SWC’s leadership shows strong alignment at the top but faces governance risks from minimally invested directors and conflicts of interest.

The legacy web design arm is profitable but financially immaterial compared to the Bitcoin treasury, which drives nearly all valuation.

Dilution from warrants, equity issuance, and convertibles poses a structural risk that hinges on Bitcoin’s appreciation.

Power law modeling provides a framework for valuation, but limited data and wide variance make forecasts uncertain.

In the previous issue of CCN Reports, I published an analysis of The Smarter Web Company (SWC), documenting its rapid appreciation following the April 2025 IPO and the subsequent price retracement during the summer. That study focused on market structure, equity issuance, and sectoral dynamics.

The present issue extends the inquiry by undertaking a fundamental analysis of SWC as a corporate entity. It examines the company’s leadership and governance, evaluates fair value based on the economics of its core business, and analyzes its Bitcoin (BTC) strategy alongside scenario-based price projections.

SWC Leadership

Whichever way you look at a company, leadership sits at the center of its destiny. With the right people at the helm, even an ordinary business can deliver extraordinary results. When leadership falls short, even a robust model can collapse under the weight of poor decisions. For SWC, whose business model depends entirely on management’s capital allocation decisions and execution capability, evaluating the leadership team becomes central to the investment thesis.

Andrew Webley – Chief Executive Officer (CEO) & Founder

Figure1: Andrew Webley | Credit: The Smarter Web Company

At the center of The Smarter Web Company’s leadership is the founder and CEO, Andrew Webley, who built the company from a startup to profitability over 16 years before pivoting to Bitcoin treasury strategy in 2025.

While lacking formal asset management credentials, Webley brings 25 years of personal investing experience and deep fintech sector knowledge from his role as Head of Online at Hargreaves Lansdown, one of the UK’s largest investment platforms.

His 9.44% equity stake (27,418,732 shares) as of Sep 4, 2025 creates strong alignment with shareholders, though concentrates significant key-person risk. In Webley’s own words, the stake represents the bulk of his personal net worth.

Jesse Myers – Head of Bitcoin Strategy

Figure 2: Jesse Myers | Credit: The Smarter Web Company

Where Webley set the direction, Myers provides the framework to carry it out, bringing intellectual depth as Head of Bitcoin Strategy. Prior to his appointment, he served on the boards of several Bitcoin treasury companies but stepped down from those positions to commit fully to SWC and avoid conflicts of interest.

Beyond his frameworks and credentials, Myers showed his alignment with shareholders through a £970,000 personal investment in SWC during the fundraising announced on 16 June 2025.

Albert Soleiman – Chief Financial Officer (CFO)

Figure 3: Albert Soleiman | Credit: The Smarter Web Company

At CMC, he led the development of investment platforms and directed major business realignment initiatives while advancing through multiple senior roles, including Head of Tax, Head of Client Asset Management (with CASS compliance oversight), and Group Head of Corporate Development. His experience also bridges traditional regulated financial services with blockchain technology through his tenure as Global Tax Director at Bitfury Group, a Bitcoin mining and blockchain solutions company.

Soleiman is the second team member after Jesse Myers with direct Bitcoin company experience and the only one with FTSE credentials. His appointment allows SWC to pursue listing upgrades from Aquis to the London Stock Exchange Main Market or FTSE index inclusion, which would provide access to significantly larger institutional capital pools. He also brings the operational expertise needed to execute complex M&A transactions, implement institutional-grade financial controls for the company’s assets, and satisfy the regulatory requirements that larger investors demand.

Mario Visconti – Head Strategic Projects (Former CFO)

Figure 4: Mario Visconti | Credit: The Smarter Web Company

Another key figure is Mario Visconti, who transitioned from CFO to Head of Strategic Projects in September 2025.

Visconti brings over 25 years of accountancy experience, including running his own advisory practice and managing finances in the construction sector. He managed SWC’s IPO process and established the company’s Bitcoin accounting framework during his CFO tenure.

In his current role, Visconti leads SWC’s acquisition strategy under the “10 Year Plan,” identifying and evaluating web design agencies for potential purchase, conducting due diligence on targets, and managing post-acquisition integration. His deep experience with small business financials and operational knowledge of SWC’s systems help execute the company’s growth strategy beyond Bitcoin accumulation.

Visconti holds 950,000 shares acquired by converting £19,000 in loan notes at IPO, which represents modest but adequate financial alignment. While the £19,000 investment shows basic commitment, it falls well short of the substantial personal stakes held by other executives and represents minimal financial risk for someone in his position.

Sean Wade – Non-Executive Chairman

Figure 5: Sean Wade | Credit: The Smarter Web Company

Sean Wade (£36,000 annual fee) brings over 30 years of capital markets experience, including founding shareholder status at Liberum Capital and leading TBC Bank’s FTSE 250 listing as Director of International Media and Investor Relations. His primary value lies in his institutional investor network and fundraising capabilities, which are critical for SWC’s continuous equity issuance strategy.

In addition to being a Chairman at The Smarter Web Company, Wade also serves as CEO of Power Metal Resources PLC and Chairman of Focus Xplore PLC, while running his consultancy Scout Advisory Ltd and property ventures. The breadth of commitments raises questions about his capacity to dedicate sufficient time to his SWC chairmanship.

He holds 500,000 shares acquired by converting £10,000 in loan notes at IPO through his consultancy company, Keysford Limited. Like Visconti, the investment is financially modest and falls far short of meaningful skin in the game compared to the substantial personal stakes of Webley and Myers.

Tyler Evans – Non-Executive Director

Figure 6: Tyler Evans | Credit: The Smarter Web Company

Tyler Evans is the Co-Founder and CIO of UTXO Management, an investment firm focused on Bitcoin treasury companies worldwide. Its 210k Capital fund delivered 640% net returns in the 12 months through June 2025. Evans, a University of Alabama Chemical Engineering graduate who entered Bitcoin in 2013, also co-founded BTC Inc., publisher of Bitcoin Magazine and organizer of the global Bitcoin Conference series.

He brings valuable Bitcoin treasury expertise to SWC through his management of a fund specializing in this exact sector. His board positions across Japan’s Metaplanet, Canada’s Matador Mining, and other Bitcoin treasury companies provide strategic intelligence about operational best practices, timing strategies, and market dynamics. For shareholders, this translates to informed guidance on Bitcoin purchase timing, custody arrangements, and treasury management decisions that could significantly impact returns.

However, Evans presents SWC’s most serious governance risk. He simultaneously serves as SWC director and CIO of UTXO Management, SWC’s largest shareholder at 13.42%. Strategic decisions that would favor UTXO’s wider portfolio at SWC’s expense would create a conflict of interest because his fiduciary duty would serve UTXO’s fund performance rather than SWC shareholders.

Evans’ personal financial commitment to SWC is minimal. He received 960,000 shares worth £24,000 as a one-time consultant fee for pre-IPO fundraising work. The stake represents virtually no personal financial risk. His compensation shows basic alignment with shareholders but falls far short of meaningful skin in the game, the same as Wade and Visconti.

Name & Role

Board Membership

Equity / Alignment

Key Strengths

Risks & Concerns

Andrew Webley – CEO & Founder

Yes

9.44% stake (27,418,732 shares, as of Sep 4, 2025). The bulk of personal net worth.

Overboarding: CEO of Power Metal, Chairman of Focus Xplore + C.A. Sperati, runs consultancy and property ventures; minimal financial alignment.

Tyler Evans – Non-Executive Director

Yes

960,000 shares (£24,000 value) granted as pre-IPO consultant fee.

Bitcoin treasury expertise; global perspective; board experience in peer companies.

Most serious governance risk: conflict of interest as both SWC director and CIO of UTXO. Fiduciary duty lies with UTXO performance, not SWC shareholders. Minimal personal alignment.

SWC Leadership Concerns

While CEO Andrew Webley and Bitcoin lead Jesse Myers demonstrate meaningful personal alignment through investments proportional to their influence on company outcomes, the same cannot be said for all members of the board.

According to corporate filings, Wade played a central role in structuring the Uranium Energy Exploration shell that SWC later used for its Aquis “reverse takeover,” a process where a private company acquires a listed shell to gain a stock exchange listing without going through the traditional IPO route. Prior to the transaction, this entity was effectively inactive and carried net liabilities of £921,384.

£562,291 of the debt was owed to Power Metal Resources Plc, where Wade is an executive. Wade, through his company Keysford Limited, received £56,000 consultancy fees from the vehicle while also acting as a major creditor via Power Metal Resources. His involvement across multiple counterparties positioned him to benefit irrespective of the shell’s operational performance.

