Using XRP to pay a home may soon be possible. Read how. | Credit: Steve Pfost/Newsday RM via Getty Images

Share

Key Takeaways

A new Senate Bill would require Fannie Mae and Freddie Mac to include unconverted cryptocurrencies in mortgage eligibility assessments.

While the bill doesn’t name specific tokens, XRP is a strong candidate if large-cap, regulated assets are prioritized.

Upcoming FHFA draft guidelines, congressional debate, and final eligibility criteria will determine whether XRP is included.

Only crypto’s volatility, cybersecurity concerns, and unresolved regulatory questions could limit or delay XRP’s inclusion.

The U.S. housing market might be on the verge of an unprecedented collision with the crypto world — one that could reshape how Americans qualify for mortgages and potentially spark new demand for digital assets like XRP.

Whether decades-old underwriting rules can adapt to a generation whose wealth is increasingly stored on blockchains rather than in bank accounts is at stake.

A New Bill Could Bring Crypto Into the US Housing Market

A new bill in Washington could allow cryptocurrencies to be part of your mortgage application — a change that could ripple through the entire digital asset market, including coins like XRP.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

U.S. Senator Cynthia Lummis (R-WY) has introduced the 21st Century Mortgage Act, which would require Fannie Mae and Freddie Mac, the government-sponsored enterprises (GSEs) that back about 70% of U.S. home loans, to include unconverted crypto assets in their risk assessments for single-family mortgages. Users could qualify for a home loan without selling their crypto first.

21st Century Mortgage Act of 2025 Explained

The 21st Century Mortgage Act of 2025 would require government-sponsored enterprises (like Fannie Mae and Freddie Mac) to consider certain digital assets when assessing the risk of a mortgage loan.

The 21st Century Mortgage Act brings mortgage lending into the Digital Age and makes homeownership more accessible for young Americans. pic.twitter.com/CNqkvcWO4N

Digital assets are digital representations of value recorded on a secure, cryptographic ledger (like cryptocurrencies). It excludes non-fungible items like collectibles or assets representing control over non-digital property.

To count, these assets must remain in a qualified custodial arrangement with a regulated U.S. custodian or in a multi-party custody setup governed by enforceable U.S. law.

Lenders can assess mortgage risk by including borrowers’ eligible digital assets in their reserves without requiring conversion into U.S. dollars.

Lenders must apply risk adjustments for market volatility, liquidity, and the proportion of reserves held as digital assets. Banks must review and update these adjustments periodically.

Before changing the way they evaluate these assets, the agencies must get board approval and submit the methods to the Federal Housing Finance Agency for review.

In short, the bill aims to modernize mortgage lending by letting regulated cryptocurrency holdings count toward a borrower’s financial strength, while also requiring safeguards to manage risk

From Cashing Out to Counting In: Recognizing Crypto in Mortgage Reserves

If you own crypto and want it to count toward your mortgage reserves, you must liquidate it into U.S. dollars. This creates two problems:

Market timing risk: Users might have to sell during a price dip, locking in a loss.

By allowing crypto to remain in its original form, the bill respects the “intrinsic value” of digital assets and acknowledges their growing role in modern wealth-building. This could be especially significant for younger Americans — 67% of crypto holders are under 45.

Supporters say acknowledging crypto in mortgage underwriting reflects the rising role of digital wealth in today’s economy.

The Mortgage Bankers Association has expressed support in principle, noting that the proposal aligns with changing patterns of asset ownership and borrower behavior. Many see it as a natural progression in financial innovation.

Echoing that view, Duke University finance professor Campbell Harvey argues that “FHFA is pushing Fannie and Freddie to recognize the world of payments is changing and that the dollar is not the only game in town.”

He pointed out that today’s borrowers frequently spread their wealth across both traditional and digital holdings, and excluding crypto from consideration may already be outdated.

How US Housing Finance Could Embrace Crypto as Mortgage Reserves

If the bill passes, Fannie Mae and Freddie Mac would treat specific cryptocurrencies as eligible mortgage reserve assets.

The FHFA (Federal Housing Finance Agency) has already issued a directive to start developing proposals for how to integrate crypto into underwriting, with the requirement that assets be:

This policy shift would mainstream crypto in the world’s largest and most regulated financial markets: U.S. housing finance.

