UK Adopts 'No Gain, No Loss' Tax Rules for Crypto Lending and DeFi

Share

Key Takeaways

Depositing into DeFi lending protocols or liquidity pools no longer triggers immediate capital gains tax.

Tax liability defers until a genuine economic disposal: a sale, a swap outside DeFi, or a fiat conversion.

CARF reporting from UK platforms to HMRC began on January 1, 2026, expanding surveillance alongside the relief.

HM Revenue and Customs (HMRC) confirmed on February 12, 2026, that the UK government is advancing a No Gain, No Loss, or NGNL, tax treatment for specific decentralized finance activities covering lending and liquidity provision.

The confirmation formalized a direction signaled in HMRC’s November 26, 2025, consultation outcome, which acknowledged that existing rules produced an outcome widely regarded as economically incoherent: users faced capital gains tax charges simply for depositing tokens into DeFi protocols and later withdrawing them, even when they received back the same assets with no genuine economic disposal having occurred.

HMRC in the UK is adopting new tax legislation related to crypto lending and liquidity pools.

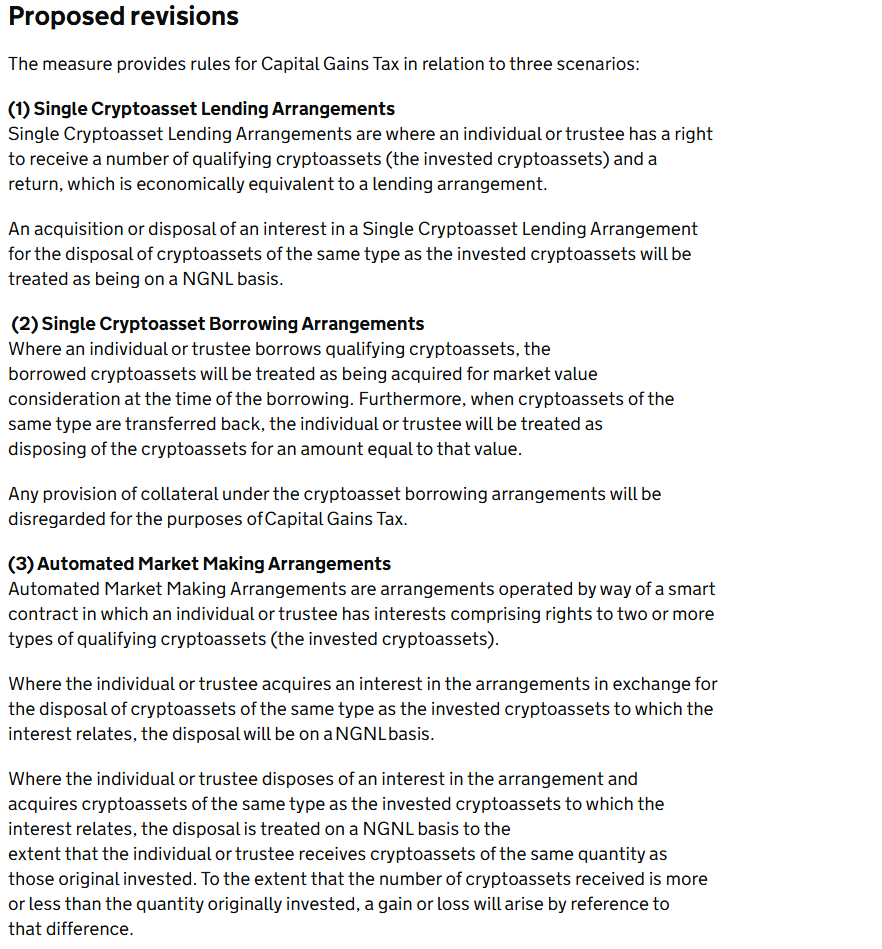

Main take is that deposits into lending protocols will be treated as ‘no gain, no loss’ (NGNL), which effectively defers capital gains tax until an economic disposal. Also underlying…

Under the NGNL framework, transferring crypto assets into qualifying lending protocols or liquidity pools does not trigger a capital gains tax event.

The taxable disposal is deferred until a genuine economic event occurs: selling the asset, swapping it outside a DeFi context, or converting to fiat.

The UK joins a small group of jurisdictions that have formally aligned crypto tax treatment with the economic reality of DeFi participation rather than its mechanical form.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

The practical significance for DeFi users is substantial. Under the prior rules, a user depositing Ethereum into an Aave lending pool at one price and withdrawing it weeks later at a higher price faced a capital gains liability on that difference, even though they never sold a single token and remained fully exposed to ETH’s price movements throughout.

Repeating that across hundreds of DeFi interactions across a tax year produced compliance costs and tax liabilities that bore no relation to whether the user had actually profited in any economically meaningful sense.

The NGNL framework eliminates that phantom liability for qualifying transactions. Routine deposits into lending pools, withdrawals at redemption, and liquidity provision through automated market makers now carry neither gain nor loss at the point of movement.

The cost basis of the original position carries forward to the eventual genuine disposal, preserving the tax system’s ability to capture real economic gains while removing the administrative burden of treating every protocol interaction as a taxable event.

Tax treatment of crypto asset loans and liquidity pools. | Source: gov.uk

The relief applies to specific qualifying arrangements. It does not extend to outright token sales, non-DeFi disposals, or swaps that represent genuine changes in economic exposure.

HMRC is still refining the precise boundaries of which automated market maker arrangements qualify, with further technical guidance expected before the end of 2026.

Carf Reporting Tightens Simultaneously

The NGNL relief does not arrive in isolation. HMRC introduced the Cryptoasset Reporting Framework, or CARF, obligations for UK-based crypto platforms from January 1, 2026, requiring them to collect and report structured data on UK-resident customers, including full identity details and complete transaction histories.

The CARF framework was developed at the OECD level and is already underpinning cross-border data exchanges between tax authorities.

The UK’s domestic extension means HMRC will receive standardized reporting from both UK and overseas platforms serving UK taxpayers, with the first international data exchanges scheduled for 2027.

The combination of NGNL relief and expanded CARF reporting reflects a deliberate policy architecture. The relief reduces the tax burden on compliant DeFi participation. The reporting requirement ensures that HMRC’s visibility into crypto activity increases substantially in the same year the relief is introduced.

Users who benefit from deferred capital gains on DeFi lending will find their transactions more thoroughly documented by their platforms than ever before in the market’s history.

Aave founder Stani Kulechov described the NGNL approach as a sanity restoration for compliant yield participants, predicting the clarity would lower barriers to DeFi entry for UK retail users who had previously faced compliance costs that made participation impractical.

Whether the CARF reporting requirement alters that reception will depend on how aggressively HMRC uses the new data flows in its enforcement activity from 2027 onward.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.