Former CFO Mario Visconti followed a similar pattern. His accountancy firm received consultancy fees during a period when the company had minimal operations, and he later converted a £19,000 loan into 950,000 shares at IPO.

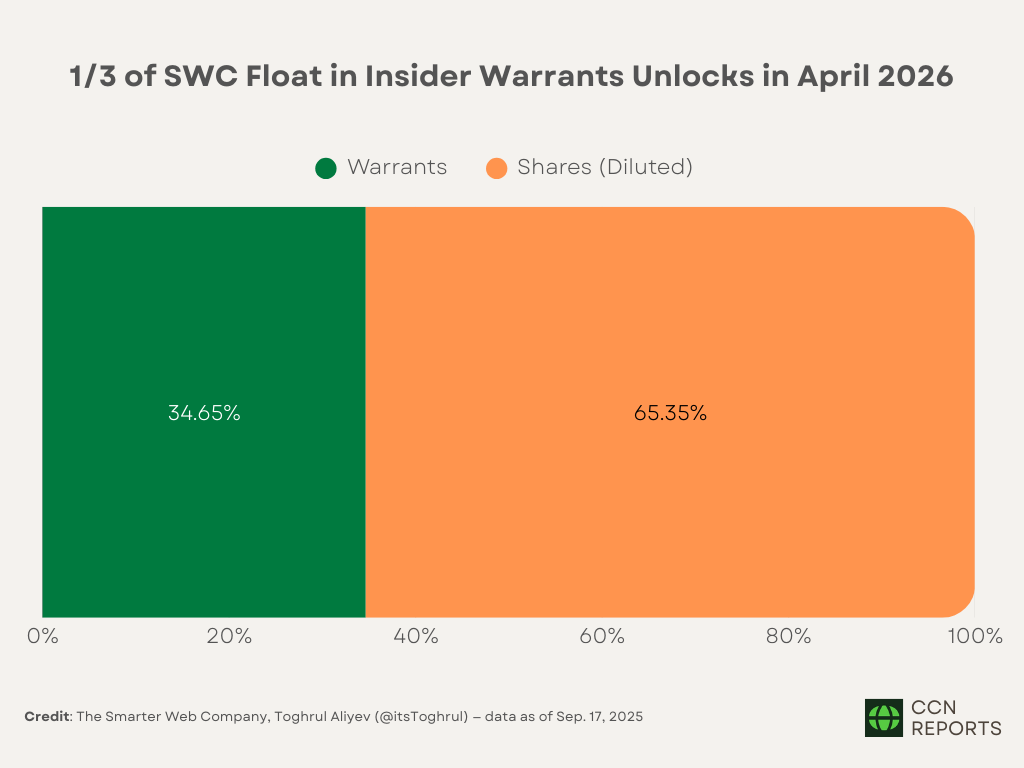

But the most significant structural concern for outside investors lies in the company’s warrant overhang. At IPO, SWC issued 96,066,335 warrants, representing more than 65% of total shares outstanding at that time. The majority of these were allocated to insiders, advisors, and participants in the reverse takeover process. Warrant terms included a nominal strike price of 2.5p, below placement pricing, and short-dated exercise periods.

Key allocations included:

Figure 7: Warrant Allocations by Investor Group | Credit: The Smarter Web Company

As of Sep 17, 2025, warrants represent 34.65% of the 277,275,004 diluted shares in issue.

Figure 8: Distribution of Diluted Ordinary Shares Including Warrant Exercises | Credit: The Smarter Web Company, Toghrul Aliyev (@itsToghrul) — data as of Sep. 17, 2025

The scale of these warrants introduces material dilution risk and creates incentives that are not fully aligned with long-term shareholder value. Maximizing warrant value requires far less than building durable enterprise performance.

In response to shareholder concerns, CEO Andrew Webley said:

When we did the pre IPO funding, several months before the IPO, people were taking more risk (as they were not buying anything with liquidity, the company was not guaranteed to list in the time I suggested, etc), and we had to put a warrant alongside the equity to be able to get it done. At the time, it was hard to raise £2.2m… We have looked at lots of ideas around what to do about the warrants, and there is no easy solution, but perhaps we could ask the two largest warrant holders (UTXO and my family) to agree to a longer time period with say 25% max exercise each year or similar… We will keep looking at ideas, with our advisors, as there will be a good solution somewhere.

While this explanation highlights the practical funding pressures faced during the pre-IPO raise and the intent to explore mechanisms to mitigate dilution, there has been no formal change to warrant terms or structure. The overhang therefore, remains in full effect.

SWC Legacy Web Design Business

The Smarter Web Company operates a web design and digital marketing business with a consistent record of financial efficiency across its 16-year history.

Revenue Structure and Service Portfolio

The company’s revenue model is built around a diversified portfolio of web design services with varying complexity and resource requirements, each designed to maximize revenue per hour worked while securing long-term recurring income streams.

Core Service Offerings:

Readymade Web Design (£795): SWC’s most efficient offering requires only 8 hours of work, generating £99.38 per hour. This template-based solution represents the highest initial revenue efficiency in the portfolio and serves as the entry point for cost-conscious clients.

Lite Web Design (£3,495): A mid-tier solution requiring 40 hours of work that generates £87.38 per hour. This package provides customization options while maintaining strong revenue efficiency.

Pro Web Design (£4,995): The premium option requires 80 hours of work and generates £62.44 per hour. Although the hourly rate is the lowest, it produces the highest single-project revenue, improves cash flow predictability, and attracts clients with complex needs who are more likely to build long-term relationships and purchase additional services.

Recurring Annual Hosting (£247): An essential revenue stream that requires no additional labor once systems are set up. Every client pays the annual fee regardless of their initial package, which creates a high-margin, recurring revenue base and improves predictability of cash flows.

Optional Add-on Services: Variable-priced website support and marketing services that provide additional revenue opportunities from the existing client base.

Unit Economics and Lifetime Value

The Smarter Web Company reports an average client lifespan of six years. The duration reflects the stickiness of hosting and maintenance contracts, which clients continue to pay annually after the initial build. High switching costs, integration with existing systems, and the need for service continuity reduce churn, producing a steady stream of recurring revenue over multiple years.