How a US Housing Bill Could Quietly Boost XRP’s Market Position

Even though the bill doesn’t mention XRP directly, the policy logic could benefit it in several ways:

Liquidity recognition:XRP is known for its fast settlement times and relatively low transaction costs. If regulators and GSEs prioritize assets with high liquidity and straightforward utility, XRP could receive the same consideration of Bitcoin and Ethereum.

U.S. market legitimacy: Being recognized in the mortgage system would be a huge credibility boost. Institutional acceptance often attracts new investment flows, which historically can lift prices.

Utility narrative: XRP’s core value proposition is efficient cross-border payments. Tying it to real-world financial infrastructure like home loans could strengthen its “real use case” narrative, which markets reward over time.

Demand shock potential: If even a small fraction of U.S. homebuyers began holding XRP to boost their mortgage applications, it could create new, sticky demand for the token.

5 Ways Mortgage Acceptance Could Reshape XRP’s Price Dynamics

If mortgage underwriters begin accepting XRP (alongside other compliant digital assets), the potential price impact could unfold through several reinforcing channels:

Increased demand: Prospective homebuyers could strategically accumulate XRP months or years before applying for a mortgage, knowing it would strengthen their reserve position. This new, purpose-driven buying behavior could create steady inflows into the asset, particularly among younger, tech-savvy demographics already more likely to hold crypto.

Lower sell pressure: Under current rules, borrowers must liquidate crypto into USD to have it counted toward mortgage eligibility, which can create abrupt selling pressure — especially during down markets. If XRP can be held in its native form, borrowers can keep their positions intact, reducing forced liquidations and helping maintain upward price momentum during periods of market stress.

Institutional flows: Mortgage-backed securities (MBS) investors and other institutional participants in the housing finance ecosystem could gain indirect exposure to crypto reserves through the loans they back. This may prompt deeper due diligence on digital assets, potentially leading to formal research coverage, risk models, and even targeted allocation to XRP in diversified portfolios.

Broader market legitimacy: Inclusion in mortgage underwriting would signal to the market that XRP has achieved a level of regulatory and institutional acceptance once considered unlikely. This recognition can be self-reinforcing, as legitimacy often attracts additional capital from retail and professional investors.

Wealth diversification incentives: As more people recognize XRP’s eligibility in a high-value, long-term financial product like a home mortgage, it could become part of a broader wealth diversification strategy — alongside stocks, bonds, and cash. This embedded utility tends to increase asset stickiness and reduce short-term speculative churn.

XRP Price to Benefit From Lummis Bill?

XRP’s long-term chart is extremely bullish.

The XRP price has consistently created higher lows since March 2020.

The price also created lower highs during the same period, forming a symmetrical triangle pattern.

The XRP rally became parabolic once the price broke out from the triangle in December 2024.

The most likely wave count suggests the breakout is part of wave C in an A-B-C structure (black).

If this is the case, the main target for the high is $5.76, giving waves A and C the same length.

The sub-wave count (green) predicts another high until the rally ends.

There is a growing bearish divergence in the RSI and MACD (orange), which often occurs between the wave three and wave five high, as is the case for XRP.

The XRP price will likely reach a new all-time high this year before beginning a lengthy correction.

