10 Countries Where Crypto Gains Are Still Tax-Free in 2026

Share

Key Takeaways

Crypto is treated as property, so selling, swapping, spending, or earning tokens can all create taxable events that affect your IRS tax refund.

DeFi activity, staking rewards, and stablecoin transactions often trigger reportable income or capital gains many taxpayers overlook.

Accurate cost basis tracking and proper loss reporting can reduce tax liability and potentially increase your IRS tax refund.

Filing by April 15, 2026 with complete digital asset reporting helps prevent delays, penalties, and refund processing issues.

Crypto activity can directly change your federal tax bill, and that means it can increase, shrink, or delay your IRS tax refund. With expanded digital asset reporting rules now in effect and broker reporting beginning under new regulations, accuracy matters more than ever.

For the 2025 U.S. tax year (returns filed in 2026), the standard federal filing deadline is April 15, 2026. Filing for an extension generally moves the paperwork deadline to October 15, 2026, but taxes owed must still be paid by April to avoid penalties and interest under current IRS rules.

Below is a fully detailed breakdown of what crypto gains and losses must be reported this year, how they affect refunds, and real-world examples based on current IRS law.

Crypto Tax Reporting Rules for 2025 US Tax Year

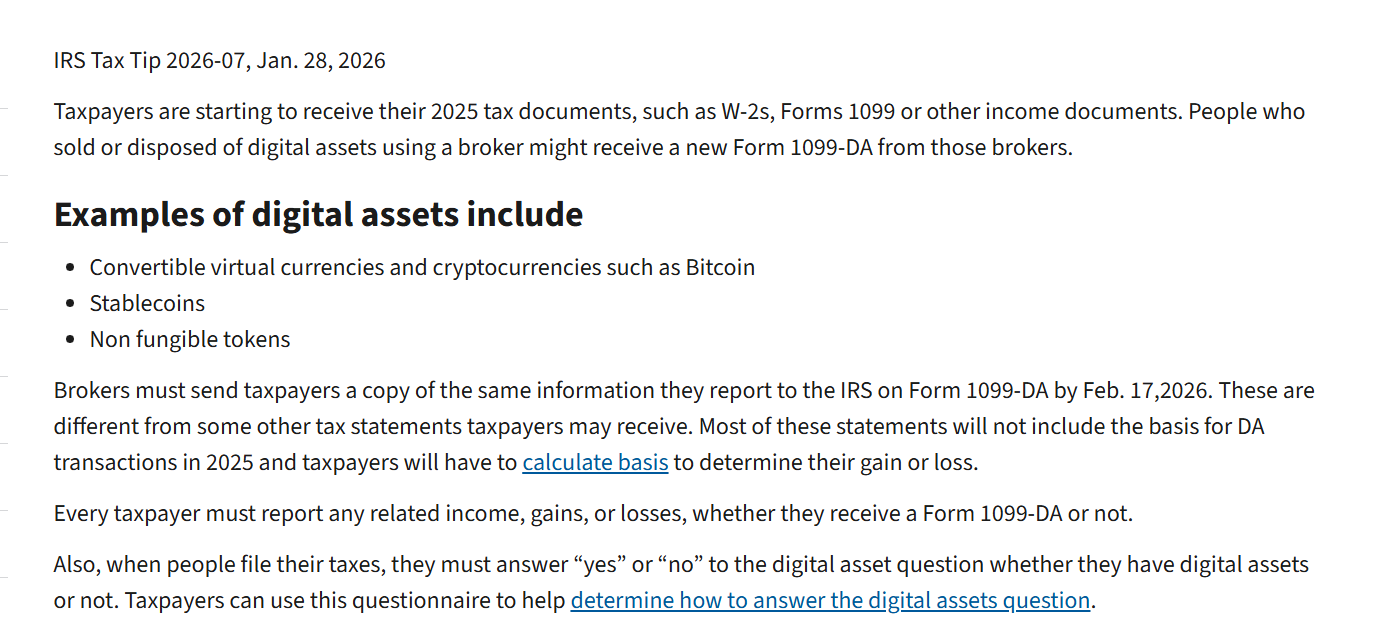

Digital assets, including Bitcoin, Ethereum, stablecoins, NFTs, and other tokens, are treated as property for federal tax purposes. That means most transactions fall under capital gains and capital losses rules, while certain receipts are taxed as ordinary income.

For 2025 transactions, broker reporting regulations begin applying under Form 1099-DA rules. Brokers generally report gross proceeds from sales and exchanges, while taxpayers remain responsible for accurately determining cost basis and resulting gains or losses.

