Nearly 88% of ASTER tokens are concentrated in six wallets.

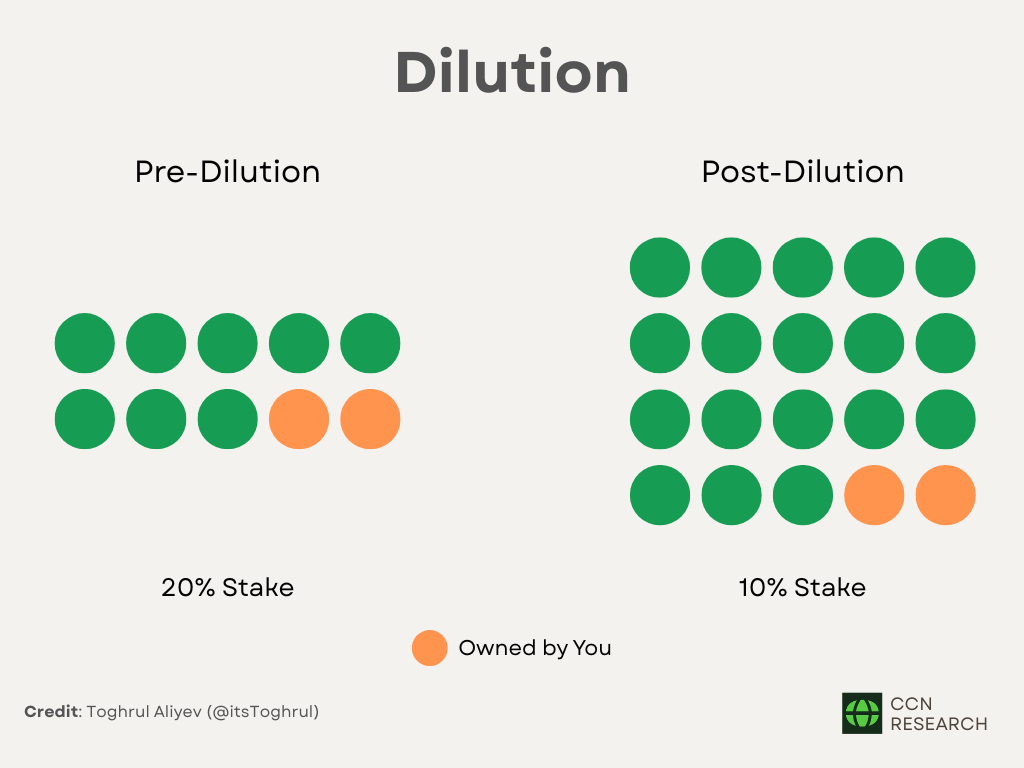

With the circulating supply set to double by 2027, Aster faces growing dilution pressure that could erode the value of early holders.

One wallet’s contract was deployed by a Binance-managed address but is labeled “Aster Treasury” on-chain.

Aster’s CEO, Leonard, argues that the wallets aren’t under team control and are mostly locked or held by exchanges.

Certik’s review found no backdoors or minting privileges in Aster’s smart contract.

Last week, I examined Aster’s sharp rise in trading activity, where daily volume climbed from $1.15 billion to $85.55 billion in 12 days.

The analysis focused on whether that growth reflected genuine trading demand or artificial volume.

To continue this month’s CCN Reports theme on perpetual futures and perpetual decentralized exchanges, I turn to the foundation of Aster’s token economy: its ownership. Six wallets on BNB Chain hold nearly the entire ASTER supply.

In this issue, I investigate who controls these wallets, how they operate, and why such extreme concentration may not necessarily spell disaster.

ASTER Tokenomics

Before addressing wallet concentration, it’s necessary to understand the project’s token distribution.