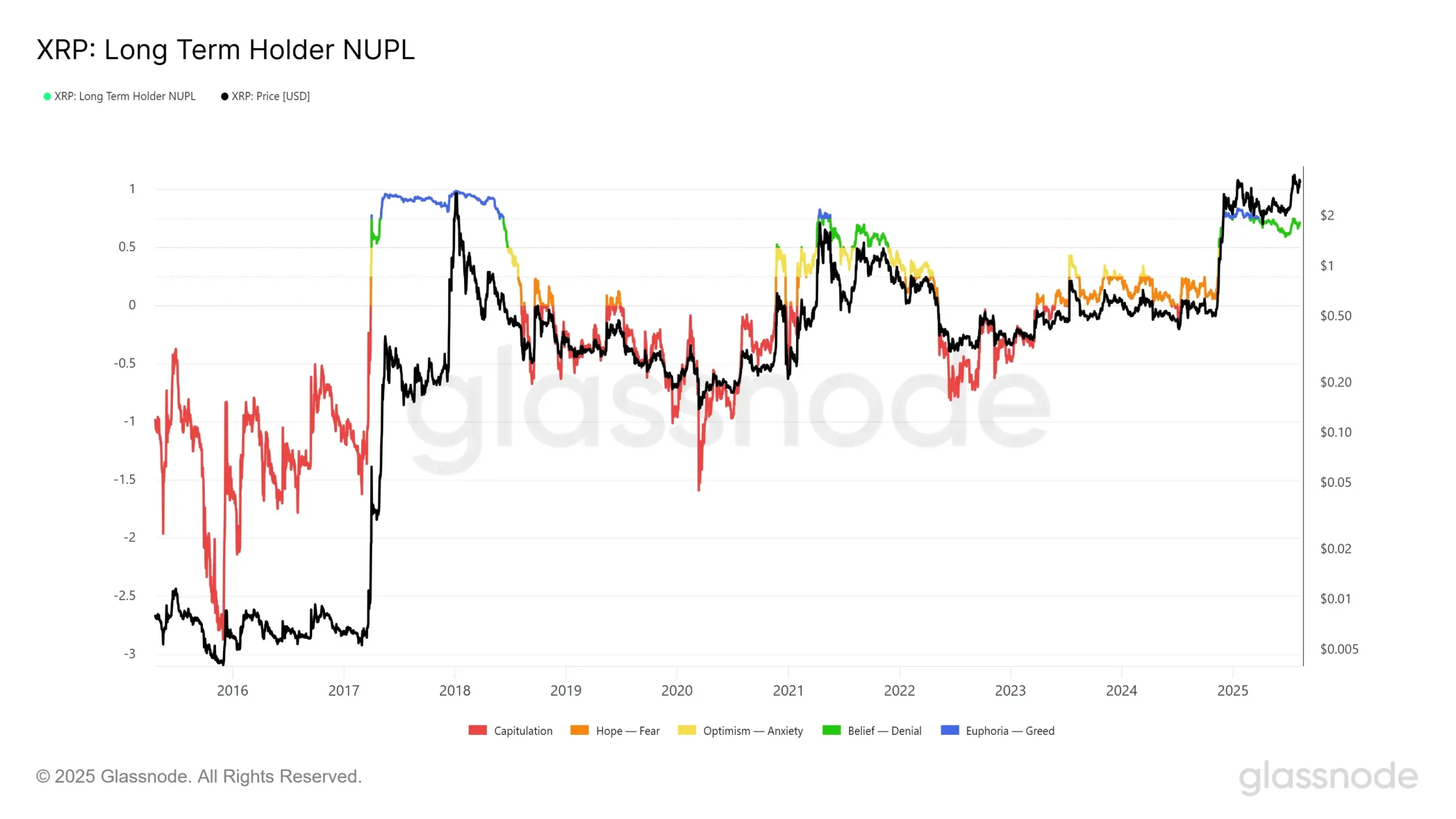

This prediction fits with the on-chain long-term holder NUPL indicator, which assesses the behaviour of long-term investors.Historically, XRP cycle tops have always occurred above 0.75, marking the cycle’s “Euphoria” and “Greed” parts.

Today, the LTH-NUPL shows a value of 0.73. The proposed price breakout will likely cause the LTH-NUPL indicator to move into this territory.

Hence, the wave count, technical indicator, and on-chain indicators all indicate the possibility of a cycle top near $5.75.

Regulatory and Risk Hurdles on the Road to Mortgage-Backed XRP

Of course, the idea has critics. Lawmakers like Senator Jeff Merkley (D-OR) warned about volatility — bitcoin is over three times more volatile than gold- and crypto markets have suffered hacks, scams, and liquidity crunches.

Mortgage analysts also fear a replay of 2008’s risky lending patterns if underwriting standards loosen without adequate safeguards.

For XRP, there’s the added factor of regulatory clarity. Even if the SEC vs. Ripple case is resolved chiefly, GSEs could initially limit eligibility to assets with the least perceived legal uncertainty.

Ron Haynie of the Independent Community Bankers of America stressed that a clear regulatory framework is essential before integrating crypto into the mortgage system.

He warned against implementing policy changes without first gaining a thorough understanding — and regulatory oversight — of how these assets perform throughout different economic cycles.

