U.S. government debt yields rose on Monday, extending their recent string of gains after Treasury Secretary Steven Mnuchin provided a sense of optimism toward upcoming China trade talks.

Despite the rally, investors shouldn’t get too excited about a sustained rise in bond yields given the current state of play in global finance.

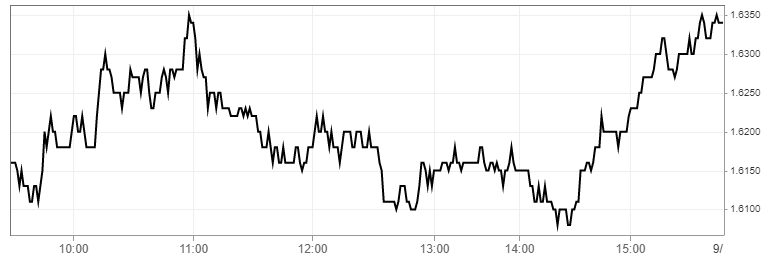

Treasury Yields Extend Rally

Yields were higher across the board on Monday even as demand for riskier assets such as stocks wavered. The yield on the benchmark 10-year U.S. Treasury note peaked at 1.640%, the highest in a month, according to CNBC data. At last check, the yield was up 8.4 basis points at 1.634%.

U.S. 10-year Treasury yield extends rally on Monday. | Image: CNBC

The 2-year yield, which had inverted with its 10-year counterpart last month, was up 5.9 basis points at 1.587%.

Treasury yields, which move inversely with their price, are used to gauge economic sentiment. An inverted yield curve is viewed by economists as one of the most reliable indicators of recession.

Don’t Be Bullish on Bond Yields

Treasury Secretary Steven Mnuchin tries to sprinkle optimism on fractured U.S.-China trade talks. | Source: Alex Wong / Getty Images / AFP

Michael Schumacher, the head of Wells Fargo’s rate strategy, told CNBC recently that the bank “really can’t buy into” the recent rise in bond yields.

In other words, demand for U.S. Treasurys will only increase as investors come to grips with myriad issues including Brexit, Hong Kong protests and trade uncertainty.

“We think about all the catalysts out there: trade, Brexit, Hong Kong,” Schumacher told CNBC’s “Futures Now” broadcast, while drawing attention to frayed relations between the United States and China.

“Is it in Donald Trump’s interests right now to try and strike a deal? Probably not, most likely not until early next year. What about the Chinese government? We’re not so confident there’s a deal coming there, either,” he said. “The way we look at it is, yeah, there’s a brief period of good news right now, but you’ve got so many choppy factors out there.”

The “good news” Schumacher referenced is the recent agreement by the United States and China to resume trade negotiations early next month. But even that isn’t convincing as both sides remain far apart on several key issues ranging from Chinese industrial policy to intellectual property. At this stage, a trade agreement before the 2020 U.S. presidential election seems highly unlikely.

Political uncertainty, weakness in economic growth and trade-war drama are all expected to incite another bond-buying frenzy. The only question is to what extent central banks will ease monetary policy to counteract these issues. The bigger question is whether another round of quantitative easing and ultra-low interest rates will have their desired effect.

Financial Editor of CCN.com, Sam Bourgi has spent the past decade focused on economics, markets, and cryptocurrencies. His work has been featured in and cited by some of the world's leading newscasts, including Barron's, CBOE, Yahoo Finance, and Forbes. Sam is based in Ontario, Canada and can be contacted at [email protected] or at LinkedIn.