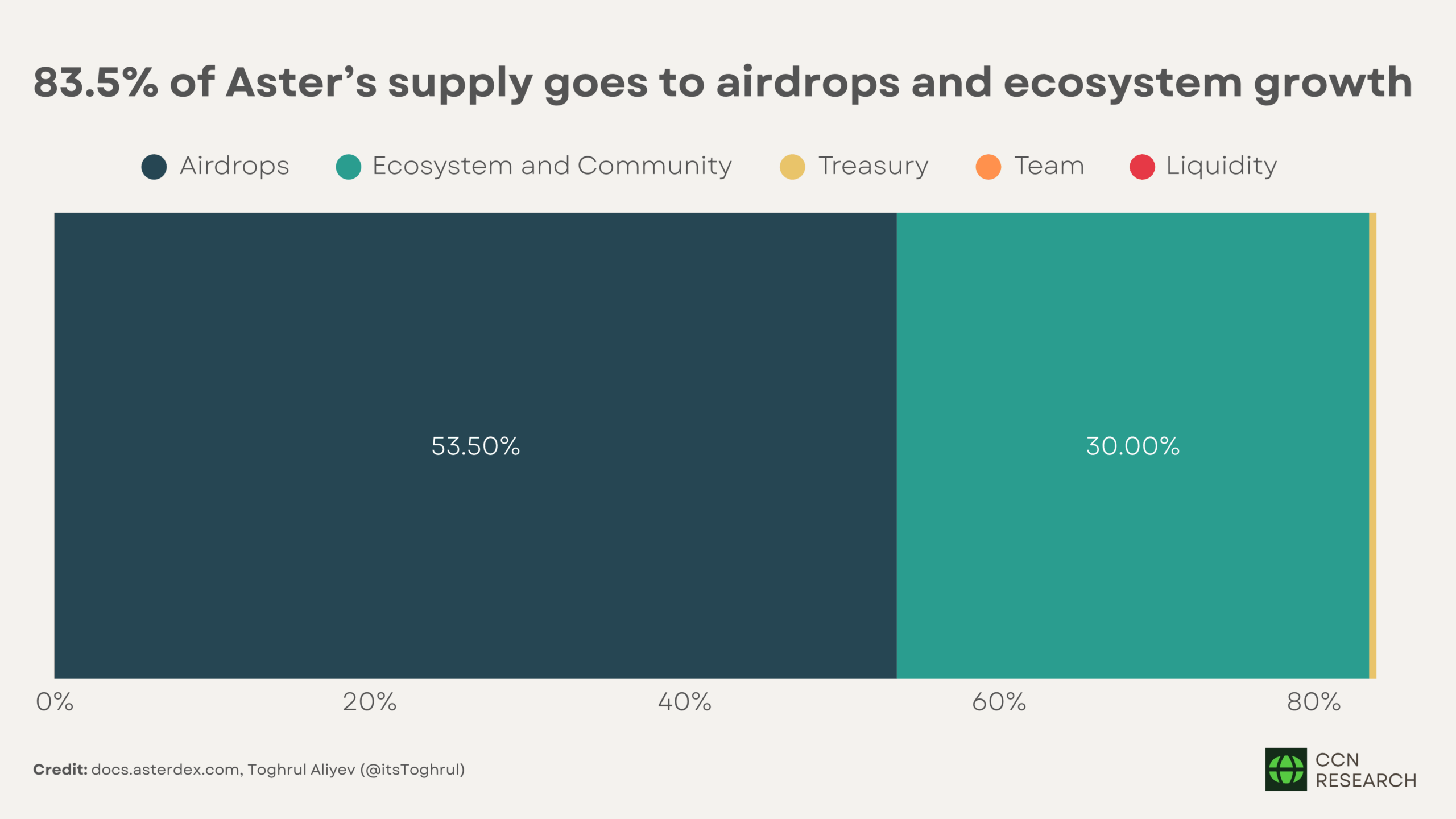

Aster operates on a total supply of 8 billion ASTER tokens. The allocation model distributes 53.5% of tokens, or 4.28 billion, through airdrops.

Another 30% supports ecosystem and community development. The remaining supply includes 7% for treasury operations, 5% for the team under a cliff vesting schedule, and 4.5% for liquidity and exchange listings (Figure 1).

