ndia Invites Binance, WazirX and ZebPay for Crypto Talks — Why It’s a Big Deal. Credit: Getty Images.

Share

Key Takeaways

India’s Finance Committee has invited Binance, WazirX and ZebPay for crypto policy discussions on May 20.

The talks will reportedly focus on crypto taxation, investor protection and the future of virtual digital assets (VDAs).

The meeting could signal a broader shift in how India approaches crypto regulation after years of uncertainty.

India’s crypto conversation is heating up again — and this time, some of the industry’s biggest exchanges are getting a seat at the table.

According to local reports, Parliament’s Standing Committee on Finance has invited Binance, WazirX and ZebPay to discuss crypto regulation, taxation, investor protection and the future of virtual digital assets (VDAs) in India.

That may sound procedural on the surface. But in the context of India’s complicated relationship with crypto, the meeting is attracting serious attention across the industry.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

For years, India has sent mixed signals on digital assets.

The country imposed a harsh 30% crypto tax and a 1% tax deducted at source (TDS) on transactions in 2022, triggering a sharp drop in domestic trading activity as users moved to offshore platforms.

Regulators and lawmakers also repeatedly warned about risks tied to money laundering, financial stability and speculative trading.

That contradiction — massive retail demand but limited regulatory clarity — has left the local industry stuck in a holding pattern.

Which is why this meeting is being viewed as more than just another policy discussion.

For many in the industry, it could be the clearest sign yet that India may finally be ready to move from uncertainty toward a more structured crypto framework.

Details About the Meeting

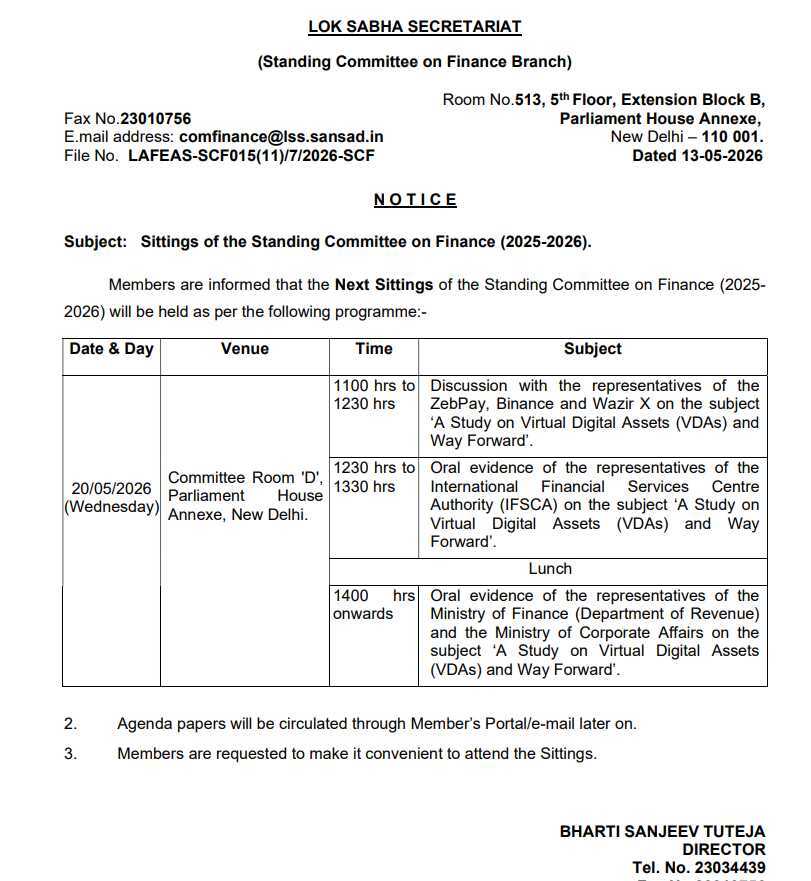

The meeting is scheduled for May 20, 2026, at Committee Room ‘D’ inside Parliament House Annex in New Delhi, according to an official notice issued by the Lok Sabha Secretariat’s Standing Committee on Finance.

Chaired by BJP MP Bhartruhari Mahtab, the discussions will begin at 11:00 a.m. and focus on what lawmakers are calling “A Study on Virtual Digital Assets (VDAs) and Way Forward.”

The first session, running from 11:00 a.m. to 12:30 p.m., will include representatives from major crypto platforms, including ZebPay, Binance, and WazirX.

Lawmakers are expected to gather industry feedback on crypto trading, taxation, regulation, and the broader digital asset ecosystem in India.

Financial Committee Invites Binance, ZebPay and WazirX—credit: Indian Government.

That will be followed by a separate session with officials from the International Financial Services Centers Authority (IFSCA) between 12:30 p.m. and 1:30 p.m.

After lunch, the committee will reconvene at 2:00 p.m. for discussions with representatives from India’s Ministry of Finance (Department of Revenue) and the Ministry of Corporate Affairs.

The structure of the meeting suggests lawmakers are trying to hear directly from both private-sector crypto firms and government regulators before deciding the next steps for India’s digital asset framework.

Today’s session also appears to expand on earlier consultations by bringing in platforms and agencies that were not part of previous discussions, signaling that policymakers may finally be moving toward a more comprehensive approach to crypto regulation.

How Earlier Crypto Talks Shaped India’s Policy

India’s finance committee has been talking to the crypto industry for years — and those conversations have quietly shaped much of the country’s current approach.

Back in November 2021, when Jayant Sinha chaired the committee, lawmakers met with exchanges and industry groups.

This includes the Blockchain and Crypto Assets Council to understand better how the sector works and the risks it poses.

At the time, many in the industry feared India could move toward an outright crypto ban.

The discussions didn’t stop there.

In December 2025, the committee once again called in domestic exchanges to discuss investor protection, AML compliance, and the growing impact of high taxes on local platforms.

Those meetings helped inform broader government thinking on enforcement, compliance and possible reforms.

These committee sessions often act as a way for lawmakers to gather direct feedback from the industry before larger decisions filter through the Finance Ministry, RBI and regulators.

India’s Crypto Industry Still Operates in a Regulatory Grey Zone

Despite its massive user base, India still lacks a comprehensive crypto law.

Exchanges currently operate through Financial Intelligence Unit (FIU-IND) registration requirements rather than a dedicated crypto licensing framework.

Meanwhile, the Reserve Bank of India continues to take a cautious stance toward digital assets, repeatedly warning about financial stability risks while prioritizing the development of its own central bank digital currency, the e-rupee.

Areas like DeFi, stablecoins and NFTs remain especially unclear.

They are taxed as virtual digital assets (VDAs), but India still lacks detailed rules on custody, investor protections, cross-border flows, and the broader market structure.

That uncertainty has created frustration across the industry.

High taxes and regulatory ambiguity pushed significant trading activity offshore, hurting local exchanges and reducing domestic liquidity.

Some founders and investors have also shifted their attention to friendlier jurisdictions such as Dubai and Singapore.

Still, the government has largely focused on tightening compliance rather than rolling out a full crypto framework.

The result is a market where crypto is legal and heavily taxed, but still sits outside the regulatory structures applied to stocks, banking or traditional finance.

From Banking Ban to Compliance Framework

India’s crypto relationship has already gone through several dramatic turns.

In 2018, the RBI effectively cut crypto businesses off from the banking system by preventing banks and financial institutions from servicing crypto-related firms. The move nearly crippled local exchanges.

That changed in March 2020, when India’s Supreme Court struck down the RBI circular, calling the restrictions disproportionate.

Trading activity quickly rebounded.

Then came another major shift in 2022, when the government formally introduced crypto taxation under the Union Budget. Virtual digital assets received their own tax category, with a flat 30% tax on profits and strict transaction reporting requirements.

By 2023, India also brought crypto exchanges and wallet providers under anti-money laundering rules through the Prevention of Money Laundering Act (PMLA).

All virtual asset service providers (VASPs) now need to register with FIU-IND, implement KYC systems and report suspicious transactions. Authorities also moved against non-compliant offshore platforms.

Today, most major Indian exchanges operate under those compliance rules.

India still has not fully regulated crypto, but it is no longer ignoring it either.

And that’s exactly why meetings like this one are attracting so much attention.

Prashant Jha is a seasoned crypto journalist based in Delhi, India, with a Bachelor’s Degree in Computer Science Engineering. Passionate about the evolving world of blockchain and cryptocurrencies, he has been a dedicated voice in the industry since 2018. Prashant’s expertise lies in regulatory reporting, where he unravels complex legal and financial developments with clarity and precision. Before joining CCN in 2024, he honed his craft at Cointelegraph, establishing himself as a trusted name in crypto journalism.

His coverage spans major industry events, including the high-profile collapses of FTX, Three Arrows Capital (3AC), and LUNA, offering readers insightful analyses of their regulatory and market implications. Prashant’s technical background enables him to bridge the gap between intricate blockchain technology and its real-world applications, making his work accessible to novices and experts.

Beyond his professional pursuits, Prashant is an avid music enthusiast, often exploring diverse genres to unwind. A sports lover, he has a particular passion for cricket and frequently engages in discussions about the game. His multifaceted interests and sharp journalistic instincts make him a valuable contributor to CCN, where he continues shaping the crypto landscape's narrative.