The gold increased to a new fresh record and investors wonder if it can grow further or it's time to sell. Here's what boosted ounce's price. l Credit: David McNew/Getty Images

Share

Key Takeaways

Gold surged to a record high above $2,266 per ounce, continuing its upward trend from March.

The expectation that the Federal Reserve will cut interest rates later this year makes gold an attractive investment.

Rising tensions in the Middle East and Ukraine are prompting central banks to diversify their reserves, increasing demand for gold.

Following a historic surge in March, the upward trajectory of gold prices persists, soaring to unprecedented heights on Monday, April 1, 2024. The yellow metal breached the $2,266 per ounce threshold, hitting a new record.

The rising interest in gold, driven by three key factors, reinforces its status as a stable and attractive investment option.

Market Bets On Fed’s Rate Cuts

Last Friday’s data release unveiled that the Federal Reserve’s key inflation gauge, the PCE index, surged by 2.8% on an annual basis in February, aligning with market projections. Despite this uptick, the Fed stood resolute during its recent March meeting, maintaining interest rates at 5.25%-5.5%, while adhering to its forecast of three rate cuts this year.

However, juxtaposed with the prevailing price index and labor market indicators, market sentiment leans towards anticipating rate cuts by the Federal Reserve in either May or June.

Historically, gold prices have mirrored an inverse correlation with interest rates. As borrowing costs decline, the appeal of gold amplifies when compared to fixed-income assets like bonds, which offer diminished returns in a low-interest-rate environment.

The PCE index seemed to have minimal effect on traders’ anticipation of a June interest rate reduction. This despite Fed chair, Jerome Powell’s cautionary note that they were unlikely to plummet to the levels witnessed after the 2008 global financial crisis.

Banks Diversify Portfolios Due To Geopolitical Risks

Further propelling the surge in gold prices are the escalating tensions gripping regions like the Middle East and Ukraine. In recent hours, Russian President Vladimir Putin’s authorization of an additional enlistment of 147,000 soldiers underscores the intensifying situation.

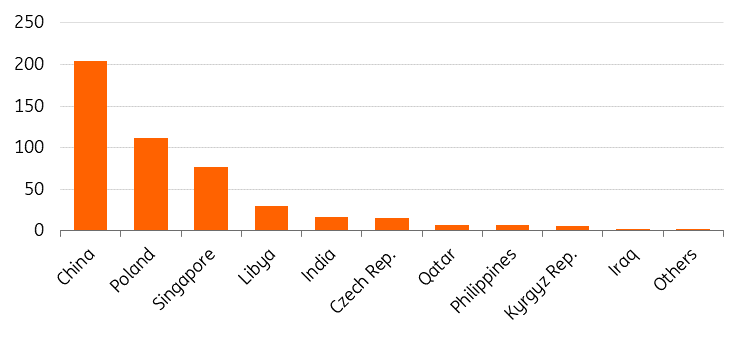

Central banks demand for gold. l Source: ING

Meanwhile, concerning the conflict in Israel, American media outlets have raised alarms about a scheduled US-Israeli summit in Rafah. Amid these geopolitical flashpoints, the rally in gold finds additional impetus from heightened purchases by global central banks. These seek to fortify reserve portfolios against geopolitical uncertainties and domestic inflationary pressures.

The escalation of tensions persisted as an airstrike in Lebanon on Sunday heightened anxieties, with Israel reporting the elimination of a Hezbollah missile unit commander. Israel and the Iran-backed group have been engaged in near-daily cross-border exchanges for several months.

Central banks tonnes purchases. l Source: ING

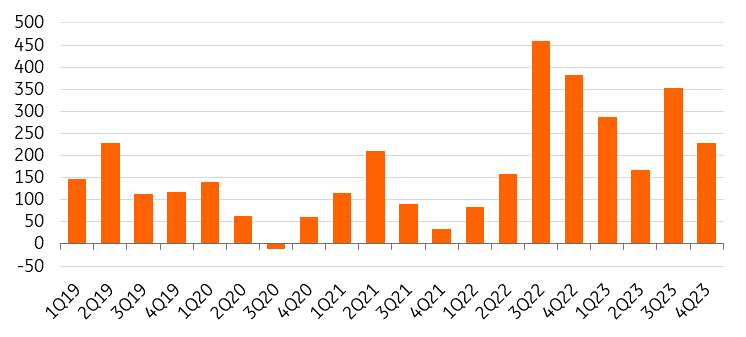

Central bank continued its robust trajectory in the fourth quarter. They witnessed an additional 229 tonnes incorporated into global official gold reserves, as evidenced by data from the World Gold Council. This surge propelled annual net demand to 1,037 tonnes – narrowly missing the 2022 record of 1,082 tonnes – driven by heightened geopolitical uncertainties prompting central banks to bolster their allocation towards secure assets.

Furthermore, the robust appetite for gold among central banks is spurred by apprehensions surrounding potential Russian-style sanctions targeting their foreign assets. This follows the US and Europe’s decision to freeze Russian assets.

Chinese Demand Also Boosts Gold’s Price

The appetite for gold is burgeoning in China, marked by pronounced demand observed in recent quarters. The People’s Bank of China (PBoC) has bolstered its reserves by acquiring substantial volumes of bullion over the past 16 months.

Moreover, industry experts highlight a growing trend among young Chinese individuals gravitating toward gold purchases. Even private investors are turning their attention to the yellow metal. This is drawn by the tumultuous state of the real estate sector, which poses significant strains on the Chinese economy despite vigorous stimulus efforts by the government in Beijing.

The People’s Bank of China emerged as the foremost gold acquirer. It accumulated a total increase of 225 tonnes in its gold reserves over the year. In 2023, the National Bank of Poland claimed the second spot as the largest buyer, significantly enhancing its gold holdings.

Between April and November, the central bank procured 130 tonnes of gold. It escalated its gold reserves by 57% to reach 359 tonnes.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.