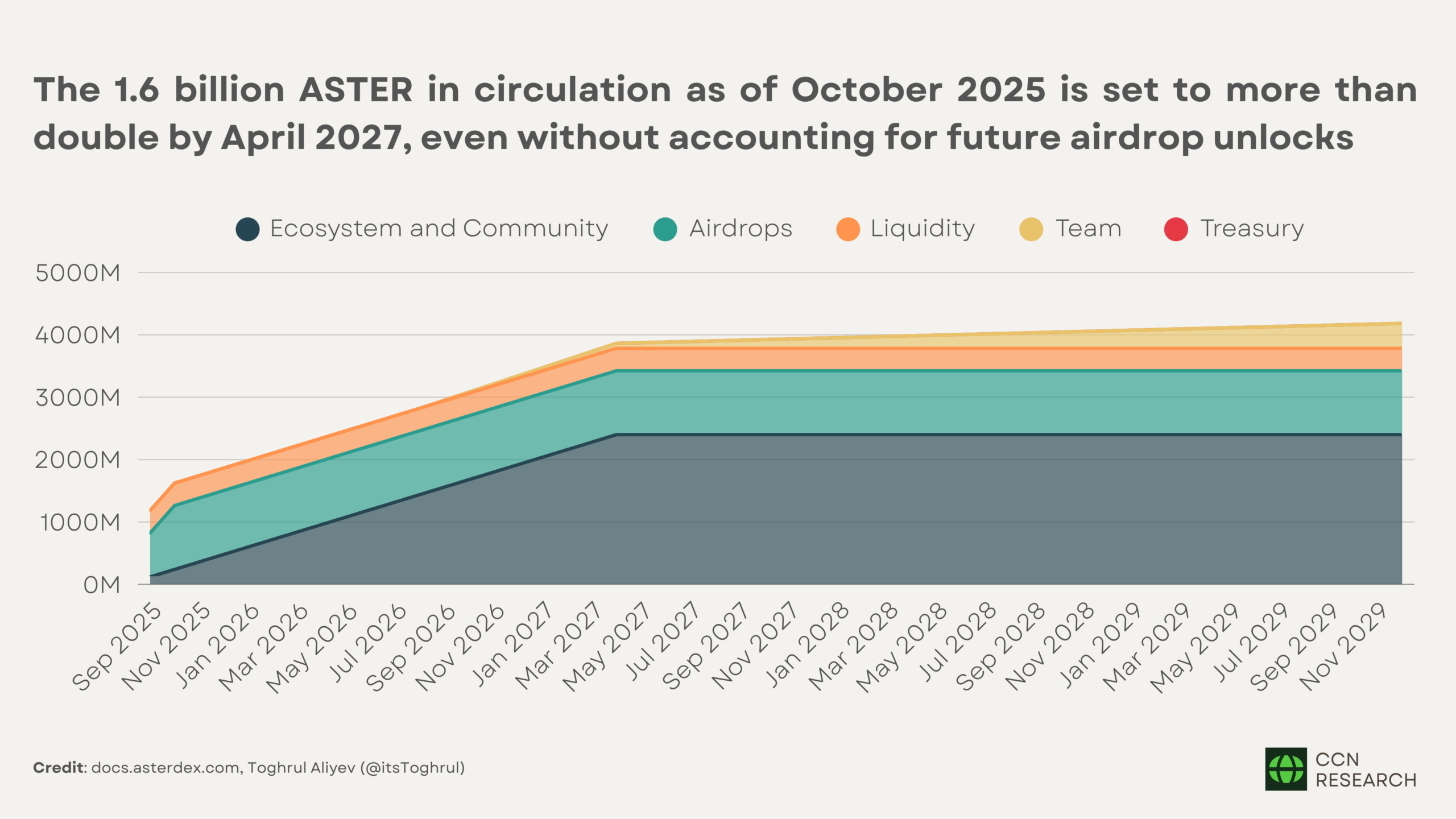

The current circulating supply stands at approximately 1.66 billion tokens, or around 21% of the total supply, following the Token Generation Event (TGE) on September 17, 2025.

Of the airdrop allocation, 8.8%, equivalent to roughly 704 million tokens, was unlocked immediately for early participants of Aster’s Spectra campaign. The rest follows an 80-month release schedule, with gradual distributions subject to adjustments in governance.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Each allocation class uses a structured vesting plan.

Team tokens feature a one-year cliff followed by 40 months of linear release.

Ecosystem tokens, excluding the APX swap pool, vest over a 20-month period.

The treasury’s 7% allocation remains locked until a governance vote approves any movement.

The key concern here is dilution. A significant portion of the supply remains locked. By April 2027, just about two years from now, the circulating supply is expected to more than double, even without accounting for future airdrops (Figure 2).

When factoring in upcoming airdrop seasons, the total supply in circulation could potentially triple.

On the other hand, a gradual unlock can also encourage participation if distributed effectively. Airdrops and ecosystem incentives are meant to expand user ownership and increase trading activity, both of which support long-term liquidity and network stability.

Whether dilution becomes a problem depends on execution, meaning how tokens are transferred from locked wallets to active circulation and whether user demand grows quickly enough to absorb the new supply.

The discussion on dilution naturally leads to a deeper question: where are the tokens stored before they unlock?

Inside the Six Wallets Controlling Aster’s Supply on BNB Chain

As of Oct 6, 2025, six primary wallets hold roughly 88% of the total ASTER supply. At first glance, that degree of concentration raises concerns about control, liquidity risk, and possible insider coordination.

But on closer inspection, nothing appears inconsistent with what the Aster team outlined.

The first two addresses align closely with the airdrop and ecosystem allocations, though both now hold smaller balances following initial distributions. Their withdrawal activity aligns with the timing and scale of the initial airdrop and ecosystem reward rounds.

The airdrop program distributed 704 million ASTER during its first season, while 832 million ASTER from the ecosystem pool was redirected to a new address, now the third-largest wallet, which holds 733,222,840 ASTER. This wallet acts as a treasury-linked liquidity reserve, facilitating constant inflows and outflows that support trading on Aster’s DEX.

Unlike the airdrop and community wallets, which are well-documented in Aster’s official token allocation and tokenomics literature, the treasury-linked liquidity reserve wallet was not publicly mentioned anywhere in the project’s initial documentation.

Perhaps the most concerning part is that the smart contract associated with this wallet was created on June 11, 2024, by “Binance Hot Wallet 11.” A “hot wallet” refers to an exchange’s actively managed wallet used for daily operations, deposits, and withdrawals, controlled by Binance. Yet, on-chain, the wallet is labeled “Aster Treasury.”

This is particularly unusual because a separate wallet already holds exactly 7% of the total supply allocated for treasury operations, as outlined in Aster’s tokenomics.

The question, then, is why the Aster Treasury wallet, absent from any public disclosure, received liquidity from the ecosystem and community allocations rather than the designated liquidity wallet, and why its creation was linked to a Binance-managed address instead of an Aster-deployed one.

I searched through all official company channels, including documentation, announcements, and social media, but found no reference to this wallet or its purpose.

Additionally, at the time of writing, the Aster team has not responded to my request for clarification. As soon as they do, I will update this section accordingly.

After accounting for the airdrop, ecosystem, and unexplained treasury-linked wallet, the remaining allocations appear consistent with Aster’s published token distribution: 7% for treasury, 5% for team allocation, and 2.4788% for liquidity. The liquidity figure is slightly lower than the stated 4.5% because part of the supply was distributed across several exchanges, including Gate, Bybit, and Binance.

What Aster’s CEO Says About the Six Wallets and the 88% Supply Claim

Leonard, Aster’s CEO, addressed the “six-wallet” issue directly during a live interview. He stated that reports claiming that the majority of the supply sits under team control are “misleading,” emphasizing that these wallets do not represent internal reserves:

“We don’t control all of those wallets. Around 80% of the supply is locked on-chain, and most of those addresses can be verified publicly. Many belong to exchange or staking contracts where users hold or trade ASTER.”

Leonard also mentioned that YZI Labs, Aster’s only private investor, holds equity in the company but does not directly control or own ASTER tokens, aside from a minor portion linked to the 5% team allocation.