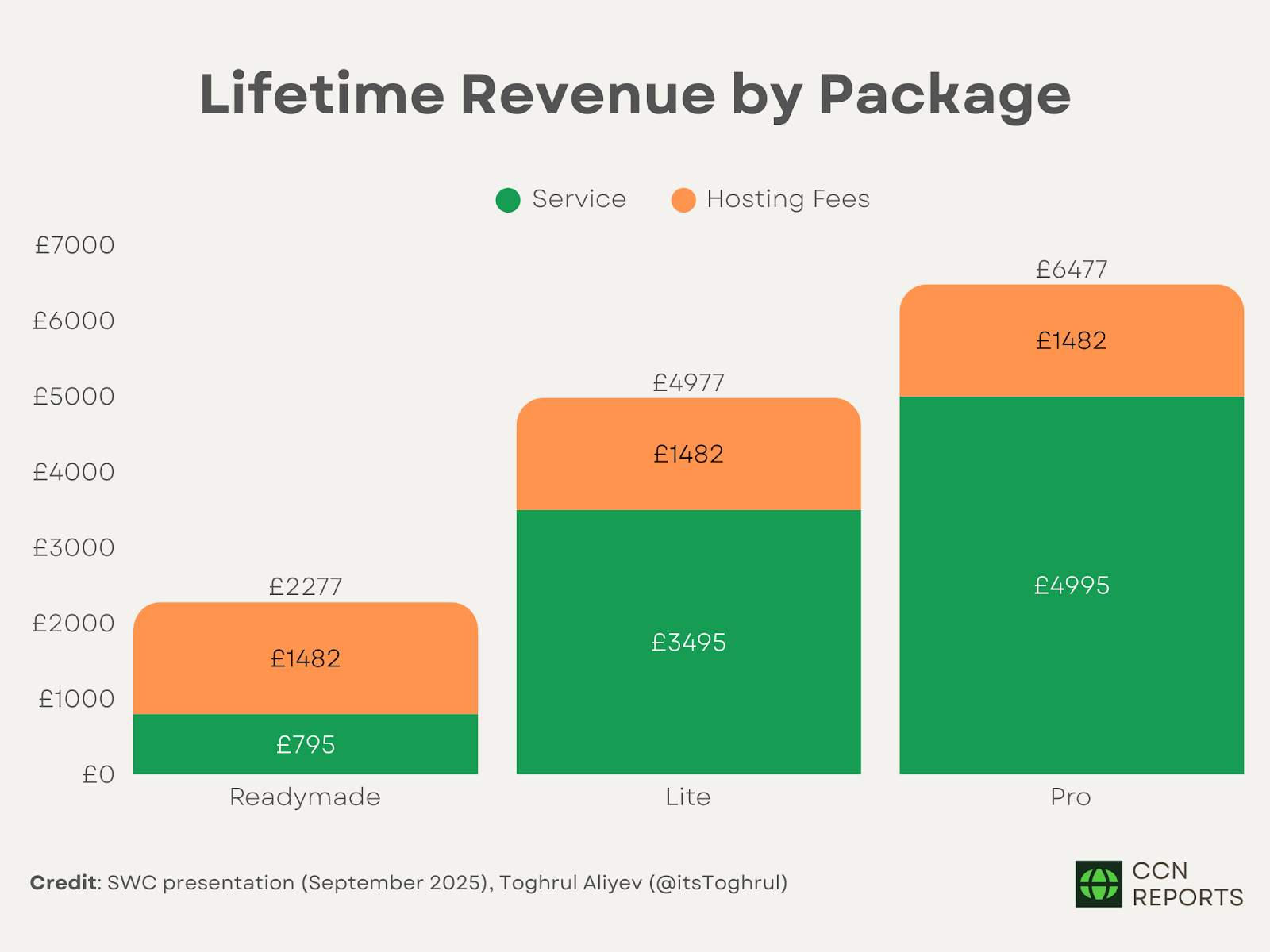

Lifetime Revenue Analysis:

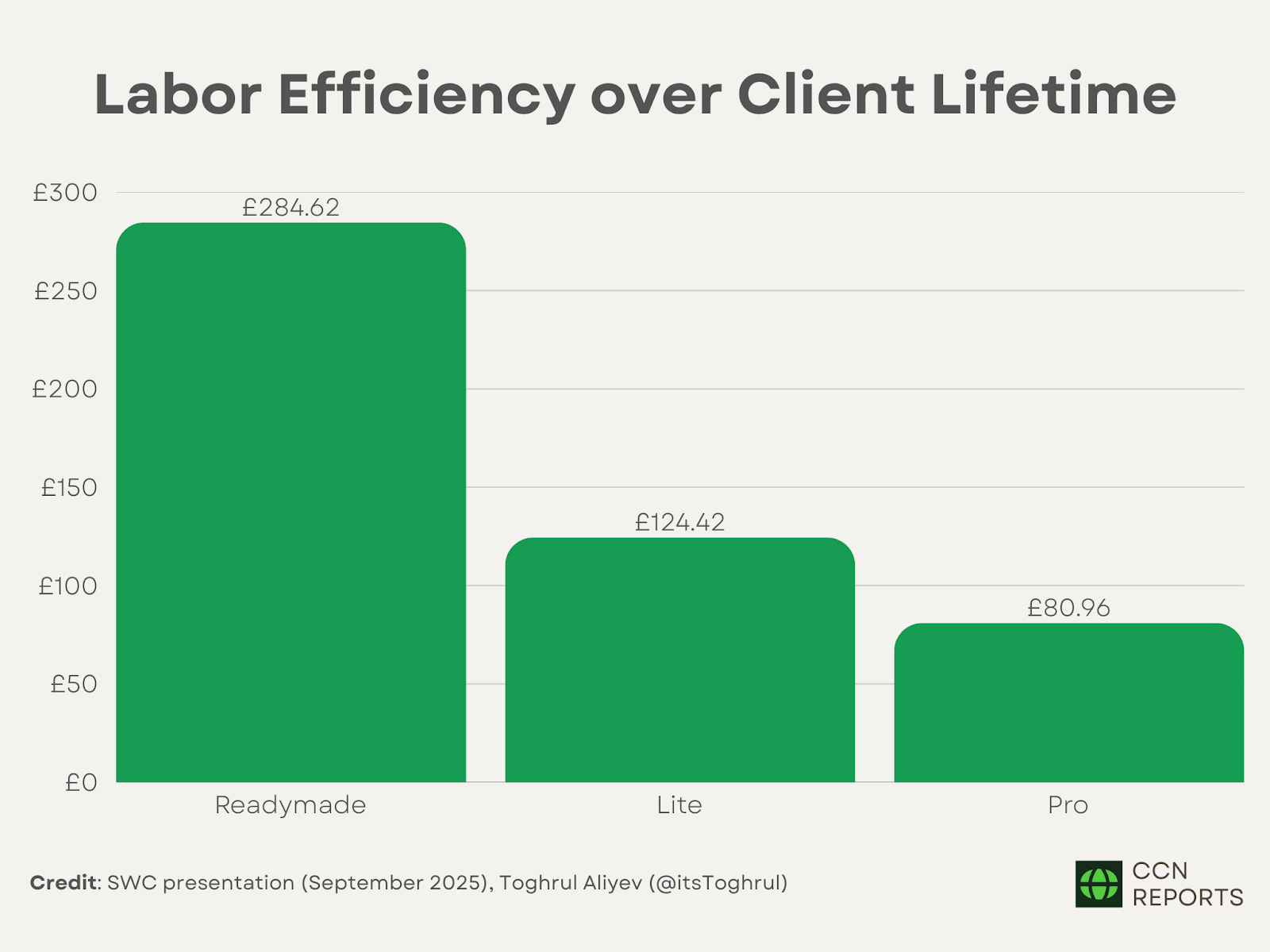

Readymade Package: The service generates £795 in upfront revenue and £1,482 in hosting fees over six years, producing £2,277 in total lifetime revenue. With 8 hours of work required, it delivers £284.62 per hour, making it the highest-return package on an hourly basis.

Lite Package: Generates £3,495 in upfront revenue and £1,482 in hosting fees over six years, resulting in £4,977 of total lifetime revenue. With 40 hours of work required, the package delivers £124.42 per hour.

Pro Package: Generates £4,995 in upfront revenue and £1,482 in hosting fees over six years, resulting in £6,477 of total lifetime revenue. With 80 hours of work required, the package delivers £80.96 per hour.

Figure 9: Lifetime Revenue by Package | Credit: SWC presentation (September 2025), Toghrul Aliyev (@itsToghrul) — data as of Sep. 17, 2025

The analysis shows that Readymade delivers the strongest unit economics and should anchor scalable growth, while Lite works best as an entry point with upsell potential. Pro offers the largest contract size but is less efficient on labor returns and only justifies focus when additional revenue streams or strategic client benefits outweigh the cost.

Figure 10: Lifetime Revenue by Package | Credit: SWC presentation (September 2025), Toghrul Aliyev (@itsToghrul) — data as of Sep. 17, 2025

Proprietary Technology Infrastructure

SWC operates a proprietary content management system (CMS), Editir, that allows clients to manage website content independently after launch. It reduces the company’s ongoing support requirements while maintaining the annual hosting and infrastructure relationship. In effect, the model scales to a larger client base without support costs growing in proportion.

Conventional agencies face scalability constraints because every new client adds a stream of support requests for updates and maintenance. By shifting content management to clients, SWC avoids this bottleneck and can serve more than 250 accounts without a proportionally large support team. The benefit to clients is greater control and flexibility, while the company continues to capture recurring revenue.

Although clients become self-sufficient in managing their content, they remain reliant on SWC for hosting, technical infrastructure, and the CMS platform itself. Each client contributes £247 per year in hosting revenue, adding up to £1,482 across the average six-year relationship. Because little work is required once systems are in place, the income behaves like an annuity, which supports margin stability.

Unlike agencies that rely on third-party platforms such as WordPress or Squarespace, SWC controls its own technology stack. This not only differentiates its service model but also creates switching costs that make client churn less likely, as migrating away requires new infrastructure and training. Technology ownership, therefore, reinforces the durability of the recurring revenue stream.

By minimizing day-to-day support obligations, the CMS also frees management bandwidth for strategic priorities. It is particularly relevant given SWC’s focus on capital allocation and the expansion of its Bitcoin treasury, areas where senior leadership attention directly influences shareholder outcomes.

Income Statement and Balance Sheet

On 25 July 2025, the company released interim consolidated accounts for the half year to 30 April 2025, providing the first group-level view that merges subsidiary performance with holding-company costs.

The filing covered both the operating web design subsidiary, which generated consistent revenues and profits, and the newly listed PLC, which absorbed the one-off costs of the reverse takeover and IPO. As a result, the statutory accounts show headline losses at the remaining profitable on a stand-alone basis.

The income statement shows turnover of £176,000 for the four months from 1 January to 30 April 2025 within the subsidiary, against which operating expenses were low enough to deliver a pre-tax profit of £93,000. Extrapolated across a twelve-month horizon, this implies an annualized revenue run-rate of approximately £528,000 and net profit potential above £270,000. Gross profit for the four months was reported at £166,000, representing a margin above 94%.

