Crypto tax havens: where are they?| Credit: Hameem Sarwar /CCN

Share

Key Takeaways

A 0% crypto tax rate in 2026 refers to local taxation only and does not remove reporting duties under global frameworks like the OECD Crypto-Asset Reporting Framework (CARF).

Countries reach 0% outcomes through different systems, including no-tax regimes, capital gains exemptions, and territorial tax rules, with classification often more important than location.

Private investing usually qualifies for 0% treatment, but frequent trading, automation, staking, mining, or advisory activity can trigger business or income tax exposure.

Regulatory transparency now defines crypto tax planning, since zero local tax no longer means low visibility across borders or protection from home-country enforcement.

As global crypto reporting rules expand in 2026, the idea of “0% crypto tax” has become harder to define, even in places often labeled crypto tax havens.

Several jurisdictions still offer zero taxation on crypto gains, but the legal basis behind those claims differs widely. Some countries impose no personal income tax or capital gains tax (CGT).

Others reach a 0% outcome only when gains meet strict conditions tied to tax residency, source of income, and the nature of crypto activity.

This article explains how 0% crypto tax regimes actually work in 2026, which countries genuinely qualify, and where zero taxation depends on classification rather than location.

What 0% Crypto Tax Means Under Tax Law in 2026

In tax terms, a 0% crypto tax regime means no personal income tax and no capital gains tax applied locally to crypto assets.

This definition applies only within the jurisdiction itself. It does not remove:

Tax obligations tied to foreign residency

Corporate or business tax exposure

International reporting requirements

As a result, crypto gains can remain untaxed locally while still becoming taxable elsewhere. For instance, U.S. citizens remain subject to worldwide taxation regardless of relocation, and many other countries tax based on citizenship or worldwide income principles.

The country sections below show how different jurisdictions apply this framework in practice, and where a 0% outcome depends on residency status, activity classification, or source of income rather than headline tax rates.

Countries With True 0% Crypto Tax for Individuals: Crypto Tax Heavens?

These jurisdictions impose no personal income tax and no capital gains tax, regardless of asset type. For individual crypto holders, gains remain outside the tax base.

United Arab Emirates: No Personal Income Tax, Conditional Business Exposure

In 2026, the United Arab Emirates (UAE) continues to offer 0% personal income and capital gains tax on crypto for individuals.

This means that individuals across all emirates (including Dubai and Abu Dhabi) pay 0% on crypto trading, staking, mining, or selling for personal use, with no capital gains tax imposed.

However, the regulatory approach has shifted from informal tolerance to clearly defined thresholds that high-volume traders and professionals must now track carefully.

No personal income or capital gains tax: Private crypto holding and occasional investing remain untaxed for individuals.

Business activity threshold (AED 1 million): Individuals whose crypto-related activity resembles a business and generates more than AED 1,000,000 in annual revenue must register for corporate tax, even without forming a company.

Corporate tax buffer: Profits up to AED 375,000 remain taxed at 0%. Once the registration threshold is crossed, profits above AED 375,000 face a 9% corporate tax rate.

VAT clarification: Crypto transfers and conversions are exempt from value-added tax (VAT). Crypto-paid services still count as taxable revenue, and VAT registration applies once service income exceeds AED 375,000 annually.

Free zone qualifying income: Free zone entities retain a 0% corporate rate only on qualifying income, including investment management and proprietary trading, provided they meet substance requirements such as local offices, staff, and operating spend.

Mainland exposure risk: Free zone companies that generate income from mainland UAE entities risk losing the 0% rate on that income stream.

The UAE has implemented the Organization for Economic Cooperation and Development (OECD) Crypto-Asset Reporting Framework (CARF).

It is important to note that, under Article 21, resident individuals and businesses with annual revenue below AED 3,000,000 can apply for Small Business Relief. Once approved, the tax authority treats them as having no taxable income until December 31, 2026.

In practice, this moves the effective 0% corporate tax threshold from AED 1 million to AED 3 million for eligible applicants.

This framework keeps the UAE attractive for individual investors while drawing a firm line around professional trading, advisory services, and cross-border transparency.

While the UAE relies on thresholds and classification to preserve its zero-tax appeal, some jurisdictions remove taxation entirely and focus instead on reporting and compliance.

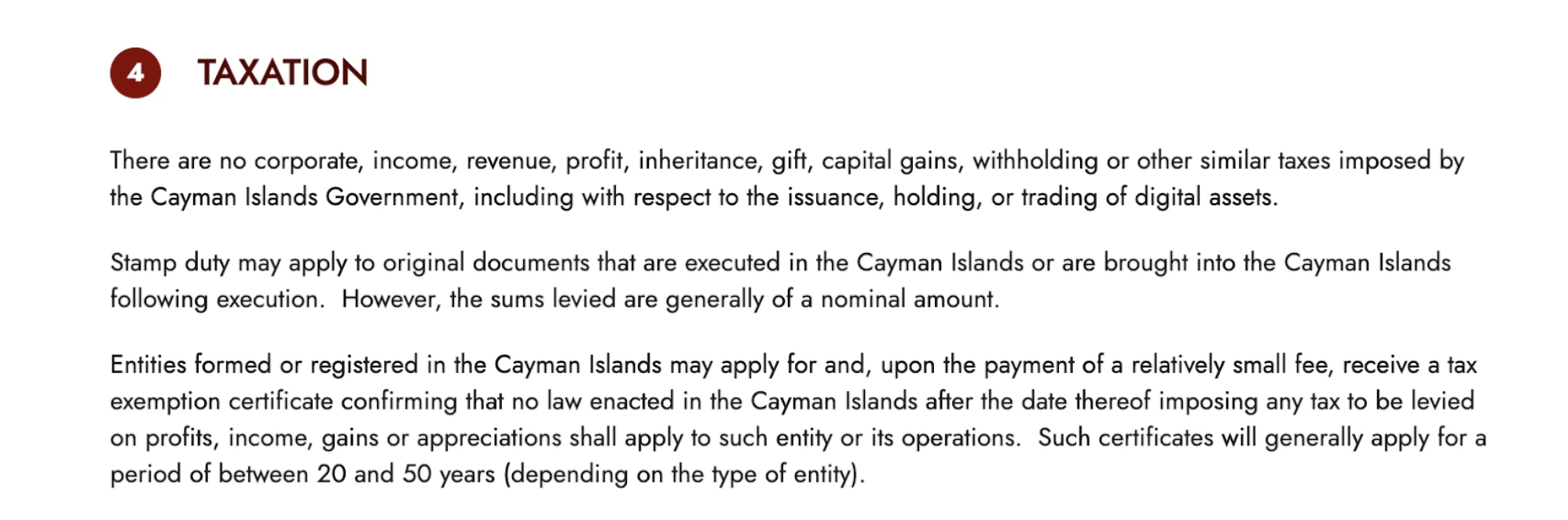

Cayman Islands: No Direct Taxes, Reporting Starts in 2026

Unlike jurisdictions that rely on thresholds or activity classification, the Cayman Islands removes crypto gains entirely from the tax base.

This means that, in 2026, the Cayman Islands will continue to impose no income tax, no capital gains tax, and no corporate tax on crypto for individuals and many entities.

Taxation rule in Cayman Islands | Source: Global Legal Insights

This zero-tax status applies to individuals and many entities, making it a classic offshore haven for crypto holdings.

No income or capital gains tax: Crypto gains remain untaxed for individuals and qualifying entities.

No corporate tax: Cayman does not levy corporate income tax on crypto businesses.

CARF effective January 1, 2026: The OECD Crypto-Asset Reporting Framework formally entered into force at the start of 2026.

Self-certification requirement: Cayman-based exchanges must now collect tax residency self-certification forms from all users.

Reporting timeline: The first automatic exchange of crypto account data with foreign tax authorities will occur in 2027, covering the 2026 tax year.

While Cayman removes taxation altogether, other countries rely on exemptions that depend on how crypto holdings are classified under domestic tax law.

Bermuda: No Personal Income or Capital Gains Tax, Corporate Exception Applies

Bermuda follows a similar zero-tax model to the Cayman Islands, removing crypto gains entirely from the personal tax base while applying targeted rules to large corporate groups.

In 2026, Bermuda imposes no personal income tax and no capital gains tax on crypto for individuals.

No personal income or capital gains tax: Crypto gains remain untaxed for individual holders.

No general corporate income tax: Most local companies operate outside a standard corporate tax regime.

Corporate exception for large groups: A 15% corporate income tax applies only to in-scope multinational enterprise groups that meet the global revenue threshold under Organization for Economic Cooperation and Development (OECD) Pillar Two rules.