Their investment was not a token sale but an equity partnership, meaning their influence is corporate rather than on-chain.

Smart Contract Review and Security

The team can make its statements, but as the saying goes in crypto, don’t trust, verify.

The most accessible way to do so is through CertiK, which has already scanned the Aster smart contract for vulnerabilities. The results show no technical risks. The only concern flagged is token concentration, an issue I addressed earlier in relation to the Binance-linked wallet.

Attribute

Category

Description / Value

Major holder ratio

Volatile Market, Centralization

90.57% (excluding holdings by exchanges and locked addresses)

Buy tax

Market

Buy tax: 0%

Can modify balance

Centralization

Token balance cannot be modified by privileged roles

Can modify tax

Centralization

Token tax cannot be modified by privileged roles

Can regain ownership

Centralization

Backdoor to regain ownership not found

Can self-destruct

Rugpull

Self-destruct function not found

Cannot buy

Market

Buy token restriction not detected

Cannot sell all

Market

Sell all token restriction not detected

Has blacklist

Centralization

Token blacklist not found

Has external calls

General

External calls not found

Has hidden owner

Centralization

Hidden owner not found

Has whitelist

Centralization

Token whitelist not found

Is anti-whale

Market

Anti-whale mechanisms not found

Is anti-whale modifiable

Market

Anti-whale mechanisms of the token cannot be modified

Is honeypot

Rugpull

Honeypot risk not found

Is mintable

Centralization

Mintable function not found

Is proxy contract

Centralization

Token is not a proxy contract

Is transfer cooldown

Centralization

Transfer cooldown mechanism not found

Is transfer pausable

Centralization

Transfer pausable mechanism not found

Not open source

Transparency

Token is open source

Ownership not renounced

Centralization

Owner privilege has been renounced

Sell tax

Market

Sell tax: 0%

A review of the contract’s structure, deployment, and on-chain activity indicates that Aster’s smart contract behaves as expected.

Token minting and transfer functions adhere to standard BEP-20 logic, and there are no backdoor mechanisms that would enable the team to mint, modify balances, or reassign ownership.

The contract cannot self-destruct, includes no blacklist or whitelist features, and imposes no buy, sell, or transfer restrictions.

Both the buy and sell tax parameters are set to 0%, and ownership privileges have been fully renounced, meaning no single entity retains administrative control.

Conclusion

Crypto moves faster than facts. A few large wallets, a sudden surge in trading, or a fragment of data can quickly be misinterpreted as claims of manipulation or control. In Aster’s case, most of those claims lose weight once scrutinized. The on-chain data aligns with the project’s tokenomics, the contract shows no technical risks, and the wallet behavior reflects an organized distribution rather than hidden control. The concentration is visible, but so is the transparency behind it.

The real issue is the lack of verification. Too many opinions are formed without research. People often conclude from screenshots instead of on-chain records, and entire narratives develop from assumptions that no one checks. That culture of reaction weakens trust and hinders the industry’s progress.

At CCN, neither the company nor I holds any affiliation with Aster or any other project mentioned in this report. Our work is entirely independent and based on verifiable data, rather than marketing or partnerships. The goal is to bring clarity to the industry through fact-checked, research-driven reporting that helps readers distinguish between evidence and opinion.

Crypto does not need more speculation. It requires investigation and accountability. Every report we publish follows that principle, to examine what others overlook, verify what others assume, and help the space mature through transparency rather than hype.

Toghrul Aliyev is the Head of Research who began his journey in crypto in 2021. It all started with a Reddit post that went viral, leading to a writing position while he was still in medical school. As he learned more about crypto, he became deeply interested in it and decided to focus entirely on this field after completing his medical degree and becoming a doctor.

Toghrul specializes in thorough research, always aiming to find details others might miss. He also has a strong understanding of stocks, real-world asset tokenization, and related areas. He is skilled in Python and SQL, which he uses to improve his crypto analysis through data analytics and data science.

When he’s not working, Toghrul enjoys sports, hiking, reading philosophy, such as Seneca's works, and playing story-driven video games.