Bitcoin Price Returns Turn Negative When Investors Miss the Best 10 Days: Analyst

Share

Key Takeaways

A Bitcoin analyst argued that missing just the 10 best trading days each year turned a median annual return of +90% into -25% from 2020–2025.

Bitcoin’s strongest rallies often occur around unpredictable catalysts, making consistent exposure more valuable than frequent trading.

Avoiding the worst days would also boost returns, but the study highlights the high cost of being out of the market during major upside moves.

Missing just 10 trading days a year erases the entirety of Bitcoin’s long-run return premium, turning a median annual gain of 90% into a median loss of 25%, according to a data analysis published this week by market analyst David Eng covering the five-year period from 2020 through 2025.

The finding underscores a structural feature of Bitcoin that distinguishes it from most traditional asset classes: annual performance overwhelmingly concentrates in a small number of sessions that are, by definition, impossible to predict in advance.

Across the six years studied, the median buy-and-hold annual return came to a positive 90%. Removing the 10 best trading days from each calendar year reduced that figure to negative 25%, a swing of 115 percentage points. Two of the six years that were positive on a buy-and-hold basis flipped to negative once the best 10 sessions were excluded.

The damage was particularly acute in 2022, when Bitcoin fell 85% for investors who missed its best 10 days, compared to a decline of 64% for those who held throughout. The 2024 year produced a buy-and-hold return of positive 121%, driven in significant part by the January approval of US spot Bitcoin ETFs, a catalyst whose timing and magnitude were not knowable in advance. Investors who reduced exposure ahead of the approval captured only a fraction of that year’s return.

The data covers daily BTC-USD closing prices, with missed days treated as zero-return sessions rather than negative ones, meaning the actual impact of exiting positions during drawdowns would likely produce worse outcomes than the analysis captures. “You do not get paid for prediction,” Eng wrote. “You get paid for being there.”

Concentration of Returns Is Not Unique to Bitcoin

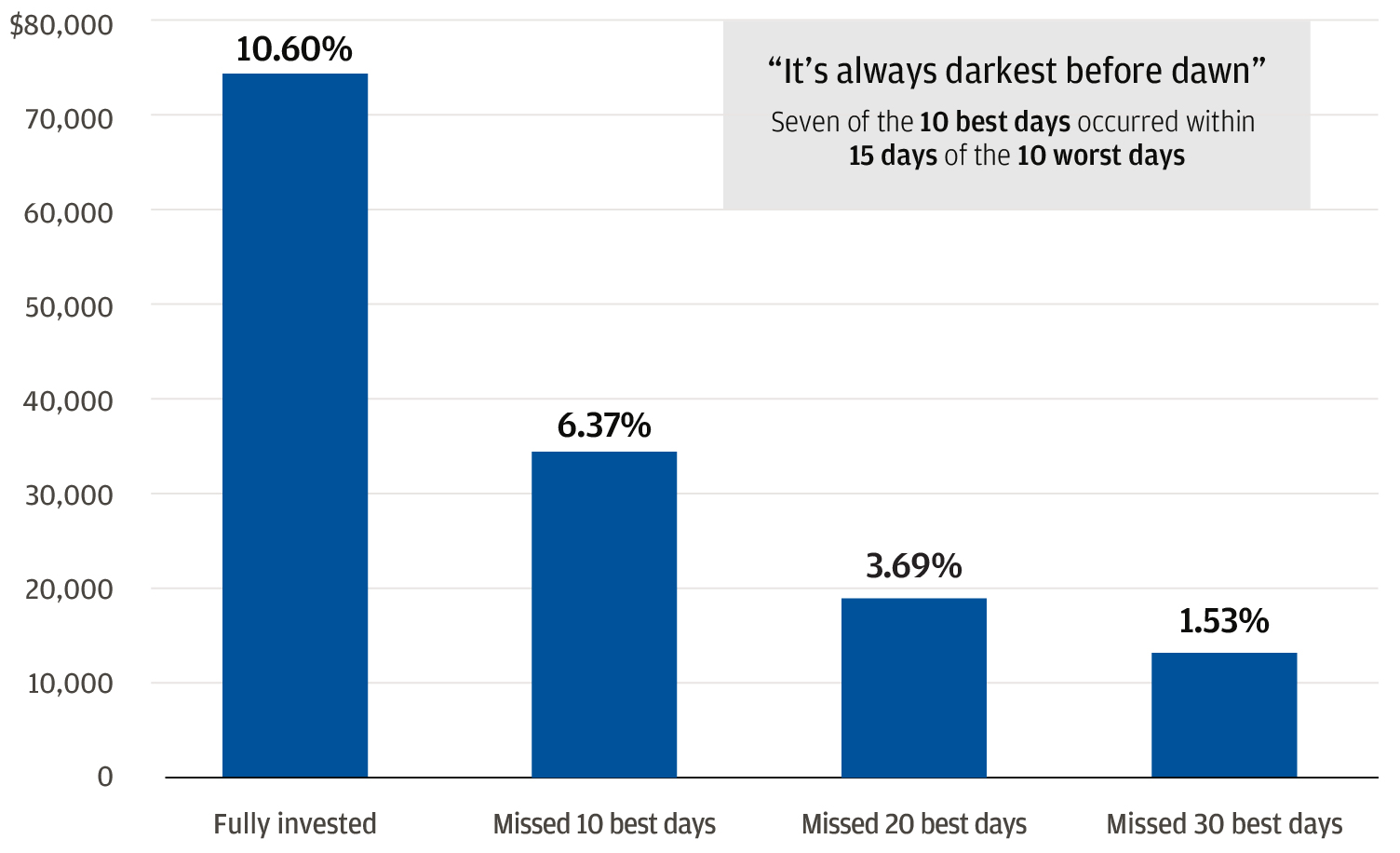

The pattern has documented precedents in traditional markets. Research on US equities has shown comparable dynamics for decades, with a frequently cited JPMorgan Asset Management study finding that missing the 10 best days in the S&P 500 over 20 years roughly halved terminal returns.

It’s about time in the market, not timing the market. | Source: J.P. Morgan

Bitcoin’s version of the same dynamic is more extreme because its best days generate larger absolute percentage moves than equity indices, and because those moves tend to cluster around catalysts that become apparent only in retrospect.

Counterarguments and a Changing Return Profile

The case against a pure buy-and-hold reading of the data is substantive. The return concentration applies in both directions: a small number of the worst sessions account for a disproportionate share of annual drawdowns, and avoiding those days would significantly improve outcomes. The 2022 data illustrates the problem from both ends simultaneously.

A second challenge concerns Bitcoin’s evolving return profile as institutional ownership deepens. The 2025 calendar year produced a negative 6% return on a buy-and-hold basis, the first post-halving year in Bitcoin’s history to close in the red.

If the distribution of returns is becoming less skewed as spot ETF flows dampen volatility, the cost of missing the best 10 days may compress over time, even as the directional lesson about exit risk remains intact.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.