At the consolidated level, however, the group reported a loss before tax of £719,566, driven almost entirely by non-operating items. The principal adjustments were the absorption of the shell company’s pre-existing net liabilities (c.£0.92 million) and the recognition of professional and advisory fees linked to the RTO and IPO. These charges were concentrated around the April 2025 listing and are not representative of the operating subsidiary’s ongoing economics. Stripping them out makes clear that the underlying business remained profitable and self-funding at the subsidiary level, while the PLC structure provided the mechanism to secure a listing on the Aquis Exchange.

Measure

Period / Basis

Amount

Notes

Revenue (OpCo)

Jan–Apr 2025

£176,000

Underlying web design + hosting

Profit before tax (OpCo)

Jan–Apr 2025

£93,000

52.8% PBT margin

Gross margin

Jan–Apr 2025

94%

High contribution from hosting and proprietary CMS

Recurring revenue share

Management disclosure (2024)

30%

Hosting + support

Revenue (OpCo)

Pro-forma FY run-rate

£528,000

Annualized from Jan–Apr 2025

PBT (OpCo)

Pro-forma FY run-rate

£279,000

Annualized from Jan–Apr 2025

Net income (OpCo)

Pro-forma FY run-rate

£209,000

Assuming a 25% tax rate

Shares outstanding

Aug–Sep 2025

277,275,004

Latest diluted basic share count

EPS (OpCo only)

Pro-forma FY run-rate

£0.000755

0.0755 pence per share

Cash

Sep 16, 2025

£400,000

RNS as of 16 Sep 2025

BTC holdings

Sep 16, 2025

2,470 BTC

Average cost $111,516/BTC

Financial debt

Sep 16, 2025

£0

No borrowings

Subsidiary-level profitability matters for two reasons.

First, the core service arm generates cash at high gross margins even at a modest scale. Second, those earnings establish a recurring base to cover administrative costs as the group expands its Bitcoin treasury. Unfortunately, the operating arm is not large enough to fund material Bitcoin accumulation, but it is large enough to contribute to corporate costs without reliance on debt.

SWC Valuation

The valuation of SWC’s legacy web design subsidiary requires separating the business from the listed holding company’s Bitcoin strategy and RTO-related distortions.

Earnings multiples (P/E): Digital service companies of modest scale in developed markets generally trade between 10–15x earnings. SWC’s established client base and history of profitability support a mid-range multiple of 12x. Applying this to £279,000 pre-tax earnings yields £3.35 million equity value.

Discounted cash flow (DCF): Discount rate at 12% (a small-cap risk premium), initial growth at 5%, which is consistent with market expansion but below high-growth digital peers, and terminal growth: 2%, in line with long-term GDP growth expectations. This produces an enterprise value of £2.96 million.

Client lifetime value (LTV): With average annual client revenue of £2,112 and a six-year lifespan, client LTV approximates £11,952. Multiplying by 250 clients produces an equity proxy of £2.99 million.

Averaging the three methods yields a valuation of £3.1 million for the web design subsidiary. On a per-share basis (277.3m diluted shares), this equates to roughly 1.1 pence per share.

At current valuations, the legacy web design subsidiary contributes only around 1% of the group’s market capitalization. When viewed through a fair value lens, this contribution is essentially immaterial. Any attempt to calculate per-share value based on the subsidiary’s cash flows produces a result so small that it functions as little more than a rounding error in the context of the overall equity valuation. The company’s share price is instead determined almost entirely by the scale and market value of its Bitcoin reserves.

Figure 11: Components of SWC’s Market Value | Credit: The Smarter Web Company, Toghrul Aliyev (@itsToghrul) — data as of Sep. 17, 2025

With reserves of 2,470 BTC purchased at an average cost of $111,516, and with Bitcoin trading around $117,000 (£85,500) on September 17, 2025, the mark-to-market value of the reserve stands at approximately £211.2 million.

Adding the £400,000 in cash reported in the September 16 RNS, together with £3.1 million attributed to the underlying operating business, produces an estimated equity value of £214.7 million. Against a diluted share count of 277.3 million, this implies a fair value per share of roughly £0.77 as of September 17, 2025.

SWC Bitcoin Treasury Strategy & Execution

Investment Framework

During our interview, CEO Andrew Webley underlined that SWC does not attempt to time the Bitcoin market. Once capital is secured, the company deploys it into Bitcoin within roughly a week, resulting in purchases on most trading days during that period.

The policy of immediately converting equity inflows into Bitcoin ensures that shareholder capital is not left sitting in fiat currency. For a company whose thesis rests on the idea that fiat erodes in real terms while Bitcoin represents a superior long-term store of value, this approach maintains strict alignment with its stated philosophy.

At the same time, the “always buying the top” approach carries its own limitations. Of course, timing Bitcoin is a losing strategy. Most attempts to trade around volatility underperform simple accumulation. However, the fact remains that committing all inflows at once can expose the company to the risk of systematically buying at cyclical highs.

In practice, the policy maximizes long-term Bitcoin-per-share exposure, but it comes at the cost of short-term balance-sheet vulnerability, since Bitcoin could trade below the company’s average acquisition price of $111,516 in the near future.

Funding Mechanisms

The Smarter Web Company finances its Bitcoin treasury expansion entirely through equity-linked channels. Private placements have been carried out at prevailing market prices, which avoids discounted issuances. The company also operates an At-The-Market (ATM) facility, capped at 20% of daily trading volume and used only on rising days, thus reducing pressure on the share price.

That said, an ATM remains dilutive by nature. The only way shareholder value grows under this model is if Bitcoin appreciation outpaces the dilutive effect of new issuance. When that happens, Bitcoin per share increases, and the program delivers accretive results. When it does not, dilution outweighs asset growth, and value per share declines.

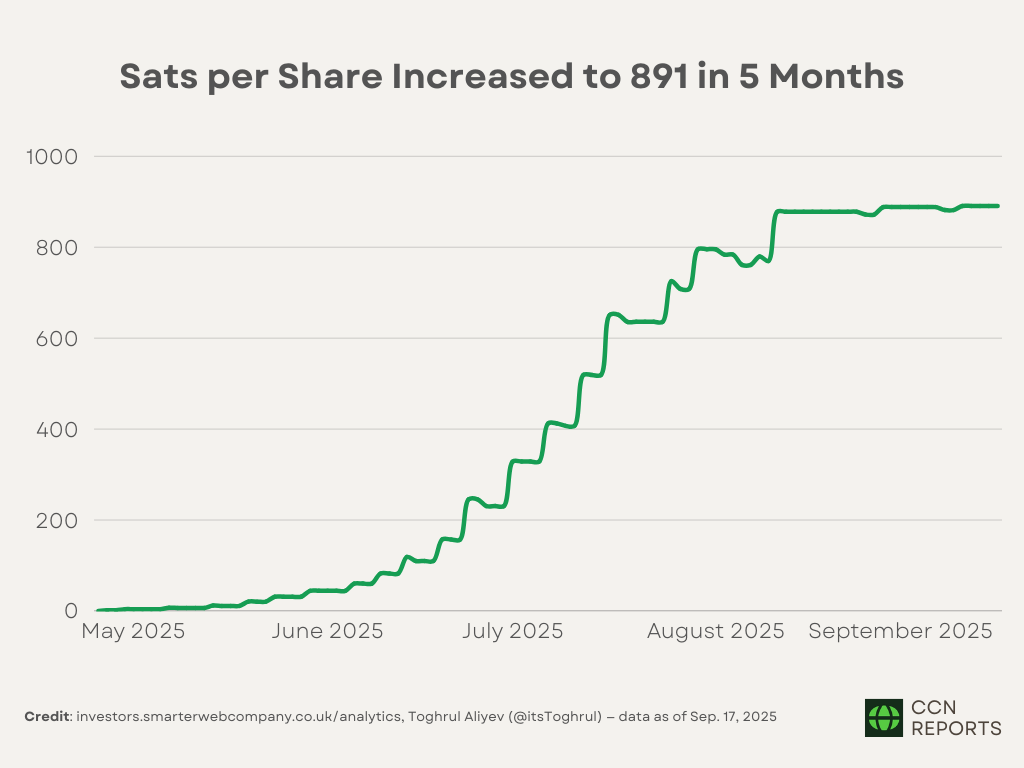

Up to now, SWC has managed to maintain a rising trend in Bitcoin per share, though the pace has slowed due to both the market weakness in late summer and the company’s limited ability to issue stock without eroding shareholder value.

