Visa Allows US Card Issuers to Settle in USDC — Implications for Stablecoin Payments

Share

Key Takeaways

xUSD’s stability depended on yield strategies and external asset management, rather than fully custodial, static reserves.

The disclosed $93M loss tied to an external fund manager, combined with a temporary pause on withdrawals, removed the ability for holders to redeem xUSD at $1.

Once redemptions were paused, market exit shifted entirely to secondary trading, where liquidity was thinner.

The event had system-wide effects on protocols that used xUSD or depended on it indirectly (such as deUSD), demonstrating how interdependencies in DeFi can amplify stress.

Stream Finance’s xUSD was designed to function as a yield-backed stablecoin, aiming to maintain a value close to $1 while distributing returns generated from diversified financial strategies. For a period of time, xUSD operated as intended, with users treating it as a relatively stable unit of account and collateral in various DeFi environments.

However, in early November 2025, xUSD experienced a significant depeg. Its price moved notably below $1, and market liquidity conditions accelerated the decline. This development did not occur in isolation, but it was the result of structural design characteristics combined with a particular stress event and a cautious broader market environment.

The goal of this analysis is to outline what xUSD was designed to be, what caused the depeg, and how the event fits into wider stablecoin history, without speculation.

What xUSD Was: Stream Finance’s Yield-Backed Stablecoin Model

Unlike fiat-backed stablecoins that maintain reserves in regulated custodial accounts, xUSD’s stability depended on a portfolio of yield-oriented positions. This included:

Collateral deployed into decentralized finance lending markets

Liquidity provision positions intended to earn trading fees

Portions of capital managed by external asset managers

Integration with broader DeFi platforms for borrowing, trading, and collateral use

However, the stability of this model relies on two core conditions:

Underlying assets remain sufficient and retrievable

Redemption pathways remain continuously open

If either of these conditions is disrupted, peg stability can weaken. In xUSD’s case, the second condition (redemption access) became central to the outcome.

Why xUSD Depegged: The November 2025 Loss Disclosure and Liquidity Freeze

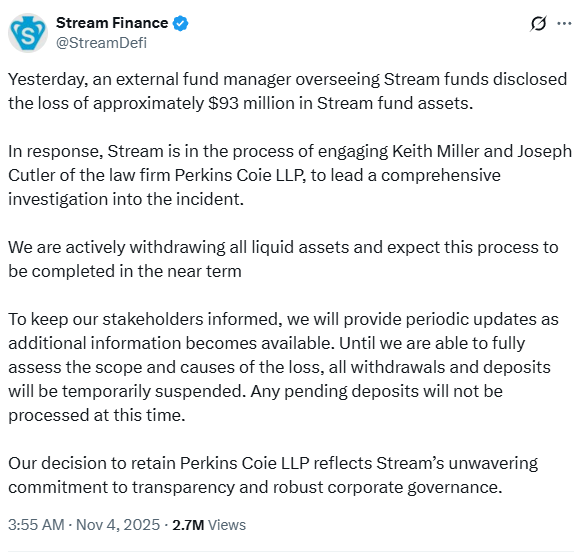

The depeg was triggered by Stream Finance publicly disclosing a significant loss (reported as approximately $93 million) connected to an external fund manager involved in overseeing a portion of the backing assets. Following this disclosure:

Stream temporarily paused withdrawals and deposits while evaluating the situation

Users attempted to exit their xUSD positions due to uncertainty

Because redemptions were paused, holders could not redeem xUSD for its underlying asset value

This meant that the only available exit mechanism was selling xUSD on secondary markets such as decentralized exchanges.

Stream Finance’s take on the xUSD depeg incident. | Source: @StreamDefi on X.

These markets typically have shallower liquidity compared to redemption-based stablecoin exits. As selling continued and buy liquidity did not scale to match it, xUSD traded progressively further below its intended $1 value.

Thus, the primary driver of the depeg was not only the disclosed loss, but the combination of loss + temporary restriction on redemptions, which removed the mechanism used to enforce peg stability.

Structural Factors That Made the xUSD Peg Vulnerable

Several structural characteristics influenced how the depeg played out:

Structural Factor

Effect on Outcome

Exposure to external asset management

A real-world loss directly impacted perceived backing strength

Portfolios designed for yield rather than pure collateral retention

The backing could fluctuate with market conditions

Redemption pause during a confidence-sensitive moment

Peg could no longer be defended via arbitrage

It is important to note that no stablecoin can maintain a peg if redemption is suspended at the same moment confidence declines. Once the arbitrage mechanism is interrupted, market price becomes solely dependent on available liquidity and sentiment, not on underlying value.

Impact on deUSD and sdeUSD

The depeg of xUSD also affected deUSD and sdeUSD, synthetic assets associated with Elixir. These assets were structurally linked to xUSD through shared liquidity and collateral flows. Because part of deUSD’s stability assumptions relied on xUSD maintaining its peg, the decline in xUSD’s price led to immediate pressure on deUSD.

Community discussions have referenced estimates about the scale of exposure between the systems, but what is clear is that the connection between the two stable assets created a transmission channel, where stress in xUSD translated into stress in deUSD. This illustrates how interlinked collateral models can amplify market shocks in DeFi.

X user’s warning on xUSD. | Source: @DU09BTC on X

Understanding Redemptions: How Stablecoins Hold Their Peg

To understand why xUSD’s price moved below $1, it’s important to understand what “redemption” means in stablecoins.

What is Redemption?

Redemption is the process where a stablecoin holder can exchange the token back for the value that backs it, usually at or very close to $1 per token.

In practical terms:

Action

Result

You return 1 unit of a stablecoin

You receive $1 worth of backing assets

This mechanism is what keeps a stablecoin stable.

If the token price falls below $1 on the market, arbitrage traders can buy it at a discount and redeem it for $1, pushing the price back up.

This only works if redemption is available.

Why Redemption Matters for Peg Stability

A stablecoin peg is held up by two forces:

Confidence in the assets backing the token.

The ability to convert the token into those assets at any time

When both are working, the price stays near $1 because:

If price drops → arbitrage pushes it back up

If price rises → issuing new tokens brings it back down

This is the core self-correcting system behind most pegged assets.

What Happens When Redemptions Are Paused

If redemption access is temporarily restricted or paused, even for review or security reasons, then:

Holders cannot exchange tokens at $1

Arbitrage cannot function

The market price is determined only by buyers and sellers on exchanges

Without a redemption mechanism, market price reflects liquidity conditions and sentiment, not the intended peg.

Ripple Effects Across the Ecosystem: xUSD, deUSD and Connected Markets

Some DeFi platforms had integrated xUSD into collateral systems or derivative asset models. Because of this, the decline in xUSD’s price affected the stability assumptions of these related assets. The most visible outcome was the impact on deUSD, a synthetic stablecoin whose structure was influenced by xUSD’s market conditions.

This resulted in:

Price pressure on deUSD

Liquidity providers and borrowers reassessing exposure

Protocols reviewing collateral risk parameters

This event highlighted a broader pattern in DeFi:

When assets are interconnected, the stress does not stay contained, it propagates through dependency links.

Comparing the xUSD Depeg to Prior Stablecoin Events

The xUSD depeg shares recognizable characteristics with earlier stablecoin stress periods:

Past Event

Shared Mechanism

Notable Difference

Terra/UST (2022)

Peg depended on continued confidence and reinvested yield

Terra was algorithmic, while xUSD was backed by real but affected assets

USDC depeg during SVB exposure (2023)

News-driven confidence shock

USDC regained its peg via immediate redemption assurances

DAI liquidity stress episodes (2023–2024)

Peg stability affected by broader market liquidity

Increased sensitivity to disclosures involving losses or asset uncertainty

Because of this, when the Stream Finance disclosure occurred, market participants acted more defensively and more quickly than they might have in a more optimistic environment.

In short:

The market was already cautious.

The disclosure acted as a catalyst.

The redemption pause removed the stabilization mechanism.

Where Things Stand Now for xUSD and What to Watch Next

Stream Finance has stated that it will be engaging attorneys Keith Miller and Joseph Cutler of Perkins Coie LLP to conduct a comprehensive investigation into the circumstances surrounding the loss.

It has also has stated that it is withdrawing all liquid assets, and expects this process to conclude in the near term. All deposits and withdrawals have been temporarily suspended while the firm assesses the situation. Pending deposits will not be processed during this period.

Stream Finance has indicated that periodic updates will be provided as more information becomes available.

The future trajectory depends primarily on:

Clarity on the recoverability of affected assets

Updated transparency on collateral composition and valuations

Whether structured redemption frameworks will be established

Adjustments by DeFi platforms with prior xUSD or deUSD exposure

Until more information becomes available, the situation remains in a review and stabilization phase.

There is no evidence that xUSD was intentionally unbacked. The issue was the impairment of part of its backing portfolio + loss of redemption access, which prevented the peg from correcting through arbitrage.

Why did the peg fall so sharply instead of gradually?

Because when redemptions are paused, stablecoins become valued purely by market supply and demand, not by their intended backing value. In thin liquidity conditions, even moderate selling can lead to sharp price declines.

Did the depeg occur because of market manipulation or coordinated selling?

There is no confirmed indication of coordinated selling. The decline aligns with a standard DeFi run dynamic: users exit when confidence decreases and redemption pathways are unavailable.

Could xUSD recover its peg in the future?

A recovery is possible only if:

backing asset values are clarified or partially recovered,

redemption pathways reopen in some form,

and counterpart protocols adjust collateral structures accordingly.

Without those steps, the peg is unlikely to re-align with $1.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy