Bank of England Stablecoin Regulation: Consultation Begins, Final Rules Coming in 2026| Credit: Hameem Sarwar /CCN

Share

Key Takeaways

The United Kingdom moves forward with a full stablecoin regime as the Bank of England begins its consultation ahead of final rules in 2026.

The framework introduces strict expectations for reserves, capital, liquidity, and consumer protection as systemic stablecoins grow in the UK payment system.

Industry reactions show a divided market, with some firms calling the rules too restrictive while others welcome stronger clarity.

The consultation connects directly to the digital pound plan and sets the foundation for a system where public and private digital money can operate safely.

The United Kingdom advanced its stablecoin roadmap after the Bank of England (BoE) opened a consultation on November 10, 2025, on rules for systemic sterling stablecoins in coordination with the Financial Conduct Authority (FCA) and HM Treasury (HMT).

The consultation marks a turning point in the country’s approach to digital money and signals that full rulemaking will arrive in 2026.

This article explains how the UK plans to guide stablecoin growth with clear rules, coordinated oversight, strong prudential standards, and a system that protects financial stability while supporting secure digital payment innovation.

Why a Multi-Money Ecosystem Could Redefine the UK’s Payment System

Policymakers aim to establish a framework that supports innovation in payments while safeguarding the UK’s financial system. Regulators want clear responsibilities for issuers, stronger safeguards, and a structure that supports secure innovation across the UK payment system.

Deputy Governor Sarah Breeden said in her speech published on October 15, 2025 that the UK is moving toward “a multi-money mixed ecosystem”, adding that central-bank money, bank deposits and regulated stablecoins should coexist and remain fully interchangeable to give users more choice and foster competition, “all freely and frictionlessly exchangeable at par.”

Broader use across retail and business payments increases demand for rules that define responsibilities, backing requirements, and safeguards.

Stablecoins connected to everyday transactions can influence liquidity flows, confidence in the financial system, and competition between traditional banks and new payment providers.

Scope of UK Stablecoin Regulation

A clear framework defines how the UK separates payment-focused stablecoins from other digital assets. Regulators seek structures that align with real-world risks without hindering innovation.

In the UK, a coordinated model gives each regulator a clear role.

Bank of England: Leads on prudential standards, reserve quality, liquidity rules, and system resilience.

HM Treasury: Defines the legal perimeter and decides when a stablecoin enters the systemic regime.

Payment Systems Regulator: Supports competition and fair access across payment chains.

Together, these bodies create a structure that supports stablecoin innovation while aiming to protect financial stability. As a result, there are different boundaries for tokens.

Which Stablecoins Fall Inside the Rules

The consultation establishes the following elements for consideration:

Payment focus: Only stablecoins used as payment instruments fall within the framework. Examples include a sterling-backed token used for online shopping, payroll, or merchant payments inside the UK.

Different behaviors: Tokens used for trading or decentralized finance (DeFi) activity fall outside this category. Examples include crypto-collateralized stablecoins used for margin trading on exchanges or for liquidity pools.

Authorities focus on these risks to identify which payment-focused stablecoins could grow large enough to affect the wider system. This assessment leads to the next category.

Systemic Sterling Stablecoins

Systemic status means the stablecoin has grown important enough that any disruption could affect payments or financial stability across the wider UK system. Sterling-backed stablecoins in this category face a stronger regulatory regime.

Usage threshold: Regulators classify a stablecoin as systemic when its size, reach, and market impact create risks for the wider UK financial system.

Treasury role: His Majesty’s Treasury reviews these criteria and makes the final decision on systemic designation.

Prudential expectations: A systemic designation triggers prudential standards that issuers must follow to support financial stability.

Non-systemic oversight: Stablecoins that do not meet these thresholds remain under the FCA’s regime, which applies to smaller or exchange-focused tokens.

Full rules are expected to be finalized in 2026. It is essential to note that all stablecoins are currently utilized in the UK, including US Dollar-pegged coins such as USDC and Tether USD, which are non-systemic within the UK’s sterling payment system context.

The most likely candidate to become systemic would be a new sterling-denominated stablecoin that gains significant market adoption for retail or corporate payments across the UK, at a scale comparable to major payment systems.

The regulatory framework sets the foundation for stronger requirements that apply once a stablecoin reaches systemic scale. As a result, regulators are shifting their focus to specific proposals.

Backing Rules for Systemic Stablecoins: What Issuers Must Hold

A major part of the consultation focuses on how systemic stablecoin issuers must support token value.

The Bank of England sets clear rules for reserves that hold stable value, provide immediate liquidity, and protect users during periods of market stress. These expectations build on the Bank of England’s earlier work on digital money, including its 2023 paper on systemic payment systems and its broader analysis of new forms of digital money

Reserve Composition for Systemic Stablecoins

The consultation proposes a two-part reserve model. Issuers must hold unremunerated deposits, which are funds kept at the central bank without earning interest, at the Bank of England and short-term sterling-denominated UK government debt securities.

This structure aims to give stablecoins a predictable value and protects convertibility. The Bank of England explains this approach across its publications and official communications.