Figure 12: Sats per SWC Share | Credit: investors.smarterwebcompany.co.uk/analytics, Toghrul Aliyev (@itsToghrul) — data as of Sep. 17, 2025

The third way The Smarter Web Company raises money is through Smarter Convert, a £21 million Bitcoin-denominated convertible launched in August 2025 and fully subscribed by institutional investor TOBAM. It carries a 0% coupon and was priced at a 5% premium to the market reference price of £1.95, setting conversion at roughly £2.05 per share.

If the stock trades 50% above that level for 10 consecutive days in the second half of the 12-month term, SWC can force conversion. Full conversion would issue around 7.7 million new shares, and the structure caps exposure at about 30% of treasury assets, which limits overreliance on the facility.

If investors choose not to convert, repayment at maturity is made in Bitcoin at the current prices, with bondholders receiving 98% of the principal and SWC retaining 2%. Should that occur when Bitcoin trades below the company’s £111,516 acquisition cost, SWC would need to deliver more coins back to the bondholder than it initially raised. The outcome effectively reverses part of the accumulation program and represents a step backwards for the long-term treasury strategy.

Competitive Landscape

Among listed Bitcoin treasuries, SWC’s advantage rests on two pillars: its first-mover dominance in the UK and its unprecedented pace of acquisition.

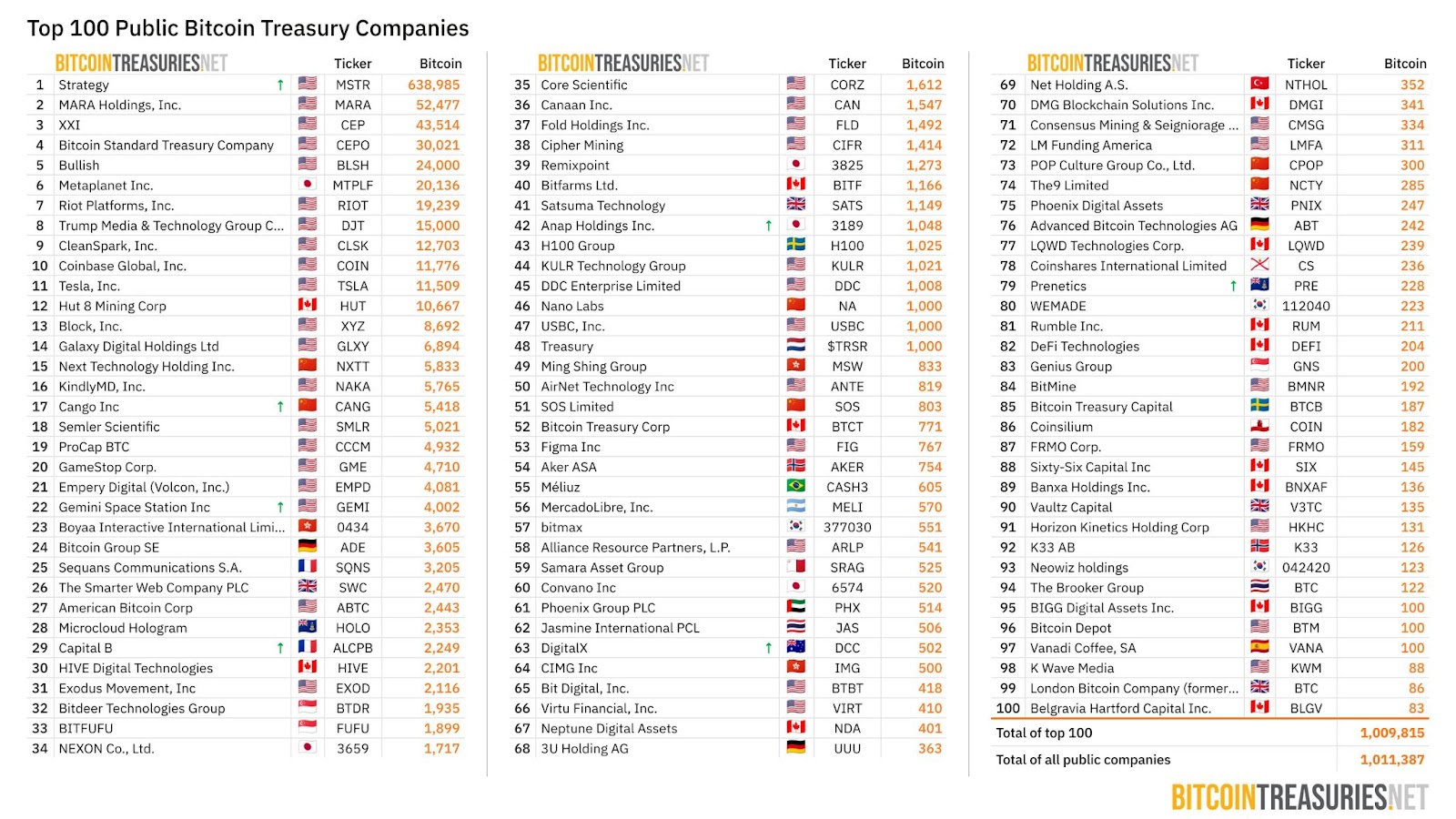

SWC is the most dominant Bitcoin treasury company headquartered in the United Kingdom. In the global ranking of the Top 100 Public Bitcoin Treasury Companies, only a handful of UK-based firms appear: Satsuma Technology, Phoenix Digital Assets, Vaultz Capital, and London Bitcoin Company (formerly Vinanz). And none of these competitors have reserves that approach SWC’s 2,470 BTC.

Figure 13: Top 100 Public Bitcoin Treasury Companies | Credit: BitcoinTreasuries.NET

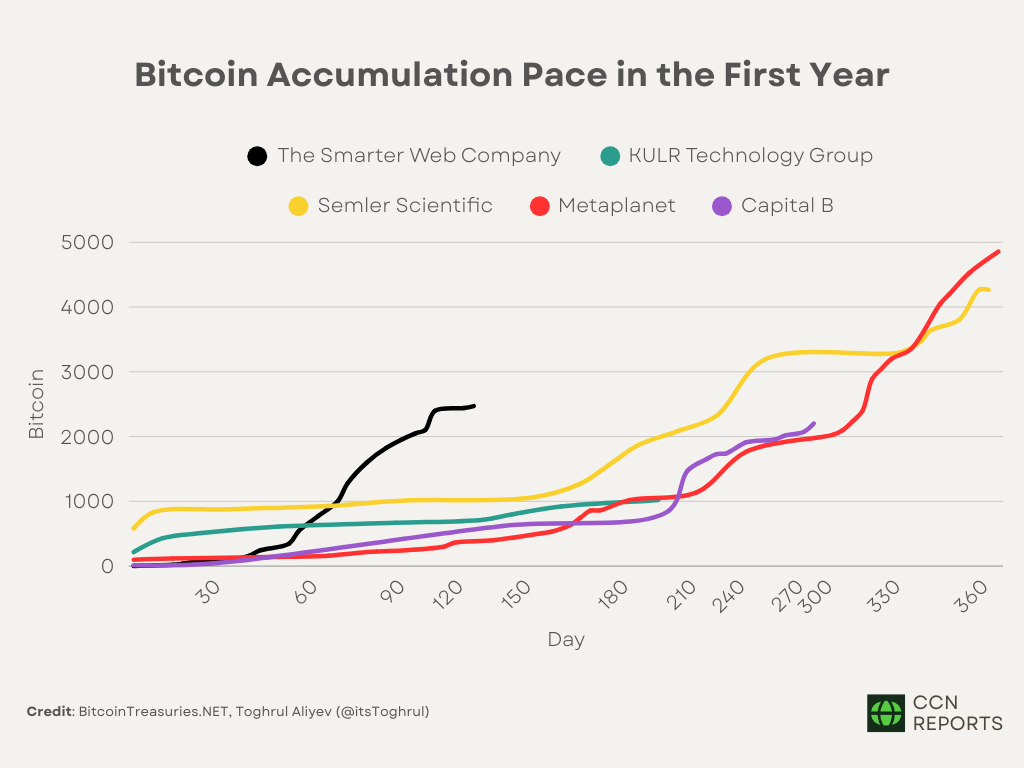

SWC has also distinguished itself as the fastest accumulator in the global Bitcoin treasury sector.

Figure 14: Bitcoin Accumulation Pace in the First Year | Credit: BitcoinTreasuries.NET, Toghrul Aliyev (@itsToghrul)

In its first six months of treasury operations, the company achieved a cumulative Bitcoin yield of 56,909%. By comparison, Strategy (United States) and Metaplanet (Japan), the two global benchmarks for listed Bitcoin treasuries, have delivered long-term Bitcoin yields of 251% and 359%, respectively, since inception.