— Gordon Law Group | Crypto Tax Lawyer (@gordonlawltd) February 17, 2026

Every federal return also includes a required digital asset question on Form 1040. Failure to answer accurately can trigger processing issues or compliance notices.

Crypto Transactions That Must Be Reported to IRS

Selling Cryptocurrency for US Dollars

Selling Bitcoin (BTC), Ether (ETH), Solana (SOL), XRP, Chainlink (LINK), or other tokens for USD is a taxable event.

Example:

Purchased 0.5 BTC for $10,000

Sold for $14,000

Capital gain = $4,000

If held longer than one year, the gain is generally taxed at long-term capital gains rates. If held one year or less, it is short-term and taxed at ordinary income rates.

Trading One Cryptocurrency for Another

Swapping ETH for SOL or BTC for USDC is taxable.

Example:

Bought 2 ETH for $4,000

Later swapped for SOL valued at $5,500

Capital gain = $1,500

Even though no cash was withdrawn, the IRS treats this as a disposition of ETH. This is one of the most common reporting mistakes that reduces refunds or creates unexpected tax bills.

𝗜𝘁’𝘀 𝘁𝗮𝘅 𝘀𝗲𝗮𝘀𝗼𝗻. Sorry for the jump scare.

This is the first year the IRS is standardizing crypto tax reporting. So we’ve teamed up with @CoinTracker to make it easier for you.

Using crypto to buy products or services triggers a capital gain or loss.

Example:

Acquired 1 ETH at $2,000

Used it later to purchase equipment when ETH was worth $2,500

Capital gain = $500

Spending appreciated crypto can shrink an IRS tax refund if not properly planned.

Stablecoin Sales and Swaps

Stablecoins such as USDC and USDT are also property under IRS rules. Even small changes in value create reportable gains or losses.

Example:

Purchased 10,000 USDC at slight premium totaling $10,050

Redeemed for $10,000

Capital loss = $50

While small individually, multiple stablecoin transactions can materially affect tax totals.

Staking Rewards and Mining Income

Staking and mining generally produce ordinary income equal to fair market value when received.

Example:

Received staking rewards worth $1,200

$1,200 reported as ordinary income

Later sale creates additional gain or loss:

Sold tokens for $1,500

Capital gain = $300

Failure to separate income reporting from capital gains reporting can result in double taxation errors or underreporting.

Crypto Capital Gains and IRS Tax Refund Impact

Refunds are calculated based on total tax liability minus withholding and estimated payments.

Crypto can affect refunds in two main ways:

Increasing total tax owed due to unreported gains

Increasing refunds if capital losses properly offset gains

Capital Loss Offsets and Refund Optimization

Capital losses first offset capital gains. If losses exceed gains, up to $3,000 may offset other income per year, with remaining losses carried forward.

Example:

$7,000 in crypto gains

$5,000 in crypto losses

Net taxable gain = $2,000

If losses are not reported, the taxpayer may overpay and reduce their refund.

Digital Asset Reporting Forms for 2025 Filing Season

Most crypto investors will interact with:

Form 8949, lists individual sales and exchanges

Schedule D, summarizes total capital gains and losses

Schedule 1, reports additional income such as staking rewards

Schedule C, used for business-related crypto income or mining operations

Broker reporting under Form 1099-DA may not include complete cost basis information for 2025 transactions, making accurate self-tracking essential.

IRS Filing Deadline and Extension Rules for 2026

For 2025 income:

Standard filing and payment deadline: April 15, 2026

Extension filing deadline: October 15, 2026

Payment still due by April to avoid penalties and interest

Estimated tax requirements apply if substantial gains were realized during the year and insufficient withholding occurred.

Failure to make estimated payments can reduce refunds or generate penalties.

DeFi and On-Chain Activity Tax Reporting for 2025 US Tax Year

Decentralized finance transactions create tax consequences that are often more complex than simple buy-and-sell activity on centralized exchanges. Because DeFi occurs directly on blockchain networks, there is typically no consolidated tax statement that captures all taxable events. Each smart contract interaction must be analyzed under existing IRS property tax principles.

Digital assets remain classified as property under federal tax law. That means any time a token is disposed of, exchanged, or received as compensation or reward, there may be a reportable event.

Liquidity Pool Transactions and Tax Treatment

Providing liquidity to automated market makers (AMMs) such as Uniswap, Curve, or similar platforms often involves depositing two tokens into a pool in exchange for a liquidity provider (LP) token.

From a tax perspective, this can trigger a disposition.

