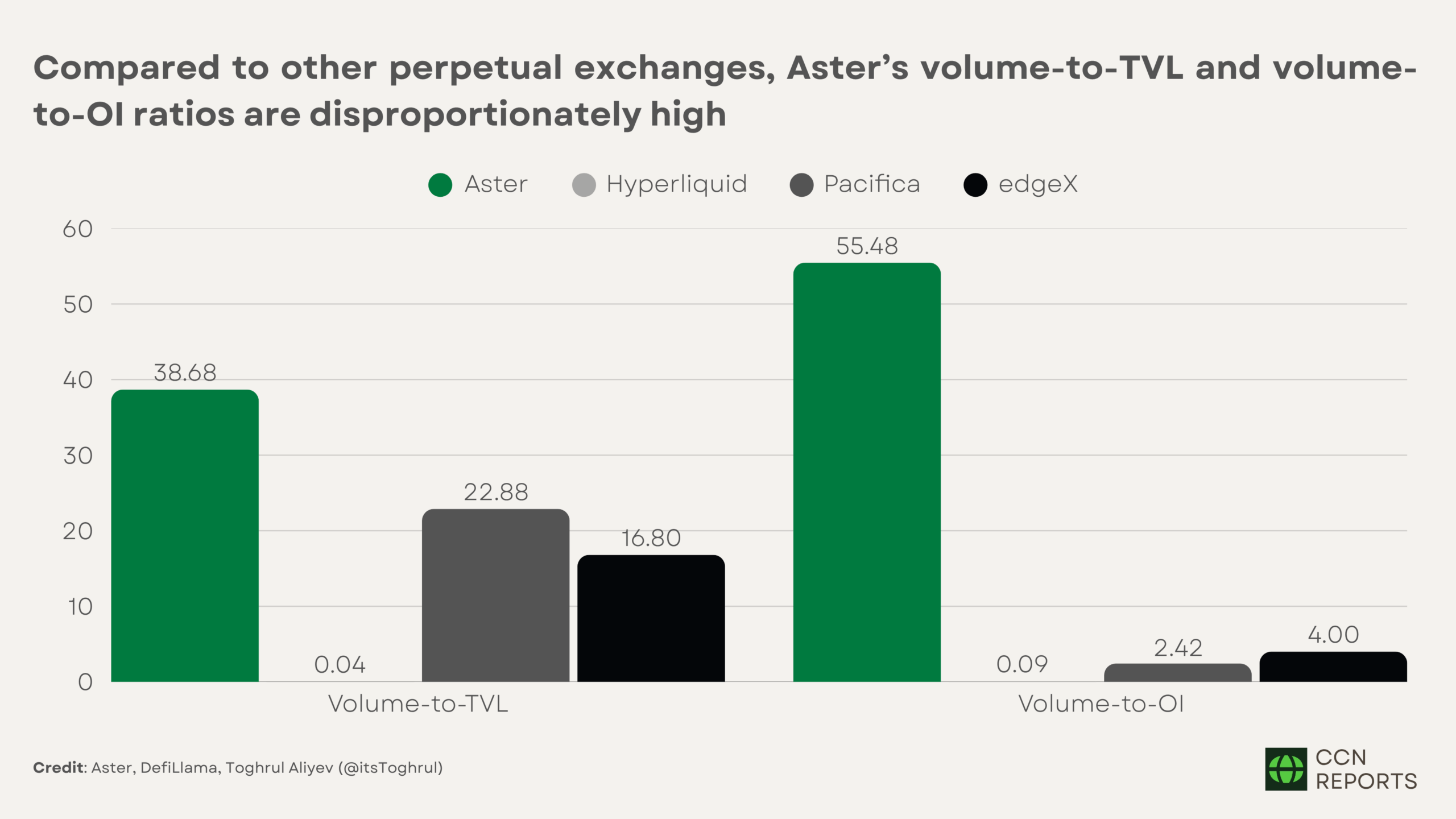

Still, when compared with other perpetual exchanges, Aster’s ratios stand out as an extreme outlier (Figure 7). As of September 28, Hyperliquid reported a trading volume of $529.79 million, TVL of $5.93 billion, and OI of $12.96 billion.

The resulting ratios were 0.09 for volume-to-TVL and 0.04 for volume-to-OI, far lower than Aster’s levels.

Another platform, Pacifica, a recently launched Solana-based perpetual exchange, reported $443.22 million in daily volume, $19.37 million in TVL, and $183.01 million in OI, producing ratios of 22.88 and 2.42. Again, lower.

EdgeX, with $4.13 billion in volume, $245.52 million in TVL, and $1.03 billion in OI, posted ratios of 16.8 and 4.

Figure 7: Volume-to-OI and Volume-to-TVL Across Perp Exchanges | Credit: Aster, DefiLlama, Toghrul Aliyev (@itsToghrul)

In each case, the ratios remain well below Aster’s. However, it is essential to note that the data used here primarily comes from DeFiLlama, which may not perfectly align with exchange-reported figures.

For example, Aster’s own website lists TVL at around $1 billion and OI at nearly $200 million, which is well below the DeFiLlama numbers.

Fortunately, the discrepancy does not weaken the concern. In fact, if the lower figures are more accurate, the resulting ratios would be even more extreme, reinforcing the underlying point.

The evidence so far points toward one possibility: wash trading. To evaluate that claim, the debate must begin with a clear definition of what it means.

What Is Wash Trading in Crypto?

Wash trading is the practice of repeatedly buying and selling the same asset in order to create the illusion of real market activity.

Instead of reflecting genuine supply and demand, the trades are arranged, often by the same party on both sides of the transaction, to artificially inflate trading volume, mislead other participants, or influence prices.

In traditional finance, wash trading is considered illegal because it manipulates market prices. In the crypto world, enforcement is more challenging, especially on decentralized exchanges, where transactions occur without centralized oversight. That makes crypto markets more vulnerable to inflated volumes, particularly on new platforms that could use trading incentives to attract users.

At its core, wash trading distorts three things traders rely on: volume (how much is traded), liquidity (how easy it is to enter or exit), and price discovery (where the “real” market price is).

There are six main types of wash trading in crypto:

Self-trading (direct washes): A trader (or bot) places both the buy and sell orders for the same asset, instantly matching against themselves.

Coordinated washes (account pairs/ring trading): Two or more accounts trade back and forth, often controlled by the same entity. It creates a loop of fake activity that looks organic at first glance.

Volume farming for incentives: Traders (or teams of traders) inflate volume to farm rewards such as airdrops, liquidity mining incentives, or leaderboard bonuses. Highly relevant for Aster’s Rh points system, since incentives tied to activity can encourage artificial turnover. However, Aster’s documentation explicitly prohibits such behavior.

Liquidity washes (fake depth): Bots place and cancel large orders rapidly, or execute small trades at high frequency, to make order books look active. This practice is more common on CEX-style order books but has also been adapted to certain DEXes with limit order functionality.

Cross-chain / arbitrage washes: Trades routed across multiple chains or pools that begin and end with the same asset, creating volume without risk. It can be masked as “arbitrage,” but it results in no real exposure.

Pool churning on DEXes: A trader cycles assets within a liquidity pool (for example, swapping ETH → USDC → ETH repeatedly). The pool records high volume, but the trader ends up with essentially the same holdings, minus fees (sometimes even refunded if they are also the liquidity provider).

Aster Trading Volume Analysis: Wash Trading or Real Growth?