What to Watch as Mortgage Crypto Rules Take Shape

Before XRP can play any role in U.S. mortgage underwriting, several regulatory and operational decisions need to fall into place. The fine print will determine not just if XRP qualifies, but how valuable it will be as a reserve asset in practice.

From draft rules to political negotiations, these policy levers could make the difference between a token price catalyst and a missed opportunity.

FHFA guidelines: Watch for draft rules from Fannie Mae and Freddie Mac that specify which cryptocurrencies qualify as eligible reserve assets, how they will be valued, and what documentation borrowers must provide. Early drafts will show whether the team considers XRP from the outset or adds it later.

Risk haircuts: If XRP is accepted, regulators may apply a “haircut” so that only a percentage of its market value counts toward reserves, to offset volatility risk. The size of that haircut will be critical — a 50% haircut versus a 10% haircut could dramatically alter how attractive XRP is for mortgage planning.

Exchange standards: To qualify, XRP must be held on a U.S.-regulated, compliant exchange with strong custody protections. This requirement could influence where and how holders store their XRP, potentially driving liquidity toward specific platforms.

Congressional debate: The bill could face opposition from lawmakers worried about housing market stability, but the Trump administration’s pro-crypto stance and FHFA Director Pulte’s backing give it political momentum. Negotiations may result in compromise provisions, such as limiting eligibility to large-cap assets or phasing in adoption over time.

Conclusion

So, if passed and implemented inclusively, the 21st Century Mortgage Act could inject digital assets — possibly including XRP — into the core of U.S. housing finance.

For XRP holders, that could mean more legitimacy, demand, and a stronger case for long-term value — all while giving homebuyers a new way to leverage their crypto wealth without selling it.

In a market where utility and adoption often drive price, a seat at the mortgage table could be one of the most meaningful developments for XRP in years.

FAQs

What is the 21st Century Mortgage Act?

The 21st Century Mortgage Act is a bill introduced by U.S. Senator Cynthia Lummis (R-WY) requiring Fannie Mae and Freddie Mac to consider specific cryptocurrencies as eligible reserve assets in mortgage underwriting. Borrowers could count unconverted crypto toward their mortgage reserves, rather than being forced to sell it into U.S. dollars.

Could XRP qualify under this legislation?

The bill doesn’t name specific cryptocurrencies, but if Fannie and Freddie’s eventual guidelines prioritize liquidity, regulated custody, and strong utility, XRP could qualify alongside Bitcoin and Ethereum. Its fast settlement, low fees, and established use in cross-border payments make it a candidate for inclusion — assuming it’s held on a U.S.-regulated exchange and meets risk standards.

Why would this be bullish for XRP’s price?

If mortgage underwriters accept XRP, it could encourage homebuyers to accumulate XRP ahead of applications, boosting demand; reduce forced selling, as borrowers wouldn’t need to liquidate to qualify; increase institutional exposure through mortgage-backed securities, raising legitimacy and potential capital inflows; and create long-term “sticky” demand as XRP becomes part of diversified wealth strategies.

What risks or limitations could hold XRP back?

Volatility remains a key concern — crypto assets can swing sharply in value. Regulators may apply “haircuts” that count only part of an asset’s value toward reserves, or limit eligibility to a small number of large-cap coins. XRP’s regulatory history, including the SEC lawsuit against Ripple, could also delay or restrict its acceptance in federally backed loans until full clarity.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Valdrin Tahiri is a cryptocurrency analyst and reporter at CCN, specializing in technical analysis with a focus on Elliott Wave theory, on-chain metrics, and fundamental research. He brings over seven years of experience in the crypto space as both a trader and writer.

He discovered cryptocurrencies in 2017 while earning his MSc in Financial Markets at the Barcelona School of Economics, which sparked a deep interest in blockchain and market dynamics. Since then, he’s contributed to top crypto outlets like BeInCrypto and CoinGape.

Valdrin also served as Community Manager of BeInCrypto’s Telegram group for three years, helping grow it into one of the largest crypto communities worldwide. His expertise in market structure and price patterns allows him to break down complex trends into clear, actionable insights.

He’s published thousands of articles covering altcoins, Bitcoin cycles, and macro trends.

Easy

Easy