Common structure:

User deposits ETH and USDC into a pool

Receives LP token representing pool share

If the transaction is treated as exchanging ETH and USDC for a new LP token, that exchange may be taxable. Each deposited token could generate a gain or loss depending on its fair market value at the time of deposit.

Example:

Purchased ETH at $1,500

ETH worth $2,200 when deposited into LP

Capital gain = $700

When liquidity is later removed, another taxable event may occur because LP tokens are exchanged back into underlying assets.

The result is potentially multiple taxable events from one liquidity strategy.

Yield Farming and Token Incentive Income

Yield farming frequently distributes governance tokens or reward tokens.

Under current IRS guidance principles:

Tokens received are generally taxable as ordinary income at fair market value at the time the taxpayer gains control over them.

Example:

Received reward tokens worth $2,000

$2,000 reported as ordinary income

If those tokens are later sold for $2,500:

Additional $500 capital gain must be reported

Failure to recognize income at receipt is one of the most common DeFi reporting mistakes that can reduce refunds or generate IRS notices.

Lending and Borrowing Protocol Tax Considerations

Lending crypto on platforms that pay interest in tokens generally creates taxable income equal to the value of interest received.

Borrowing against crypto, by contrast, is generally not taxable if structured as a loan. However:

If collateral is liquidated, that liquidation is a taxable disposition.

Understanding protocol mechanics is critical to proper classification.

Wrapped Tokens and Cross-Chain Bridges

Wrapping assets or bridging between blockchains can trigger tax consequences depending on structure.

For example:

Converting ETH to wETH may or may not be treated as a taxable exchange depending on analysis of control and token equivalence.

Bridging ETH to another chain where a new token is issued may be treated as a disposition if economically distinct property is received.

Documentation of fair market value at the time of conversion is essential.

NFT and Governance Token Transactions

Governance tokens often behave like capital assets. Buying and later selling them generates capital gains or losses.

NFTs are also property. Selling an NFT at a higher price creates capital gain. Income received from NFT royalties may be treated differently depending on role and structure.

Accurate blockchain transaction logs are critical because there is often no consolidated statement summarizing activity.

Common Crypto Tax Errors That Shrink IRS Tax Refunds

Incorrect Cost Basis Calculations

Cost basis must include purchase price plus transaction fees.

Failing to include fees inflates taxable gains.

Example:

Bought BTC for $20,000 plus $200 fee

True basis = $20,200

Selling for $25,000 produces:

Correct gain = $4,800

Incorrect gain if fee ignored = $5,000

That $200 difference directly affects the tax owed and refund amount.

Ignoring Partial Dispositions

Selling part of a position requires identifying which tax lot is sold.

If a taxpayer purchased BTC at different times:

Lot 1 at $10,000

Lot 2 at $30,000

Selling 0.5 BTC requires determining whether FIFO, specific identification, or other method applies.

Using wrong lot selection can significantly increase taxable gains.

Failing to Track Wallet-to-Wallet Transfers

Moving assets between personal wallets is not taxable. However, without proper documentation, automated software may treat transfers as sales.

Duplicate gain reporting artificially increases tax liability and reduces refunds.

Maintaining internal records of transfer timestamps and wallet addresses prevents this error.

Relying Solely on Exchange 1099 Forms

Exchange forms often show proceeds but may not reflect cost basis for assets transferred in from other platforms.

If BTC was bought on Exchange A and sold on Exchange B:

Exchange B may report proceeds only

Taxpayer must supply original purchase basis

Failure to reconcile results in overstated gains.

BIG BOOST: Americans are receiving larger tax refunds this year, even though taxpayers are filing at a slower pace than they were a year ago.

The average tax refund has climbed to $2,290 — up 10.9% from this time last year — according to the latest IRS data.

Long-Term vs Short-Term Capital Gains Strategy for 2025

Capital gains tax rates differ based on holding period.

Assets held more than one year typically qualify for long-term capital gains rates, which are lower than ordinary income rates for many taxpayers.

Comparison Example:

Short-term gain of $10,000 taxed at 32 percent = $3,200 tax

Long-term gain of $10,000 taxed at 15 percent = $1,500 tax

Difference = $1,700

This difference directly impacts total tax liability and IRS tax refund outcome. Strategic holding periods can significantly influence after-tax returns.

Crypto Loss Harvesting Strategy for 2025 Tax Planning

Tax-loss harvesting involves realizing losses before year-end to offset gains.

Under current federal law, wash sale rules explicitly apply to securities. Cryptocurrency is classified as property and not currently subject to statutory wash sale rules, though legislative proposals have aimed to change this. Taxpayers should monitor regulatory updates.