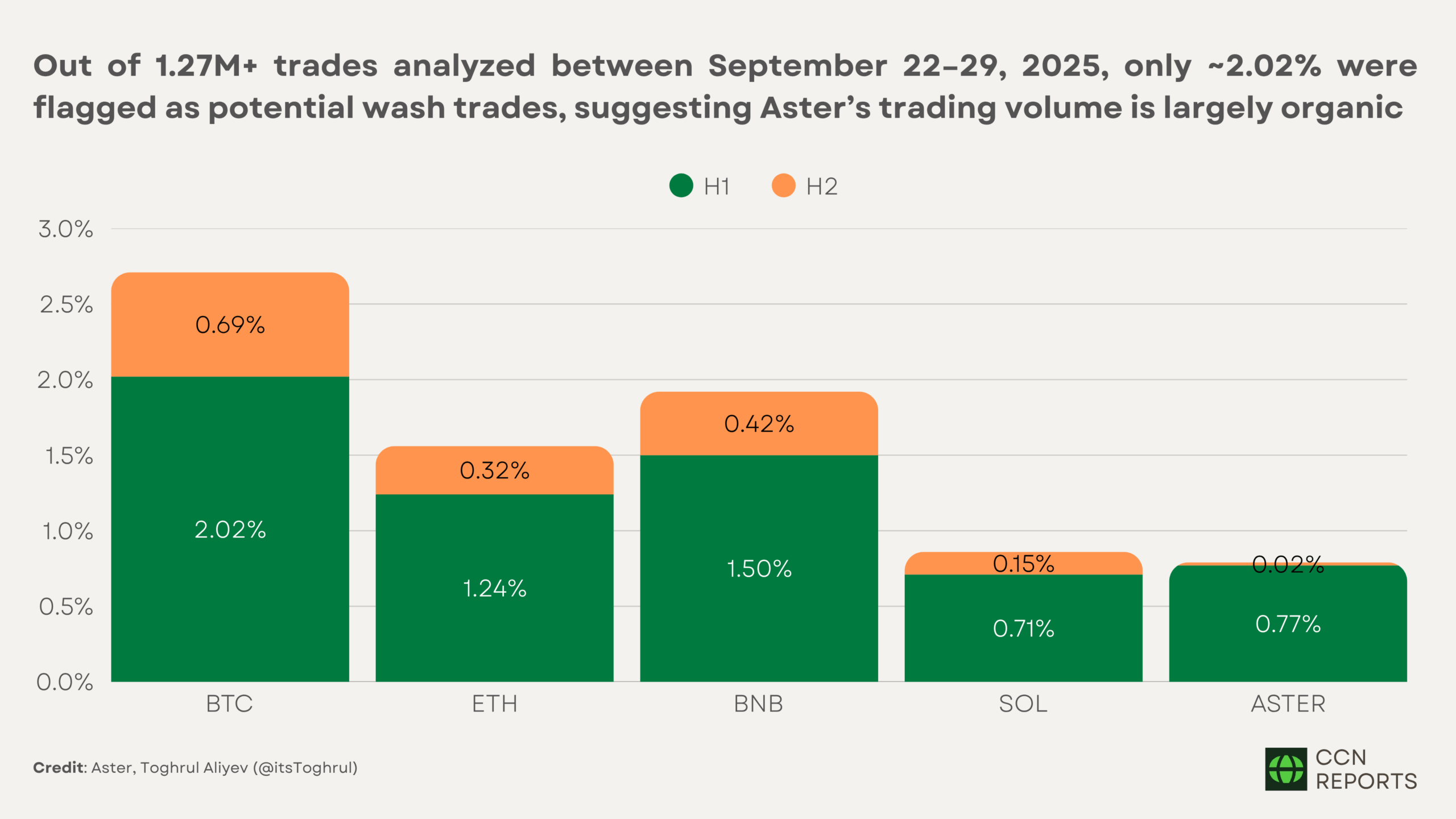

With the mechanics of wash trading defined, the next step is to test whether Aster’s reported activity reflects these patterns. To do so, I analyzed the platform’s trade history for the week of September 22–29, 2025.

The dataset comprised more than 1.27 million trades across eight markets, with the top five pairs —BTC, ETH, BNB, SOL, and ASTER —accounting for the vast majority of turnover.

The objective was not to prove intent, since the absence of account identifiers makes it impossible to confirm self-trading at the wallet level. Instead, the goal was to identify the share of trades that exhibit statistical patterns consistent with wash trading.

If wash trading were a major driver of Aster’s volume, the data should reveal repetitive, low-risk trading loops at scale.

Methodology

To test this, I applied two simple heuristics. Each is designed to capture a distinct style of wash trading, while maintaining transparent and reproducible analysis.

Heuristic 1: Consecutive Identical Size Flips

I flagged cases where a trade was immediately followed by another trade in the opposite direction (buy vs. sell) for the exact same quantity. For example, a sale of 1 ETH followed directly by a buy of 1 ETH.

Heuristic 2: Balanced One-Second Windows

I aggregated trades into one-second intervals and compared the total buy and sell notional. If the two sides matched within a 2% tolerance, I flagged all trades in that interval. The logic is that coordinated wash trades aim to cancel exposure, so a second where buys and sells line up almost perfectly suggests intentional balancing.

Limitations

I want to emphasize that these heuristics provide upper bounds rather than definitive proof. Some legitimate behaviors, such as high-frequency arbitrage or rapid hedging, can create similar patterns.

Conversely, wash trading that avoids precise size-matching or timing symmetry would not be detected here. The figures should therefore be interpreted as estimates of the maximum possible share of wash-like trades.

Findings

Applying the two heuristics to Aster’s trade records produces a consistent result:

Only a small fraction of activity shows signs of potential wash trading. Out of more than 1.27 million trades analyzed during the week of September 22–29, 2025, roughly 2.02% were flagged (Figure 8).

By notional value, the flagged trades accounted for about 1.7% of total reported volume.

The share of flagged trades across markets:

BTC/USDT: 2.7%

ETH/USDT: 1.6%

BNB/USDT: 1.9%

SOL/USDT: 0.9%

ASTER/USDT: 0.8%

Figure 8: Wash Trade Distribution on Aster | Credit: Aster, Toghrul Aliyev (@itsToghrul)

The analysis, therefore, indicates that, despite some anomalies, Aster’s reported volume is largely the result of organic trading dynamics.

Why Large-Scale Wash Trading Seems Unlikely on Aster

The first question to ask is simple: What would Aster gain from wash trading? Inflating volumes might briefly create the impression of dominance, but the costs of being exposed would be catastrophic.

Unlike in 2017–2018, when fake volume on exchanges could go unnoticed, the industry is now saturated with analytics platforms, on-chain data monitors, and competing exchanges that are ready to highlight anomalies.

If Aster deliberately engaged in large-scale wash trading and the cover were to be blown, the reputational damage would not only undermine the token but also potentially lead to the exchange’s demise. From a risk–reward standpoint, the downside dwarfs the benefit.

At the same time, Aster already had what most projects crave: hype and visibility. The endorsement from Changpeng Zhao gave the project credibility far beyond what artificial order flow could provide.

Fortunately —or perhaps unfortunately —in crypto, narrative often matters more than fundamentals, and being associated with a figure of CZ’s stature is equivalent to a multimillion-dollar marketing campaign.

Mainstream brands pay celebrities extraordinary sums for a reason: the return on attention can be 5–10 times the cost. Aster effectively received that kind of exposure for free. Why jeopardize it by manufacturing trades that could be unmasked in a matter of weeks?

It also matters that Aster offers real features that users can and do use. Lower fees than competitors, MEV-resistant execution through hidden order types, and novel offerings like 24/7 stock perpetuals make the platform distinct.

Exchanges with no genuine utility are more likely to lean on artificial activity to appear successful.