Figure 15: Cross-Company Bitcoin Yield Comparison | Credit: Toghrul Aliyev (@itsToghrul) — data as of Sep. 17, 2025

SWC Price Projections

Before making price projections for The Smarter Web Company, we recommend reading my Strategy piece and Giovanni Santostasi’s blog to fully understand the Bitcoin Power Law Theory.

In short, the theory suggests that Bitcoin’s price follows a power-law growth curve, roughly Price = A * Days since Genesis^5.688, which implies consistent, scale-invariant growth over time. It provides a framework for understanding Bitcoin’s long-term price behavior and, by extension, the valuation of companies that hold BTC as a treasury asset.

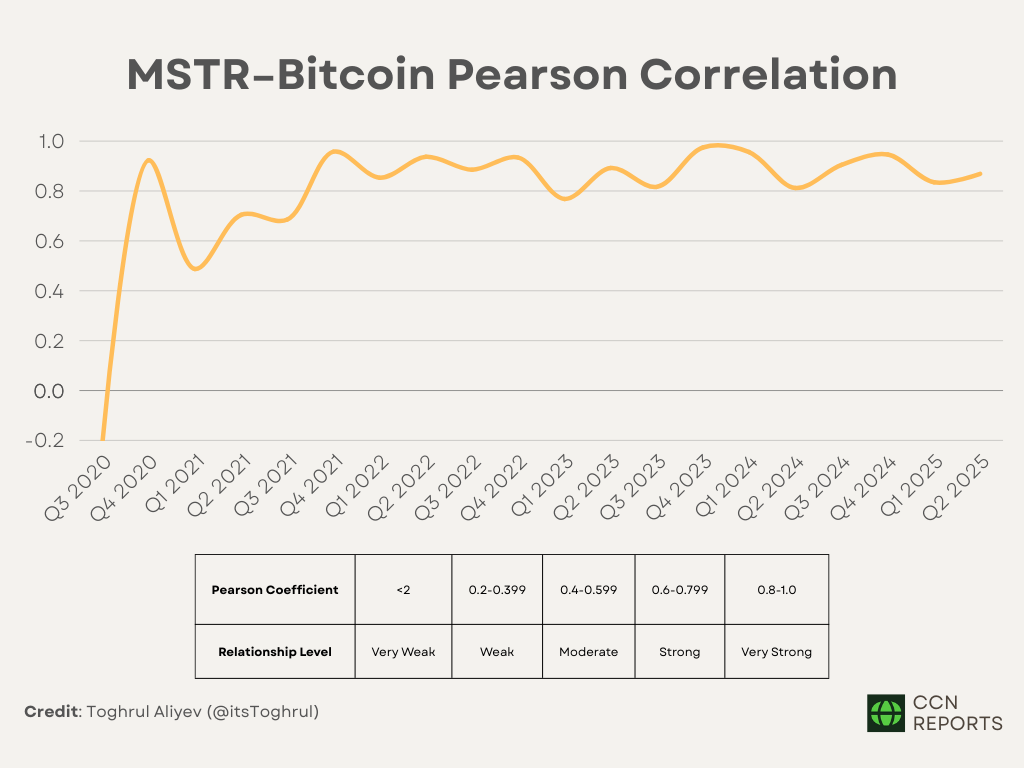

The phenomenon is most clearly demonstrated by Strategy (MSTR), which has maintained a Pearson correlation coefficient above 0.8 with BTC since adopting its Bitcoin treasury policy in August 2020. Since then, MSTR’s equity price has developed its own power-law relationship with a slope coefficient of approximately 7.2, compared to Bitcoin’s 5.7, which indicates that the company’s stock provides leveraged exposure to Bitcoin’s underlying growth trajectory.

The mechanism driving this correlation operates through several channels.

First, companies that hold Bitcoin as their primary asset naturally inherit Bitcoin’s volatility characteristics, creating direct sensitivity to price movements.

Second, those that continuously accumulate Bitcoin introduce a compounding dynamic that resembles a power law effect. Each purchase adds marginal exposure, but over time, the aggregate reserve grows non-linearly. In other words, the company’s equity price can trace a steeper power law slope than Bitcoin itself, as seen with Strategy, where consistent accumulation amplified its long-term correlation with Bitcoin and created a leveraged growth curve.

Third, the market tends to value such companies as a multiple of their Bitcoin net asset value (mNAV). Valuations typically fluctuate within broad premium or discount bands relative to underlying Bitcoin holdings, with premiums expanding during bull markets and compressing during bear markets.

However, despite all this evidence, the Bitcoin treasury company sector remains in its infancy. The available price history is limited to roughly five years for MSTR and only one to two years for newer entrants. In the case of SWC, the track record is not even six months.

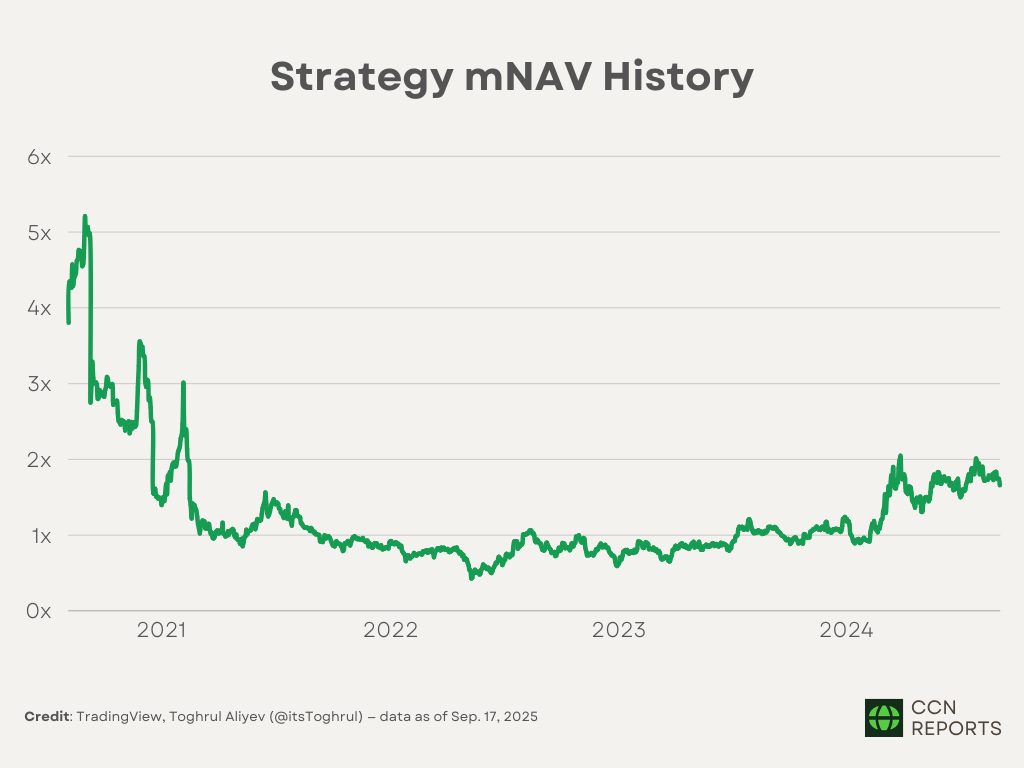

Because MSTR was the only company to experience a bear market in 2022 while holding a significant Bitcoin reserve, its price history remains the only reference point. During that period, MSTR’s equity traded at a discount of up to 0.5× mNAV, indicating that Bitcoin treasury stocks can face drawdowns as steep as half their net asset value relative to underlying holdings.

Figure 17: Strategy mNAV History | Credit: TradingView, Toghrul Aliyev (@itsToghrul) — data as of Sep. 17, 2025

SWC Power Law Model

Given the theoretical framework and empirical precedent, we have developed a specific power law model for The Smarter Web Company. Our analysis yields the formula:

SWC Power Law Price = 0.4655 *(BTC Power Law Price / 100,000)^3.95

The model primarily applies to the US-listed version of SWC stock (TSWCF) but demonstrates reasonable accuracy for the UK-listed shares (SWC) with adjustments for GBP/USD foreign exchange fluctuations. The power law channel operates with an upper trendline using a 10x multiplier and a lower trendline using a 0.1x multiplier.

SWC’s power law coefficient of 0.4655 and exponent of 3.95 reflect the company’s specific characteristics as a smaller Bitcoin treasury company with higher volatility relative to Bitcoin’s base power law. The lower exponent compared to Bitcoin’s 5.8 suggests that while SWC benefits from BTC’s growth, it exhibits different scaling characteristics due to factors including company size, accumulation speed, and market liquidity.

When applied to recent data, the model shows weak explanatory power across the full sample (R² ≈ 0.10). Over the most recent 60 days, the fit improves to R²= 0.8.

On one hand, the low R² points to a poor fit. On the other hand, the short-term correlation looks solid. For a company like SWC, where data is still limited, it is tough to build a model that works over the long run without frequent readjustments. Focusing on R² at this stage, when the stock doesn’t even have six months of price history, is not viable.

If a different power law model is applied with the slope it has today, the implied stock price would reach billions within three years.

SWC Power Law Price (Unrealistic) = 1.08 * (BTC Power Law Price / 100,000)^19.12

BTC Power Law Price on Dec 31, 2028 = $303,568.79

SWC Power Law Price (Unrealistic) = 1.08 * ($303,568.79 / 100,000)^19.12= $1,795,477,146.64

Figure 18: SWC Power Law Fit with High R² but Unrealistic Projection | Credit: TradingView, Toghrul Aliyev (@itsToghrul)

That is simply unrealistic. The initial version is far more grounded, though it depends on assumptions and uncertain factors that may or may not play out.

One assumption is continued BTC accumulation by SWC. Historical behavior points in that direction, but policy can change.

A second assumption is the trajectory for BTC held and shares outstanding. The power law formula establishes a structural link between Bitcoin and SWC’s equity price, but its relevance depends on variables that fluctuate with strategy and market conditions. SWC’s Bitcoin purchases are opportunistic, and equity issuance is shaped by external demand. A deterministic forecast would therefore miss the volatility inherent in those dynamics.

To capture this uncertainty, I applied a Monte Carlo framework. In practice, Monte Carlo means generating a large number of simulated paths for BTC purchases and share issuance, each with randomized inputs that stay within predefined ranges. The outcome is not a single line but a distribution of possible futures.

Data anchor and horizon:

History used for calibration: April–September 2025. BTC rose from 0 → 2,470. Shares rose from 146M → 277M.

Projection window: Month-ends from September 2025 → December 2026. September 2025 is prorated for the half month remaining after September 16.

How the simulation works:

Each month, the model draws how many buy bursts occur and how large they are.

Purchases occur in whole BTC only (minimum 1 BTC per event).

Larger BTC stacks slow future buying through a saturation rule.

Equity issuance has two parts: purchase-funding shares and a separate ATM program that opens wider when the mNAV premium is higher.

Bitcoin price follows the power law at the month-end.

The engine runs 400 paths per scenario. Results are reported as p10 / p50 / p90: bear / base / bull lines.

Findings

Scenario

BTC holdings (p10 / p50 / p90)

Shares (M) (p10 / p50 / p90)

Base

5,560 / 6,512 / 7,342

497 / 538 / 575

Bear

4,630 / 5,056 / 5,430

361 / 375 / 391

Bull

8,990 / 9,959 / 10,950

574 / 628 / 695

The power-law channel for SWC must pass through facts the market already knows and a balance-sheet state that the operating model can plausibly deliver. I therefore anchored the curve with two points:

Early anchor (price): the lowest converted close for TSWCF in the opening month, $0.04567764 on 28-Apr-2025. The UK line (SWC) was converted to USD using contemporaneous GBPUSD so that both listings map to one series.

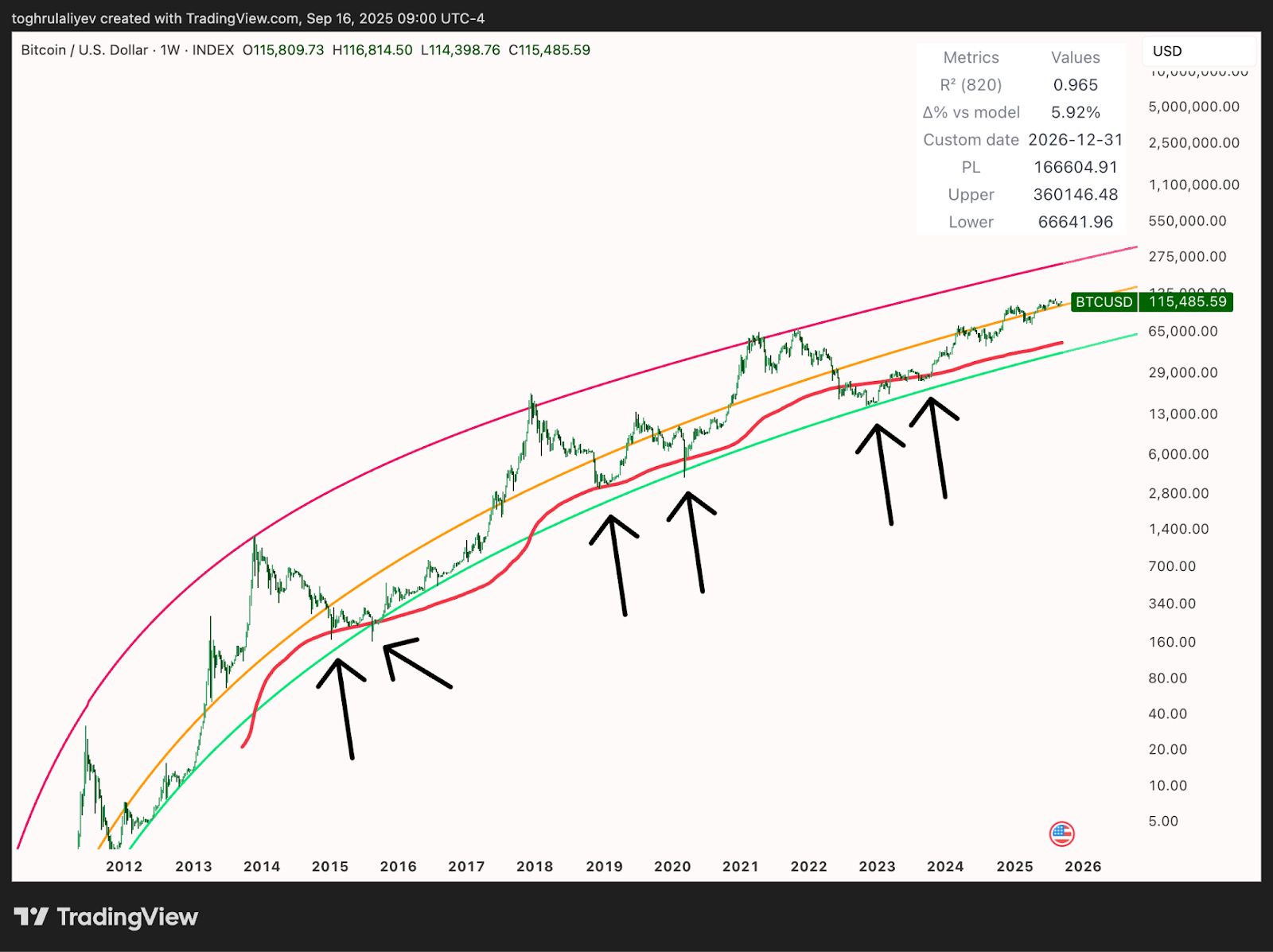

Forward anchor (balance sheet at cycle floor): the Base-case p50 end-state from the Monte Carlo: 6,500 BTC and 538 million shares at Dec-2026. Cycle theory implies BTC trades near the lower power-law band / 200-week zone during a retrace; I set the reference at $70,000/BTC.

Figure 19: Bitcoin Power Law | Credit: TradingView, Toghrul Aliyev (@itsToghrul)

The forward anchor implies:

NAV = 6,500 BTC * $70,000 per BTC = $455 million

NAV/share = $455M / 538M shares≈ $0.85/share

A 0.40x mNAV (more conservative than MSTR’s ~0.50x trough in 2022 bear market) yields an equity price of:

$0.85/share * 0.4 mNAV = $0.34/share

The channel normalization follows from those two anchors. The April low fixes the early intercept; the Dec-2026 floor case fixes the forward level. Fitting a single power-law curve between them, under the requirement that SWC’s path remains inside a realistic band around Bitcoin’s own power-law, produces the 0.4655 coefficient and 3.95 exponent reported earlier. The result preserves the observed early print, respects the balance-sheet arithmetic at a conservative BTC price, and avoids the pathological slopes that would send the equity to implausible levels within a few years.

