She Didn't Have a Bank Account — But She Had Bitcoin: Women's Stories of Financial Liberation Across the Globe

Share

Key Takeaways

While Afghan women use crypto to bypass restrictions for secret online education and income, Nigerian women use Bitcoin to finance startups and get around banking barriers.

Filipina foreign workers use crypto platforms to reduce remittance expenses, resulting in record $35.63B inflows in 2025.

Bitcoin education programs in El Salvador and India empower women to manage digital assets even in unbanked regions.

As of late 2025, 39% of women globally engaged with crypto, indicating a change from male-dominated speculation to useful, gender-neutral financial utility.

Imagine watching half of your weekly income vanish into bank fees before you can feed your kids, or needing a man’s signature to create a savings account. This is not a historical narrative for millions of underbanked women – it is their Tuesday.

Yet, year-by-year, something is shifting as technological expansion is steadily dismantling old barriers. Sometimes, a simple smartphone app is what is needed for a woman to build some wealth without ever facing a bank teller’s skepticism. And, cryptocurrency is making this possible. With over 861M users globally, women make up 39% of global cryptocurrency investors as of 2025.

To celebrate International Women’s Day 2026, the article highlights five inspiring stories of women from different continents who are using cryptocurrency and Bitcoin to overcome financial barriers and achieve greater economic independence.

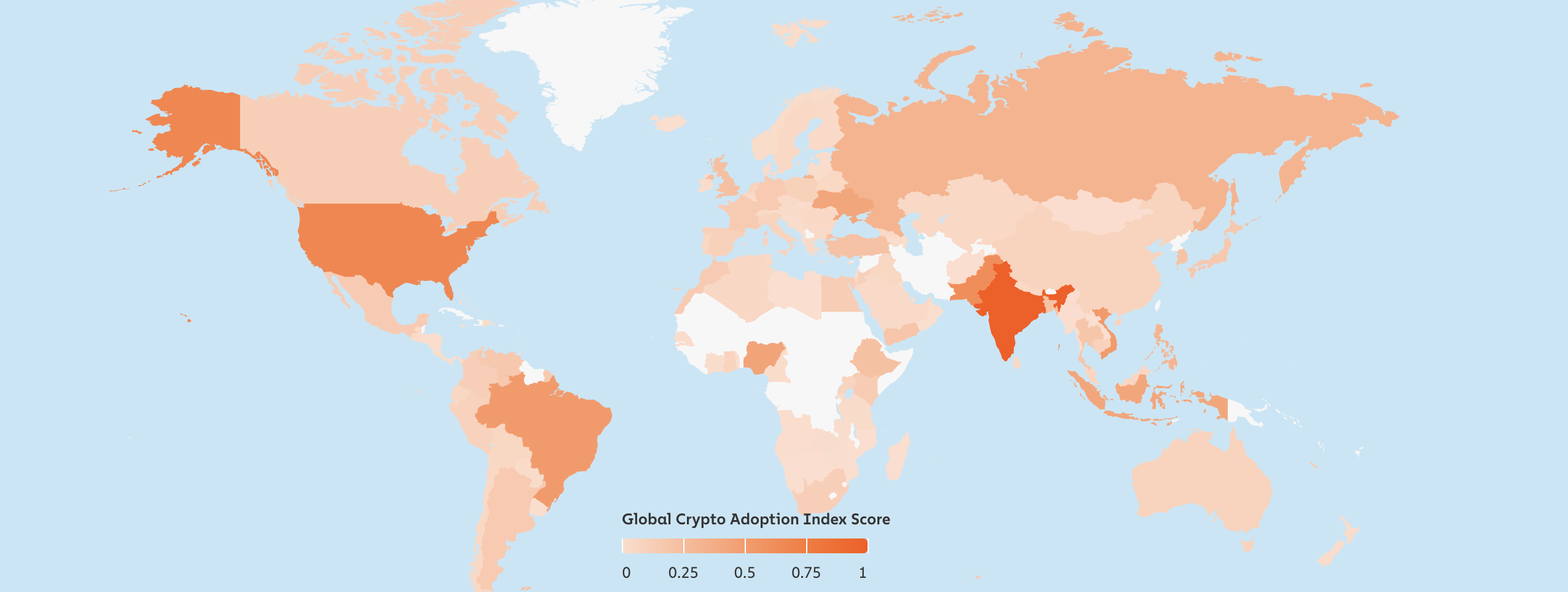

Global Crypto Adoption Index Score 2025 | Chainalysis

Breaking Barriers in Nigeria

In the bustling markets of Lagos, the “why” behind crypto adoption is simple: survival. Nigeria leads Africa in peer-to-peer (P2P) trading, driven by a traditional banking sector which often excludes small-scale female entrepreneurs. How can these ladies maintain the viability of their companies when the local Naira swings so much?

Many female merchants now bypass banks entirely, using stablecoins pegged to the US Dollar to settle international invoices. They bypass the “foreign exchange trap” that hinders conventional businesses by carrying out direct transactions with suppliers via mobile wallets.

Initiatives like Lorraine Marcel’s Bitcoin Dada, which focuses on financial literacy and safe transactions, trained over 300 women in 2025, bringing the total to 1,200 since its founding. Why the surge? Banks often demand collateral women lack, but crypto’s decentralization allows instant, borderless deals.

Revolutionizing Remittances in the Philippines

In the past, sending $200 home meant waiting days for a family member to come to a real pickup location and losing $20 due to predatory wire fees. What happens when you remove the middleman?

For Filipina overseas workers (OFWs), crypto slashes the sting of high remittance fees. In 2025, total inflows reached a record $35.63B, up 3.3% from prior years, with crypto capturing a growing share via apps like Coins.ph.

In order to save up to 6% on bank fees, a nurse in the United States can send stablecoins home, quickly converting them to pesos. Mothers and grandmothers who oversee the local household now have more money since the cost of these transfers has dropped to almost $0. This preserves earnings for family needs like education. With 10% of GDP from OFWs, crypto adoption ranks high, empowering remote financial control and stability amid inflation.

Gaining Ground in El Salvador

The 2021 enactment of El Salvador’s Bitcoin law has spurred financial inclusion for women living in rural areas without banks. Due to a lack of credit history, a female street vendor in San Salvador or El Zonte had no opportunity to expand her business. Women in El Salvador have increasingly gained banking access through digital wallets like Chivo, allowing secure transactions and remittances without traditional bank requirements.

Mandatory acceptance fosters participation in a male-heavy economy, though adoption lingers at around 2% due to education gaps. Still, it offers remittance and savings tools, proving crypto’s equity potential.

Surviving Restrictions in Afghanistan

For women denied access to banks, crypto offers a secret route to financial survival in Taliban-controlled Afghanistan. Bitcoin became “freedom money” in this context. In 2025, amidst internet outages, Kabul women kept online companies, earning stablecoins to support their families. Many regional holders are women, with trading lessons available through platforms such as Zoom. Since 2021, projects such as Roya Mahboob’s Digital Citizen Fund have powered offline education apps, enabling anonymous learning and payments. How? Thanks to its anonymity, crypto enables international transactions without intermediaries. Despite connectivity issues, this tool supports livelihoods and education, emphasising its importance in oppressive situations.

Building Wealth in India

Despite having one of the most tech-savvy populations, millions of rural women in India are still excluded from finance. Lack of records or credit score is a common barrier to obtaining microloans.

In 2025, participation increased, with women accounting for 15% of trading volume and diversifying into Bitcoin, Ethereum (ETH), Solana (SOL), and other tokens. Maharashtra female entrepreneurs use digital IDs to track their companies’ transactions as well as apps for microloans to avoid high bank fees.

Why the boom? Crypto yields outpace stocks, with non-metro cities like Kolkata leading at 20% growth. This builds security in a $1T digital economy, empowering women as key investors.

Why a Gender-Neutral Ledger Matters

The stories of these women prove that financial liberty is about the system’s architecture rather than just the price of a coin. The blockchain is intrinsically gender-blind; it doesn’t care about who you are, where you live, or what your community believes you should be or do. It just cares whether you have the correct key.

The statistics for late 2025 show that reducing the gender gap in finance is a win not only for equality but also for the global economy since women’s financial empowerment boosts GDP growth and strengthens communities. Bitcoin has evolved from a “niche asset” for crypto enthusiasts to a vital tool for previously overlooked economic actors.

Bitcoin bypasses common banking exclusions in remote or biased systems by providing mobile-based financial services like transfers and savings.

Why did women start using cryptocurrencies more frequently?

In markets like India, membership has doubled thanks to enhanced learning, streamlined apps, and success stories, giving them more economic control.

Why is crypto significant for remittances in 2026?

It facilitates immediate cross-border settlement and lowers transaction fees from an average of 7% to less than 1%.

Why are private keys important for women's safety?

Private keys provide women with complete control over their cash, guaranteeing that third parties cannot confiscate or freeze them.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Curious about how technology and crypto reshape global finance, Elizaveta Savenko explores blockchain, AI, decentralized systems, their applications, and regulatory requirements. She contributes to research, educational initiatives, and industry collaborations, examining trends in digital assets and fintech innovation, increasing awareness of the crypto space and its impact on financial systems.

Easy

Easy