The standard requirements include:

40% in unremunerated deposits at the Bank of England: Issuers keep a large share of reserves at the central bank for maximum safety and instant liquidity.

60% in short-term UK government debt: Issuers hold the rest in government securities that keep stable value and can be sold quickly when users redeem their tokens.

Some issuers may enter the market as systemic from launch, while others may grow into systemic status from the FCA’s non-systemic regime. The consultation introduces a step-up regime to support early operations without weakening safeguards.

New issuers can hold up to 95% of reserves in short-term UK government debt during the first phase. They must shift toward the standard 60% limit as their stablecoin’s value increases. This approach follows principles highlighted in the FCA’s discussion paper on regulating cryptoassets and HM Treasury’s policy work on stablecoin regulation.

.Additionally, it is worth noting that the rules prohibit issuers from paying interest on systemic stablecoins. Regulators want these tokens to operate as payment instruments, not savings products.

Key Details From the Stablecoin Consultation and Limits

The consultation adds new requirements that build on earlier proposals and sets the following:

Temporary Holding Limits

The consultation introduces temporary limits to manage the risk of rapid shifts from bank deposits into stablecoins.

Individuals: Up to £20,000 per systemic stablecoin

Businesses: Up to £10,000,000 per systemic stablecoin

Exemptions: Large firms can request higher limits when they show operational need and strong risk controls

The Bank of England presents these holding limits as one part of a broader transition plan. Regulators want a stable environment while they assess how payment-focused stablecoins behave at scale. Once they understand adoption patterns, they turn to the next phase of the framework.

Capital Requirements for Systemic Issuers

The consultation outlines capital standards that aim to keep systemic issuers strong during periods of stress. These rules follow international expectations for firms that support payment systems.

Cover business risk: Issuers must keep capital that protects operations during unexpected events.

Largest plausible loss event: Capital must cover the cost of recovering from the most severe loss scenario regulators consider realistic.

Six months of operating expenses: Issuers must hold enough capital to continue operating during a prolonged disruption.

These standards ensure issuers can continue meeting obligations even when markets face pressure.

Liquidity Support From the Central Bank

The consultation explores a potential liquidity backstop for systemic issuers. The Bank of England considers using a lending facility that would only apply in limited cases.

Only solvent and viable issuers qualify.

Funds support short-term liquidity needs during stress.

The tool mirrors support available for other regulated payment institutions.

This measure aims to maintain convertibility during market turbulence without turning stablecoins into deposit-like products.

Safeguarding Through a Statutory Trust

The consultation strengthens legal protections for users. Issuers must hold backing assets in a statutory trust when they serve UK customers.

Users gain a clear legal claim to the reserves.

Trust protection applies if an issuer fails.

The structure prevents issuers from using reserves for unrelated business activities.

This requirement gives users confidence that reserves remain secure and accessible.

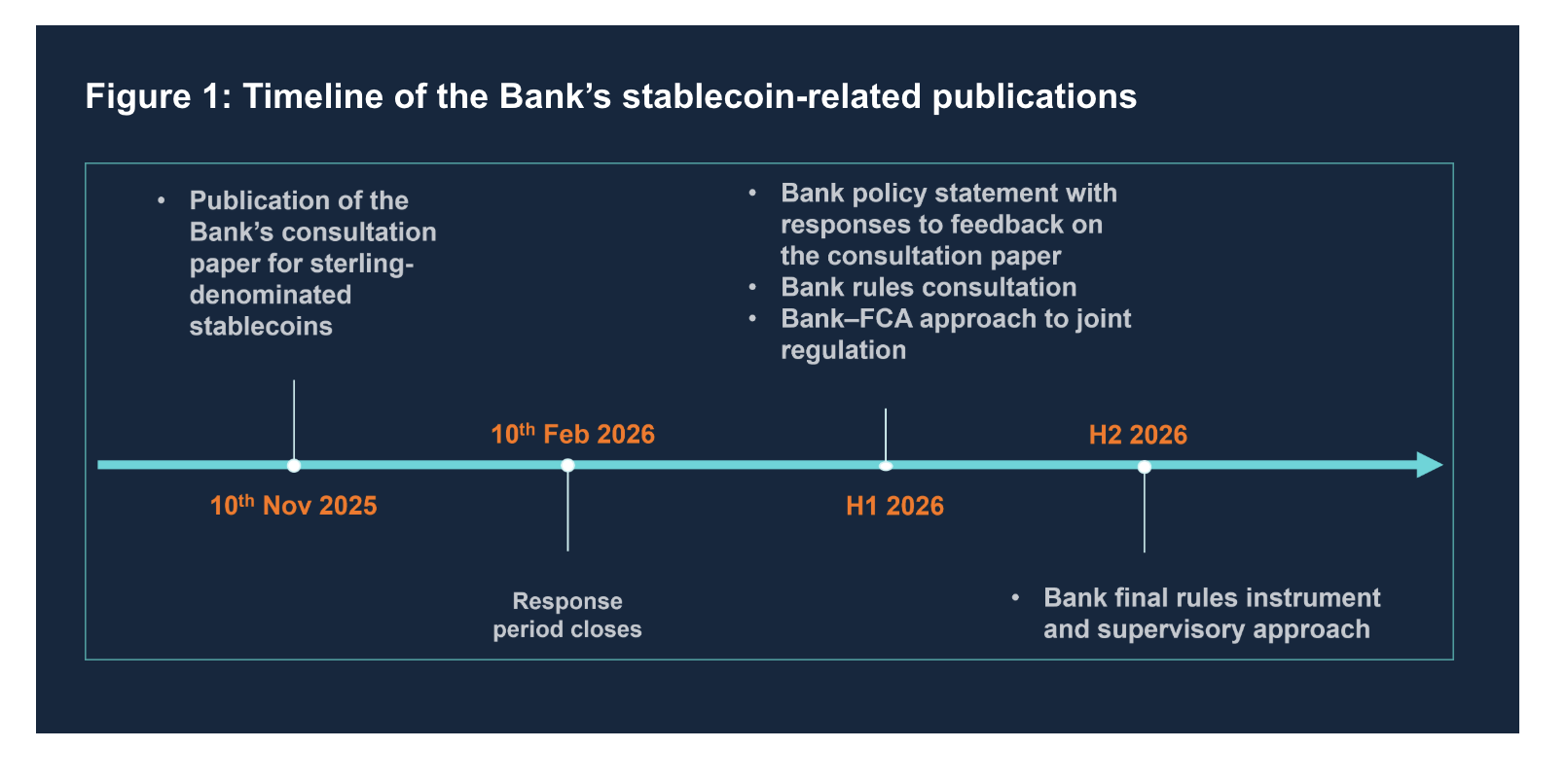

The UK regulatory transition for stablecoins will unfold through 2026, as shown in the timeline:

Proposed regulatory regime timeline | Source: Bank of England

The timeline illustrates the Bank of England’s plan to finalize stablecoin regulation. The consultation opened on November 10, 2025 and runs until February 10, 2026.

The BoE and the FCA will publish policy feedback and consult on detailed rules in the first half of 2026. Final rules and the supervisory approach will arrive in the second half of 2026.

The Broader Impact on the UK Financial System

Stablecoins are becoming a larger part of global payments. With new policy proposals, the United Kingdom aims to treat stablecoins as a core part of its future payment infrastructure.

A clear framework aims to encourage responsible growth, attract investment, and give firms more confidence when building payment-focused products.

Banks, fintech firms, technology companies, and global processors could all face new rivals as systemic stablecoins introduce faster transfers, lower costs, and easier links to new financial applications.

However, industry reactions reveal differing views and highlight the sector’s continued division. Some argue the proposals remain too strict and limiting and may slow product development during the transition period.

Views on proposal | Source: X @itxmaddy_xyz

Others say the rules bring essential clarity and that firms should begin preparing to comply. These mixed views reflect the wider debate about innovation, stability, and the future shape of digital payments in the United Kingdom.

Views on proposal | Source: X @First1Bitcoin

Additionally, the consultation also links directly to the Bank of England’s work on a potential digital pound. Policymakers could be shaping a system where private stablecoins and a central bank digital currency (CBDCs) operate together.

The UK stablecoin framework aims to set the foundation for a future in which digital money prevails.

It brings ongoing debates to the sector, drawing attention not only to the potential benefits of a regulated environment but also to concerns such as reduced privacy under future CBDC models.

Will the new rules apply to foreign stablecoins like USDC or Tether USD?

Foreign stablecoins can operate in the UK, but they remain non-systemic unless they reach large-scale use in sterling payments. The full systemic regime applies only when a token influences the stability of the UK payment system.

Could a UK stablecoin issuer become a bank under this framework?

An issuer may seek a banking license if it wants to accept deposits or pay interest, but the stablecoin regime itself does not grant banking permissions. Stablecoin issuers must stay within the limits set by the prudential framework.

How will small fintech firms adapt to the reserve and capital rules?

Smaller firms can operate under the FCA’s non-systemic regime, which has lighter requirements. The systemic rules apply only when a stablecoin reaches a size and reach that could affect financial stability.

Does the consultation change the timeline for a potential digital pound?

The consultation does not set a launch date for a digital pound. It positions stablecoin rules as a foundation that allows a central bank digital currency to enter the system later without causing disruption.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Lorena Nessi is an award-winning journalist and media technology expert with 15 years of experience in digital culture and communication. Based in Oxfordshire, UK, she combines academic insight with hands-on media practice.

She holds a PhD in Communication, Sociology, and Digital Cultures, and an MA in Globalization, Identity, and Technology.

Lorena has taught at Fairleigh Dickinson University, Nottingham Trent University, and the University of Oxford. She is a former producer for the BBC in London, with additional experience creating television content in Mexico and Japan.

Her research focuses on digital cultures, social media, technology, capitalism, and the societal impact of blockchain innovation.

She has written extensively on digital media and emerging technologies, with her work featured in both academic and media platforms. Her Web3 expertise explores how blockchain technologies shape culture, economics, and decentralized systems.

Outside of work, Lorena enjoys reading science fiction, playing strategic board games, traveling, and chasing adventures that get her heart racing. A perfect day ends with a relaxing spa and a good family meal.

Easy

Easy