No impact on individuals: Private investors and small entities remain outside the corporate tax scope.

Regulatory focus over taxation: Bermuda prioritizes licensing, supervision, and compliance rather than taxing crypto activity itself.

This structure allows Bermuda to preserve its zero-tax appeal for individuals while aligning with international minimum tax standards for large multinational groups.

While jurisdictions like the UAE, Cayman Islands, and Bermuda remove crypto gains entirely from the personal tax base, other countries reach similar 0% outcomes through capital gains exemptions rather than zero-tax systems.

Capital Gains Exemptions Supporting 0% Crypto Outcomes

These countries tax income but exempt private capital gains, including crypto held as private wealth. The distinction between private investing and professional activity remains decisive.

Switzerland: Private Capital Gains Exempt, Wealth Tax Applies

Switzerland remains one of the most established jurisdictions for private crypto investors, combining capital gains exemptions with ongoing wealth taxation.

In 2026, crypto assets held as private wealth remain exempt from capital gains tax for individual investors.

Private investors pay 0% capital gains tax (CGT on sales, but annual wealth tax (0.3–1% in most cantons) applies to total assets, including crypto.

On January 1, 2026, Switzerland formally implemented the OECD-CARF.

This means that from that date, Swiss exchanges are collecting data to be shared with the tax office. If a resident has “hidden” crypto in the past, 2026 is effectively the final year for “voluntary disclosure” before the data becomes visible to the authorities.

Territorial Tax Systems With 0% Outcomes for Crypto

These jurisdictions tax only locally sourced income. Crypto gains often fall outside the tax base, but source and intent remain decisive.

Singapore: No Capital Gains Tax, Business Classification Risk

Singapore does not impose capital gains tax and continues to treat private crypto investing as non-taxable when it does not qualify as a trade or business.

In 2026, individual crypto investors remain untaxed on disposals unless activity crosses into commercial territory.

No capital gains tax: Crypto disposals by private investors remain untaxed.

Income tax classification: Frequent trading, automation, or reliance on crypto as income can trigger income tax.

Low-income tax rates: Even when taxable, Singapore maintains comparatively low progressive rates.

Singapore’s clarity attracts investors, but the line between private investment and trading remains actively enforced.

Hong Kong applies a similar framework, with an important expansion in exemptions for structured investment vehicles.

Hong Kong: Capital vs. Revenue Split With Expanded Fund Exemptions

Hong Kong continues to distinguish between non-taxable capital gains and taxable trading profits, while expanding exemptions for funds and family offices.

In 2026, most individual crypto investors remain untaxed, provided activity does not qualify as a trade or business.

No capital gains tax: Long-term crypto gains classified as capital remain untaxed.

Territorial system: Only Hong Kong-sourced profits are taxable.

Fund and family office exemption: Privately offered funds and qualifying family offices can access a 0% rate on crypto gains, even with frequent trading, if substance and asset requirements are met.

Retail investor treatment: Individuals trading on Securities and Futures Commission (SFC)-licensed exchanges generally remain untaxed if crypto trading is not their primary business.

Hong Kong’s 2026 updates strengthen its position as a structured crypto finance hub while

preserving the capital gains exemption for individuals.

Where Crypto Gains Face 0% Tax in 2026: Country Comparison

The table below compares how different jurisdictions reach a 0% crypto tax outcome in 2026. While all listed countries can offer zero taxation for individuals, the legal basis ranges from no-tax systems to territorial and capital gains exemption regimes.

Country

Personal tax on crypto gains

System type

Main condition

United Arab Emirates (UAE)

0%

No direct taxes

Non-business activity

Cayman Islands

0%

Territorial

Reporting only

Panama

0%

Territorial

Foreign-sourced gains

Paraguay

0%

Territorial

Non-commercial activity

Bermuda

0%

No income tax

Individual, not MNE

Singapore

0%

Capital gains exempt

Not a trading business

Switzerland

0%

Private wealth exemption

Non-professional investor

Georgia

0%

Explicit exemption

Individual status

Vanuatu

0%

No income tax

Residency

British Virgin Islands

No direct taxes

Individual holder

Mauritius

0%

Capital gains exempt

Non-business income

Hong Kong

0%

Territorial

Non-local source

While the table shows a 0% crypto tax outcome across multiple jurisdictions, that result depends on how tax authorities classify the activity.

In most countries, crypto gains remain untaxed only when treated as private investment rather than business income.

Trading frequency, use of automation, reliance on crypto as a primary income source, or the provision of services can shift gains from capital into taxable income. Once that reclassification occurs, zero-tax treatment no longer applies, even in jurisdictions commonly described as crypto-friendly.

The remaining jurisdictions in the table follow frameworks already outlined.

Panama and Paraguay apply territorial tax systems, where foreign-sourced crypto gains remain untaxed unless activity becomes local or commercial.

Georgia and Mauritius rely on capital gains exemptions for private investors, with taxation triggered once crypto activity qualifies as business income.

Vanuatu and the British Virgin Islands impose no personal income or capital gains tax, placing them alongside Cayman and Bermuda as true zero-tax jurisdictions, with practical considerations centered on residency and compliance rather than taxation itself.

Across all cases, a 0% crypto tax outcome generally covers private holding and occasional investing. However, it is important to note that yield generation, staking, mining, advisory services, or frequent trading might introduce additional tax and reporting considerations

Why Regulatory Monitoring and Professional Advice Still Matter

Crypto regulation often moves more slowly than technological development, but regulatory changes can materially affect tax treatment over time.

For that reason, individuals relying on a 0% crypto tax framework should regularly review local guidance and regulatory updates rather than assume rules will remain static.

Because crypto tax outcomes depend on activity classification, residency status, and reporting obligations, consulting a qualified tax advisor remains essential before structuring holdings around a 0% tax assumption.

In 2026, a 0% tax regime is a reporting-heavy environment. The implementation of CARF means that zero local tax does not mean zero global visibility.

Taxpayers must now ensure that their “tax home” is defensible against high-tax jurisdictions using automated data-sharing to flag “tax nomads” who lack genuine local substance.

Taken together, the jurisdictions most often described as crypto tax havens in 2026 include the United Arab Emirates, Cayman Islands, Bermuda, British Virgin Islands, Vanuatu, and, under specific conditions, Switzerland, Singapore, and Hong Kong.

Each offers a lawful path to a 0% crypto tax outcome, either through the absence of income and capital gains taxes or through exemptions for private investment.

However, the label “crypto tax haven” now reflects legal structure and classification more than secrecy, as reporting, substance, and residency rules determine whether zero taxation holds in practice.

Does a 0% local tax rate mean I don’t have to report my crypto to anyone?

No. In 2026, the OECD’s Crypto-Asset Reporting Framework (CARF) is active. Even in 0% zones like the UAE or Cayman Islands, exchanges must collect your data and share it with your home country’s tax authority. 0% refers to the rate, not a lack of reporting.

When does “personal investing” become a “taxable business” in the UAE?

The threshold is AED 1,000,000 in annual revenue. If your crypto activity generates more than this, you must register for Corporate Tax. However, you still enjoy a 0% rate on the first AED 375,000 of profit.

Is Switzerland truly 0% for crypto if there is a “Wealth Tax”?

While capital gains (profits from selling) are 0% for private investors, you pay a “Wealth Tax” on your total holdings. This usually ranges from 0.3% to 1% of your portfolio value as of December 31 each year, depending on your Canton.

Can “AI Agents" on Ethereum trigger new tax obligations in 2026?

Yes. If an AI agent trades on your behalf autonomously and generates frequent, high-volume transactions, tax authorities in jurisdictions like Singapore or Hong Kong may classify this as “commercial trading” (badges of trade) rather than passive investing, potentially triggering income tax.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Lorena Nessi is an award-winning journalist and media technology expert with 15 years of experience in digital culture and communication. Based in Oxfordshire, UK, she combines academic insight with hands-on media practice.

She holds a PhD in Communication, Sociology, and Digital Cultures, and an MA in Globalization, Identity, and Technology.

Lorena has taught at Fairleigh Dickinson University, Nottingham Trent University, and the University of Oxford. She is a former producer for the BBC in London, with additional experience creating television content in Mexico and Japan.

Her research focuses on digital cultures, social media, technology, capitalism, and the societal impact of blockchain innovation.

She has written extensively on digital media and emerging technologies, with her work featured in both academic and media platforms. Her Web3 expertise explores how blockchain technologies shape culture, economics, and decentralized systems.

Outside of work, Lorena enjoys reading science fiction, playing strategic board games, traveling, and chasing adventures that get her heart racing. A perfect day ends with a relaxing spa and a good family meal.

Easy

Easy