Figure 20: SWC Power Law | Credit: TradingView, Toghrul Aliyev (@itsToghrul)

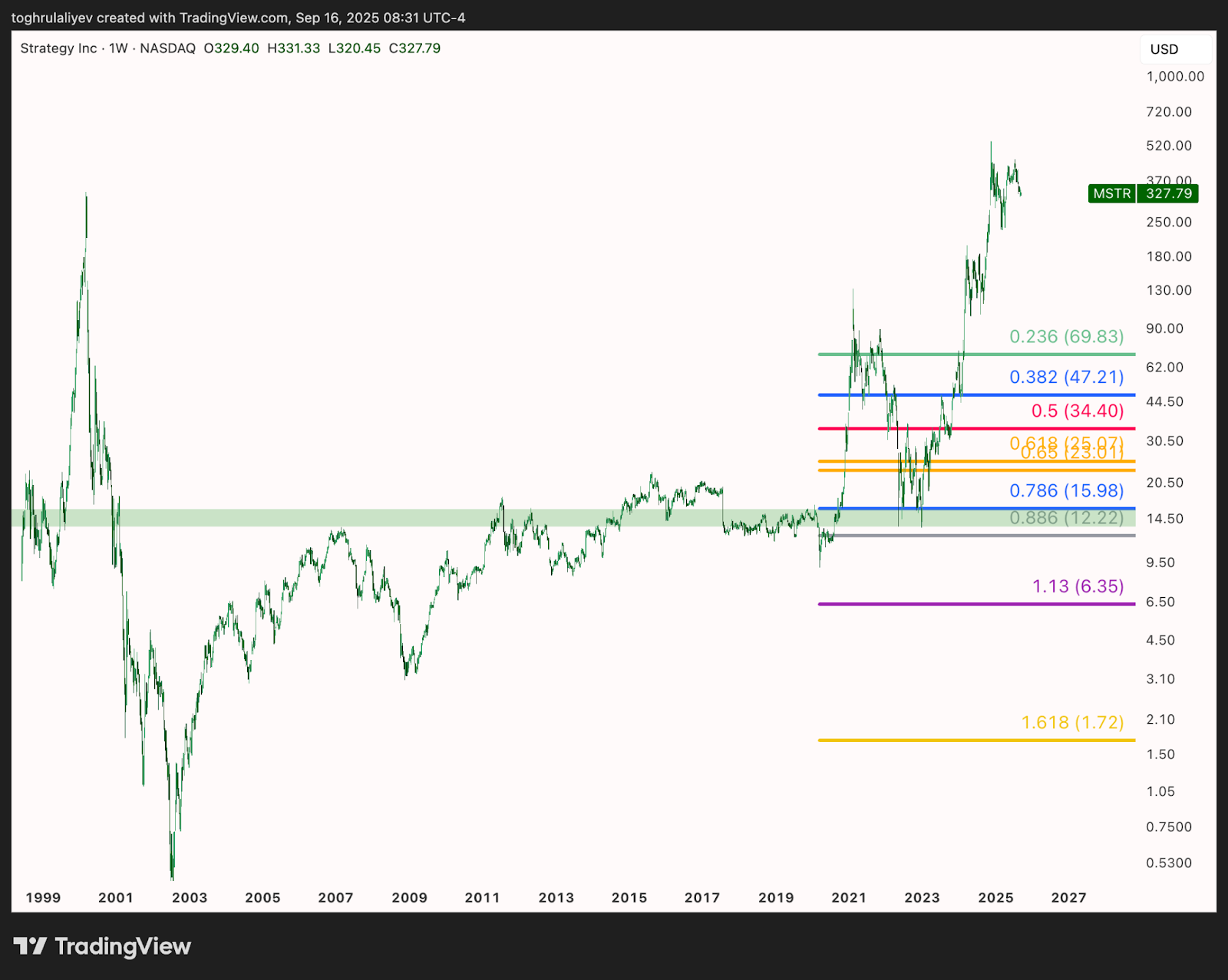

Additionally, the $0.34 anchor sits just above the Fibonacci golden-pocket retracement (61.8%–65%) measured from the April 2025 all-time low to the June 2025 all-time high, which translates to $0.25–$0.30 on TSWCF or ($SWC/100)*GBPUSD. That same band matches the first post-IPO resistance shelf observed during the initial advance, $0.25–$0.33. Confluence between the retracement band and the early resistance shelf sets a support zone immediately below the model floor, which makes $0.34 a logical and probable downside mark for the future. Alignment is also seen at the 1.13 retracement from the June high to the September trough, which coincides with the upper 10× power-law boundary.

Figure 21: SWC Power Law with Fibonacci Levels | Credit: TradingView, Toghrul Aliyev (@itsToghrul)

For context, MSTR’s rebound from its 2022 lows began at a well-defined multi-year support zone established over more than two decades of trading history. SWC does not possess an extended price record, so the analysis must rely on what is available and that is the observable range in 2025.

The analysis of The Smarter Web Company shows a business model that blends elements of a traditional operating enterprise with the characteristics of a financial vehicle. Leadership quality and alignment stand out as differentiators. CEO Andrew Webley and Head of Bitcoin Strategy Jesse Myers have meaningful personal stakes in the outcome, while other directors hold positions that carry more modest financial exposure and, in some cases, potential conflicts of interest. The presence of large warrant allocations also creates a structural overhang that may dilute long-term shareholders, even if the mechanism initially served a practical funding purpose.

The legacy web design business demonstrates durable profitability at the subsidiary level, producing recurring revenue and high margins. However, its scale is insufficient to transform SWC into a self-funded Bitcoin accumulation platform. The operating arm functions instead as a financial anchor, covering administrative expenses and providing a consistent base of positive cash flow while the group relies primarily on capital markets to fund treasury expansion.

Against that backdrop, valuation depends almost entirely on the trajectory of Bitcoin reserves and the company’s ability to maintain accretive issuance. The power law model provides one structural framework for mapping potential outcomes, but its application to SWC rests on assumptions about Bitcoin price cycles, treasury accumulation, and share issuance that are inherently uncertain.

As observed, the model rests on assumptions that may or may not hold, and on technical analysis that provides structure but not certainty. The cycle theory has guided Bitcoin investors for over a decade, yet its persistence cannot be guaranteed.

The current macro environment differs from prior cycles in several respects, including the presence of large institutional allocators and a regulatory approach that is in many jurisdictions more permissive toward cryptocurrencies than in earlier periods. These factors may extend the cycle, compress it, or eliminate the pattern.

Markets, however, always rotate between overbought and oversold conditions. For Bitcoin, the oversold condition has historically coincided with the 200-week moving average and the lower boundary of the power-law channel. Should such conditions emerge again in the coming year, the base-case scenario (p50) is the most probable outcome.

If macroeconomic conditions deteriorate further and 2026 develops into a year-long recessionary environment, the bear-case p50 scenario becomes more plausible, with reserves and equity levels tracking toward the lower end of modeled outcomes.

Conversely, if the cycle structure fails altogether and Bitcoin continues to trade above prior ceilings, the bull-case p50 scenario is the relevant guidepost.

It is important to emphasize that SWC price projections represent theoretical scenarios based on historical patterns and mathematical relationships that may not persist in the future. The Bitcoin treasury space remains nascent, with limited available data.

Recent events have already demonstrated the limitations of existing models. For example, Tennyson Securities proposed a model using 3x to 10x mNAV levels as support and resistance for The Smarter Web Company. However, this model was quickly invalidated when SWC dropped well below the predicted range, falling to approximately 1.68x mNAV. While the model could be adjusted to 1x/10x to accommodate wider ranges, such post-hoc modifications highlight the inherent uncertainty in the modeling approach of Bitcoin treasury companies.

Additionally, the R-squared value of 0.1 for our SWC power law model, while improving to 0.8 over recent periods, still indicates substantial unexplained variance in the relationship. A more statistically rigorous model would require a higher correlation coefficient, but achieving this results in projections that reach unrealistic price levels, which clearly exceed any reasonable valuation framework.

The purpose of this analysis is not to provide definitive price targets but rather to establish a framework for interpreting potential future price movements based on the best available theoretical and empirical evidence. As the Bitcoin treasury sector continues to evolve, these models will require ongoing refinement and validation against actual market outcomes.

So, while the power law approach represents the most theoretically grounded method currently available for projecting SWC valuations, it cannot eliminate the substantial uncertainties inherent in both the model and the emerging sector. The output should therefore be regarded as a structured guide to possible outcomes rather than as a precise forecast.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Toghrul Aliyev is the Head of Research who began his journey in crypto in 2021. It all started with a Reddit post that went viral, leading to a writing position while he was still in medical school. As he learned more about crypto, he became deeply interested in it and decided to focus entirely on this field after completing his medical degree and becoming a doctor.

Toghrul specializes in thorough research, always aiming to find details others might miss. He also has a strong understanding of stocks, real-world asset tokenization, and related areas. He is skilled in Python and SQL, which he uses to improve his crypto analysis through data analytics and data science.

When he’s not working, Toghrul enjoys sports, hiking, reading philosophy, such as Seneca's works, and playing story-driven video games.