Donald Trump's new crypto filings have sparked a flurry of criticism — will it impact the CLARITY Act? | Source: CCN.

Share

Key Takeaways

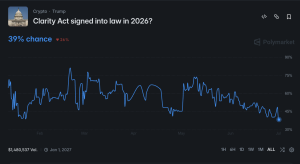

Traders now assign just a 39% chance that the CLARITY Act will become law in 2026.

President Donald Trump’s latest financial filing revealed more than $1.4 billion in crypto-related assets and income.

The filings sparked criticism from former White House lawyer Ty Cobb.

Critics warn disclosures could complicate the legislation.

Odds of the US CLARITY Act becoming law this year have fallen below 40% on crypto prediction platform Polymarket.

The move comes after President Donald Trump’s latest financial disclosure revealed more than $1.4 billion in crypto-related assets and income.

Trump’s disclosure drew criticism from Ty Cobb, a former White House lawyer during his first administration, who described the President’s financial filings as “the greatest onslaught of corruption in the history of mankind.”

Meanwhile, others have criticized that Trump’s personal financial interests could stall the legislation.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Trump’s latest ethics filing showed substantial crypto-related assets and income across several ventures, including two Bitcoin cold wallets valued at more than $50 million each.

According to Forbes, the wallets appear to represent direct Bitcoin holdings, which, when combined with Trump’s indirect exposure through Trump Media & Technology Group’s Bitcoin treasury, give the president more than $500 million exposure to BTC.

Trump’s financial disclosure report featured over 900 pages. | Source: X: @dethective

The disclosure also detailed more than $1.1 billion of other crypto-related income, including approximately:

$635.1 million from the TRUMP memecoin

$236.3 million from World Liberty Financial token sales

$196.9 million from the sale of ownership interests in the USD1 stablecoin venture

$65.6 million from the partial sale of Trump’s stake in World Liberty Financial

$6 million from Melania Trump’s NFT business

$1.82 million in Ethereum staking rewards

The filings come after Trump has repeatedly pledged to make the US the “crypto capital of the world” and backed legislation designed to provide greater regulatory certainty for digital assets.

Former White House Lawyer: ‘Greatest Onslaught of Corruption’

Speaking on CNN, former Trump White House lawyer Ty Cobb criticized the President’s crypto activities.

When asked if he believed they were legal, Cobb replied: “I don’t believe so.

“Certainly, I don’t think it was contemplated by the founders when they created the Emoluments Clause,” Cobb said.

Referring to Trump, Cobb added:

“This is somebody who every day is devoted to the accumulation of wealth and power.”

He described the recent events as “seeing the greatest onslaught of corruption in the history of mankind in the last 18 months.”

Cobb noted how average Americans should be outraged by a President openly creating rules that line his own pockets.

The White House has previously defended Trump’s financial disclosures and ethics compliance.

Timing Could Complicate CLARITY Act

The disclosures were released as the Senate continues to stall on passing the CLARITY Act.

Many in the industry believe the renewed attention on Trump’s crypto interests could make passage more politically difficult.

Tony Edward, founder of Thinking Crypto Podcast, noted that the timing of Trump’s disclosures was “interesting.”

“This info could further strengthen the Dems who are using ethics to roadblock the Clarity Act,” Edward added.

The timing of these disclosures is interesting. This info could further strenghten the Dems who are using ethics to roadblock the Clarity Act. The transparency is good but the timing maybe bad for the Clarity Act which is about to hit the Senate floor in July. https://t.co/OngOK9SfNO

— Tony Edward (Thinking Crypto Podcast) (@thinkingcrypto) July 1, 2026

He noted that while the “transparency is good,” the timing will be bad for the legislation.

SkyBridge Capital founder Anthony Scaramucci also said that Trump’s crypto exposure “will be cited as one of the main reasons if Clarity doesn’t pass.”

Other social media users also suggested Trump’s financial interests could become a focal point during the Senate debate.

CLARITY Act Polymarket Odds Fall Below 40%

Following the disclosures, Polymarket traders are currently assigning a 39% probability that the CLARITY Act will be signed into law before the end of 2026.

The contract has declined steadily over recent weeks after trading above 60% for much of the Spring.

Polymarket CLARITY Act odds are falling | Source: Polymarket

At the beginning of June, the market gave over a 60% chance it would be signed.

Just one month later, it has dropped over 20%, with many lawmakers concerned it could be pushed back into August and beyond.

Galaxy Research Also Lowers Odds of Passage

Galaxy Research has also become more cautious about the CLARITY Act’s prospects.

Last week, the firm lowered its estimate of the legislation becoming law in 2026 to 50% from 60% earlier this month.

In a policy update, Galaxy Head of Research Alex Thorn said the downgrade reflected mounting concerns over the Senate’s legislative calendar.

“The absence of news is itself the news,” Thorn wrote.

He said lawmakers have yet to release a unified version reconciling the Senate Banking and Agriculture committees’ proposals or schedule a floor vote.

Thorn added that the legislation still faces several procedural hurdles, including:

Publication of a merged bill

A motion to proceed

Senate debate,amendments

Final approval

Subsequent House action

All of this is needed before it can reach President Donald Trump’s desk.

According to Thorn, Senate Majority Leader John Thune would need to commit to floor consideration by early July for the measure to have a realistic chance of clearing before lawmakers leave for the August recess.

Without that timetable, Thorn warned the legislation could slip into September.

This would be another challenge, as it is closer to the midterm elections, which could make floor time to discuss the legislation harder to secure.

CLARITY Act Push Back Continues

The CLARITY Act has continued to see criticism from Senate Democrats led by Elizabeth Warren.

In May, the bill could weaken investor protections through a “tokenization loophole.”

Warren said the legislation would allow companies to issue tokenized versions of traditional financial products on blockchain networks while avoiding existing securities regulations.

The Massachusetts Democrat warned the proposal “fails to address one of the biggest concerns that retirees face.”

🚨 WATCH: Chairman @SenatorTimScott leads the Senate Banking Committee in a historic markup of the CLARITY Act, legislation to establish clear rules of the road for digital assets. https://t.co/wlHj2jcAEF

— U.S. Senate Banking Committee GOP (@BankingGOP) May 14, 2026

She described the potential regulatory gap as “a catastrophic problem” and introduced an amendment requiring investment advisers to implement additional procedures before recommending crypto-related investments to clients.

“My amendment would require investment advisors and other entities in the financial system to develop and implement processes to protect investors from the heightened risk posed by crypto,” Warren said.

Republican Senator Cynthia Lummis opposed the proposal, arguing it would unfairly single out digital assets.

“This amendment would single out digital assets for a special presumption of noncompliance and create unnecessary litigation risk,” Lummis said.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Kurt Robson is a London-based reporter at CCN, specialising in the fast-moving worlds of crypto and emerging technology. He began his career covering local news in Cornwall after graduating from Falmouth University with First Class Honours in Journalism. There, he cut his teeth on everything from council meetings to missing swans.

He quickly rose through the ranks to become a frontline journalist at several of the UK’s leading national newspapers. Over the years, he has interviewed musicians and celebrities, reported from courtrooms and crime scenes, and secured multiple front-page exclusives.

Following the upheaval of the COVID-19 pandemic, Kurt shifted his focus to technology journalism—just ahead of the AI boom. With a natural curiosity and a trained eye for emerging trends, he has found a new rhythm in reporting on innovation.

At CCN, Kurt's work focuses on the cutting edge of crypto, blockchain, AI, and the evolving digital world. Drawing on his background in people-first reporting and his deep interest in disruptive tech, Kurt delivers stories that are insightful, entertaining, and human-centric.