Since that filing, Bitcoin has dropped roughly 20%, slipping under $60,000 on June 5 for the first time since September 2024.

Two events, one timeline, an obvious villain. The problem is that the timeline is the only thing connecting them, and correlation, this clean usually hides a messier truth.

It sounds plausible, especially because the offering routes up to 30% of shares straight to retail through Robinhood, Fidelity, and Schwab, roughly three times the slice a typical IPO reserves for individuals.

If you check the dates, SpaceX does not price until June 11 and does not begin trading on the Nasdaq until June 12, under the ticker SPCX. The bulk of Bitcoin’s decline happened before a single share changed hands.

Investors cannot fund a purchase that has not opened, which means the mechanical “sell Bitcoin, buy SpaceX” trade could not have driven the early June plunge. Onchain and stablecoin flow data reinforce the point, showing no abnormal exodus of crypto capital cashing out to chase the offering during the crash window.

There is even an irony that the rotation theory ignores. SpaceX itself holds Bitcoin, sitting on roughly $789 million in unrealized gains as of late May. The company being blamed for draining Bitcoin is one of its larger corporate holders.

What Actually Drove the Bitcoin Crash

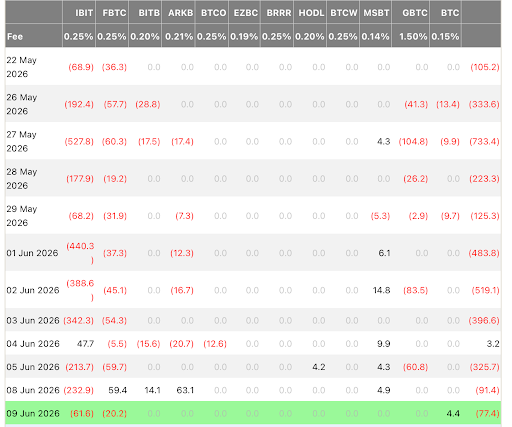

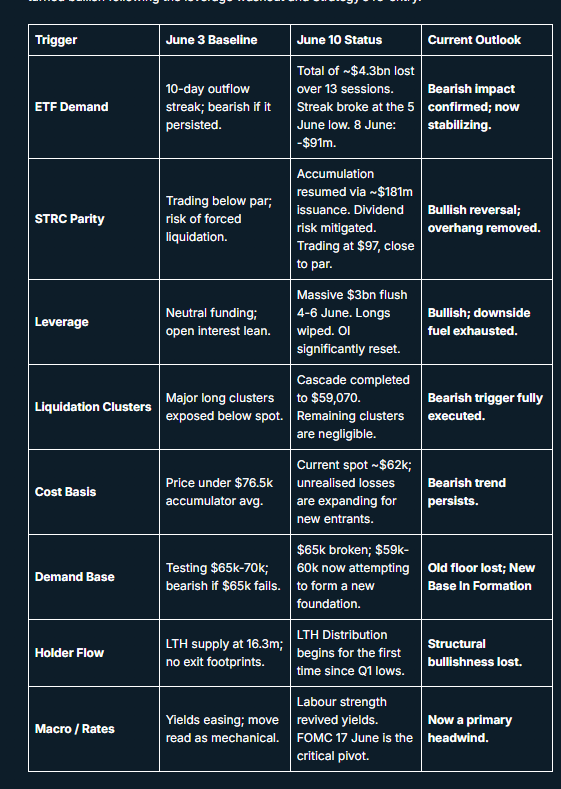

The real engine was mechanical, running on leverage and fund flows. United States spot Bitcoin ETFs bled for 13 consecutive sessions through June 3, the longest outflow streak on record, shedding around $4.4 billion. Those redemptions are not sentiment.

The primary catalyst for the downturn was spot ETF selling pressure. | Source: Bitfinex.

When investors pull money, the issuer sells the underlying Bitcoin on the spot market to raise cash, applying steady, automated downward pressure regardless of what anyone believes about rockets.

On top of that came a leverage flush. Between June 2 and June 5, crypto derivatives liquidations reached roughly $1.6 billion to $1.8 billion, with one stretch force-closing about $394 million in a single hour.

Close to 272,000 traders were wiped out, and the long-short split was lopsided, with the overwhelming majority holding bullish positions that were caught leaning the wrong way.

It was the largest deleveraging event since the prior October’s crash. That is not capital migrating to an IPO, but it points to overcrowded long positioning collapsing under its own weight.

Sentiment had already been softened a day earlier. On June 1, Strategy, the largest corporate Bitcoin holder, announced its first Bitcoin sale since 2022. The amount was tiny relative to its stack, but it dented the “never sell” conviction that retail had built its thesis around, and it gave nervous longs a reason to hit the exit.

Macro Storm That Hit the Same Week

Bitcoin did not fall in a vacuum. It fell alongside a broad risk-off cascade that had nothing to do with crypto fundamentals. A hotter-than-expected United States jobs report landed that week, reviving fears that the Federal Reserve’s next move could be a rate hike rather than a cut, sending Treasury yields higher and crushing long-duration risk assets.

The Nasdaq dropped 4.2% on June 5, its worst single-day decline of 2026, with chip leaders like Nvidia down around 6% as the AI trade wobbled amid bubble fears.

Geopolitics piled on. Iran launched missiles at Israel that week, the first such attack since the April ceasefire, pushing Brent crude back toward $95 a barrel and stoking the exact inflation worry that keeps the Fed hawkish.

Bitcoin, which trades as a high-beta risk asset far more than as digital gold, did what every speculative position did in that environment. It got sold.

Kernel of Truth in the Rotation Thesis

None of this means the SpaceX story is pure fiction.

There is a legitimate, slower version of it worth taking seriously. For years, crypto held a near monopoly on high-upside, lottery-style speculation. That monopoly is ending. Mega IPOs like SpaceX and the anticipated OpenAI and Anthropic listing, alongside the AI equity boom, now offer the same dopamine to the same risk-hungry investors.

Over time, that competition can pull speculative capital away from crypto, helping explain why Bitcoin struggled even as equities remained near record highs.

But that is a gradual shift, not something that causes a 20% selloff in a matter of days. That distinction matters. Competition for investor attention is real, but the idea that the SpaceX IPO directly triggered a leverage-fueled Bitcoin crash does not hold up when the timeline is examined.

Why the Distinction Matters

Misdiagnosing a crash leads to the wrong conclusions about what comes next. If you believe SpaceX broke Bitcoin, you might expect prices to keep bleeding until IPO mania cools, a vague and untradeable thesis.

If you understand that the move was a leverage washout amplified by record ETF outflows and a hawkish macro shock, you get sharper signposts.

Liquidation cascades exhaust themselves, funding rates have already flipped negative, and forced selling tends to overshoot. The path from here depends on ETF flows stabilizing and the Fed picture clarifying, not on how many retail traders buy SPCX on June 12.

While SpaceX’s IPO dominated headlines, Bitcoin’s decline appears to have been driven by market mechanics rather than capital rotating into the offering. ETF redemptions, leverage unwinds, and macro headwinds played a far larger role.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.