Aster, by contrast, has product hooks that plausibly generate organic traffic. Even if not every user is there for the features, they provide a floor of legitimate demand that reduces the incentive to fake numbers.

But the strongest point lies in the incentive structure. Through its Rh points system, Aster essentially outsourced volume generation to its users.

Traders compete for airdrop eligibility by churning trades, holding positions, or using leverage, which are behaviors that naturally inflate turnover. From Aster’s perspective, the job is already done. Users are motivated to trade excessively without the exchange needing to simulate that activity itself.

One could argue that in such a system, wash trading becomes “user-driven.” That doesn’t make all activity ideally organic, but it does make exchange-driven manipulation redundant.

Aster reserves the right to disqualify trades that are deemed to be wash trades, displaying attributes of market manipulation, bulk-account registrations to farm additional bonuses, or any other attempts at fraud.

If the analysis presented earlier is accurate, roughly 2% of trades would fall into that category. That share is not negligible, but it suggests that the overwhelming majority of activity would remain valid under Aster’s own criteria.

There is, however, an unavoidable caveat. Without wallet-level identifiers, no analysis can prove intent. Some portion of Aster’s activity may indeed be artificial, and the heuristics used here can only flag suspicious patterns rather than confirm them.

It is possible that crypto exchanges still quietly engage in practices reminiscent of earlier cycles, and proving or disproving this will always be difficult.

Still, when the incentives are weighed, the logic points in one direction. Aster already had hype from a Binance-linked endorsement. It already had features capable of attracting traders.

It already had an airdrop framework that drove users to inflate their own volume. In that context, deliberately orchestrating large-scale wash trading would be unnecessary and irrational.

The longer-term question is what happens when airdrops end. Aster has designed its reward program as a sequence of seasons. With Season 2 underway and a third already planned, the incentive loop is set to run for some time.

That structure keeps traders engaged in the near term, and by the time it winds down, many may already have settled into routines that make Aster their default venue.

Many who argue that Aster’s rise is nothing more than manipulation are likely overstating the case. Some of that skepticism may come from the pain of missing one of the year’s strongest opportunities.

It is easier to label growth as “fake” than to accept that others captured returns while you stayed on the sidelines.

The debate also tends to focus on decentralization. Roughly 89% of the token supply sits in just six wallets, which, from a governance standpoint, is far from ideal (Figure 9).

Yet for most market participants, decentralization is not the deciding factor. What matters more is whether the product delivers returns or provides a smoother trading experience.

In practice, user-friendly features and the potential for ROI outweigh philosophical concerns about the concentration of supply.

From an analytical standpoint, I see little incentive for Aster itself to engage in wash trading. The platform already had the visibility, features, and incentive mechanics to generate activity organically.

Still, no conclusion can be absolute without wallet-level identifiers. If wash trading exists on Aster, the more plausible explanation is that it originates from users chasing airdrop eligibility rather than from the exchange engineering it directly.

Those trades would eventually be disqualified under Aster’s rules, but the fees would remain with the platform, supporting revenue, sustainability, and, by extension, token value.

So, Aster’s explosive volumes are best explained by the intersection of hype, incentives, and genuine product use.

Whether that momentum translates into lasting dominance will depend less on debates about decentralization or wash trading and more on the platform’s ability to retain users once the airdrop seasons are over.

Toghrul Aliyev is the Head of Research who began his journey in crypto in 2021. It all started with a Reddit post that went viral, leading to a writing position while he was still in medical school. As he learned more about crypto, he became deeply interested in it and decided to focus entirely on this field after completing his medical degree and becoming a doctor.

Toghrul specializes in thorough research, always aiming to find details others might miss. He also has a strong understanding of stocks, real-world asset tokenization, and related areas. He is skilled in Python and SQL, which he uses to improve his crypto analysis through data analytics and data science.

When he’s not working, Toghrul enjoys sports, hiking, reading philosophy, such as Seneca's works, and playing story-driven video games.