Example:

$12,000 gains earlier in year

Realize $10,000 loss in December

Net taxable gain = $2,000

Without harvesting, tax would apply to a full $12,000.

Losses exceeding gains can offset up to $3,000 of ordinary income annually, with excess carried forward.

Accurate documentation of sale dates and market values protects loss deductibility.

Stablecoin Treasury Backing and Tax Transparency Developments

IMF research shows stablecoins increasingly backed by short-term US Treasuries. This enhances reserve transparency but does not alter tax classification.

Disposing of stablecoins remains a taxable event even if price movement is minimal.

Institutional integration and regulatory focus increase likelihood of third-party reporting consistency and cross-checking with IRS systems.

IRS Enforcement and Digital Asset Compliance Expansion

IRS enforcement has expanded through:

Blockchain analytics tools

Broker reporting regulations including Form 1099-DA implementation

Enhanced digital asset question disclosure

Increased reporting transparency reduces probability that unreported gains go unnoticed.

Accurate and complete reporting reduces audit risk and refund processing delays.

Estimated Tax Payment Requirements for Active Crypto Traders

Significant realized gains during 2025 may require quarterly estimated tax payments.

Failure to make adequate estimated payments can result in penalties even if a refund is generated at filing.

Safe harbor provisions typically allow penalty avoidance if:

100 percent of prior-year tax was paid (110 percent for higher income taxpayers), or

90 percent of current-year tax liability was paid

Monitoring realized gains throughout the year helps prevent unexpected penalties.

Practical Steps to Protect 2026 IRS Tax Refund

Consolidate exchange and wallet transaction history

Reconcile all wallet transfers

Categorize transactions as income or capital events

Confirm accurate cost basis tracking

Review Form 1099-DA and other broker statements carefully

Verify digital asset disclosure question accuracy

Seek professional review if DeFi, cross-chain, or high-frequency trading activity occurred

Careful documentation, correct classification, and timely filing under current IRS law ensure compliance and help safeguard refund outcomes for the 2025 tax year.

IRS Tax Refund Outlook for 2025 Crypto Filers

Crypto activity does not automatically reduce an IRS tax refund. What determines the final outcome is accuracy, documentation, and timing.

Properly reporting gains ensures tax liability is calculated correctly. Properly reporting losses ensures overpayment does not occur. Misreporting either direction can delay processing, trigger notices, or reduce a refund unnecessarily.

For the 2025 tax year filed in 2026, compliance matters more than ever due to expanded broker reporting and increased IRS visibility into digital asset transactions. Capital gains, staking rewards, DeFi income, stablecoin swaps, and cross-chain transfers must all be evaluated under current property tax rules.

An IRS tax refund is simply the difference between what was paid during the year and what is actually owed. Overstating gains reduces a refund. Failing to claim losses reduces a refund. Underreporting income can create penalties that eliminate a refund entirely.

Careful reconciliation of transaction history, correct cost basis tracking, and proper classification of income versus capital activity protect both compliance and refund outcomes.

With April 15, 2026 as the standard filing deadline for 2025 income, early preparation and complete digital asset reporting remain the most reliable way to secure an accurate IRS tax refund under current law.

Does receiving a 1099-DA mean IRS already calculated my crypto taxes?

No. Form 1099-DA and other broker statements generally report transaction proceeds, and in some cases limited additional information. They do not automatically calculate your capital gains, losses, or income. You are responsible for determining accurate cost basis, holding period, and correct tax treatment. If basis is missing or incomplete, reporting errors could directly affect your IRS tax refund.

Can crypto losses increase my IRS tax refund?

Yes, in many cases. Capital losses first offset capital gains. If total losses exceed gains, up to $3,000 can typically offset ordinary income per year, with remaining losses carried forward. Properly reporting losses can reduce total tax liability, which may increase your IRS tax refund if sufficient taxes were already paid during the year.

Do small crypto transactions really need to be reported?

Yes. The IRS treats digital assets as property, and technically each taxable disposition must be reported, even small transactions. While minor rounding differences may not materially change tax owed, repeated small gains or losses can accumulate and affect overall liability. Incomplete reporting may also create inconsistencies with broker reporting.

Will filing an extension delay my IRS tax refund?

Filing an extension does not automatically delay a refund if no additional tax is owed. However, refunds are generally issued only after a return is processed. An extension moves the filing deadline, not the payment deadline. If you expect a refund, filing earlier in the season typically results in earlier processing, provided your crypto reporting is accurate and complete.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy