HODLers, Meet Homeowners: Fannie Mae to Accept Crypto as Mortgage Collateral for the First Time

Share

Key Takeaways

Better and Coinbase’s new offering could give crypto holders a new way into homeownership without forcing them to sell their Bitcoin first.

The structure is not one simple Bitcoin mortgage. It uses two loans: a standard home loan and a separate crypto-backed down payment loan.

Fannie Mae’s role keeps the main mortgage inside the traditional U.S. housing system, showing that this is a tradfi model with crypto added in, not a fully crypto-native loan.

The product may help crypto-rich buyers, but it also adds risk through extra leverage and the chance of forced crypto liquidation if payments fall behind.

Crypto as mortgage collateral has long felt like a far off dream. However, the day is finally in sight.

On March 26, 2026, Better Home & Finance (Better) and Coinbase partnered to begin offering crypto-backed mortgages for potential homebuyers. The product will roll out over the next few months.

This alone makes the announcement stand out. For years, if you’re a crypto holder and you wanted to buy a home, you usually had one option in selling your assets, moving your money into a bank account, and beginning a standard mortgage. This new model offers a different route, treating cryptocurrencies as something that can support a major real-world purchase.

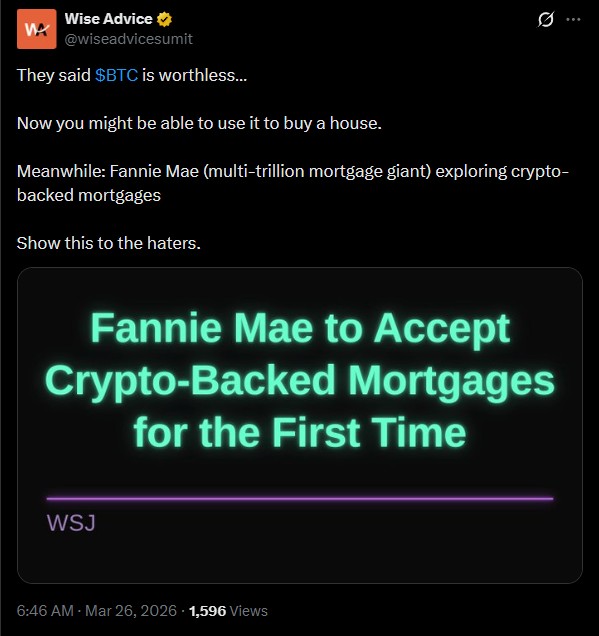

Source: @wiseadvicesumit on X

But while the proposed change sounds meaningful, as it’s a step toward providing crypto holders a real path into the housing market without forcing them to sell, there are a few caveats.

Top Crypto Tax Accounting Software

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Imagine you’re looking at a $500,000 home. Through the new model, perhaps you can pledge $250,000 in Bitcoin to help cover a $100,000 down payment. But that’s not the only step. You won’t just get one big Bitcoin mortgage. Instead, you’ll have to apply for a standard loan as well, totaling two loans to purchase your home.

That two-loan structure is a prime detail. Better is still making a normal conforming mortgage on the house, while the crypto-backed part is a separate loan tied to your down payment. At launch, Better and Coinbase say that eligible assets are Bitcoin and USDC, which shows how tightly controlled this first version is.

Your main home loan could be a normal 15-year or 30-year mortgage, while your crypto sits in custody as a separate down payment loan.

Said main mortgage is where Fannie Mae comes into play. It’s designed to fit Fannie Mae guidelines, which helps keep your home loan inside the standard US mortgage system instead of pushing it into a fully separate crypto lending avenue.

Essentially, Fannie Mae isn’t offering a crypto-native approach, but rather traditional finance allowing crypto to step in the door. It’s digital assets being routed through traditional finance rules.

This process will likely appeal to long-time Bitcoin holders with strong income and good credit who want to buy a home without cutting into their crypto position. One who will hold it to use as collateral for a residence. A long-time Bitcoin holder who bought early, has held, and is ready to buy a home without shrinking their position.

Crypto Moves Closer to Homeownership With New Mortgage Policy

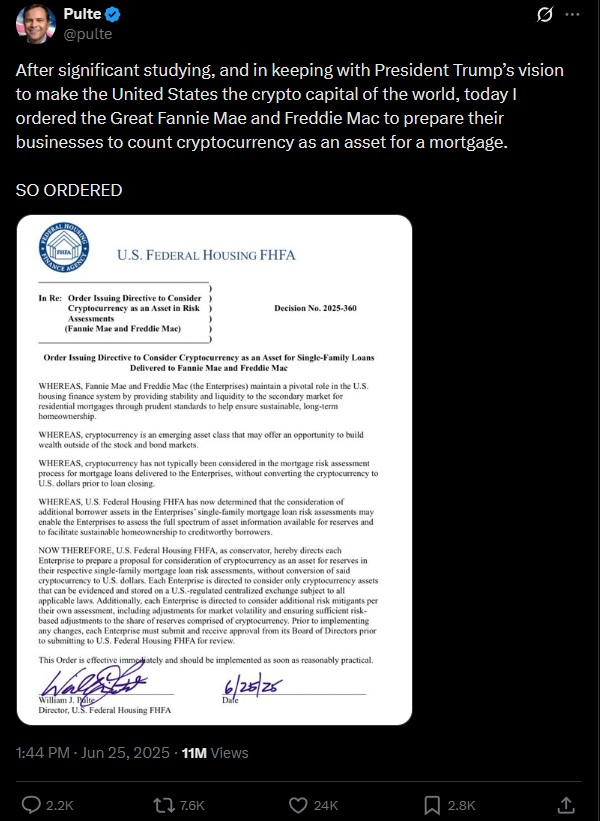

The policy actually came to be on June 25, 2025, in which the Federal Housing Finance Agency (FHFA) had Fannie Mae and Freddie Mac to allow crypto as an option when it comes to collateral for single-family mortgage risk assessments. The decision was made, in part, to align with US President Donald Trump’s crypto-focused policies. It ensured your crypto portfolio was a real part of your balance sheet.

This change matters because it brings crypto deeper into everyday finance, turning it from a store of wealth into an asset that can help support a home purchase.

Such a point is easy to miss, despite it being the most important angle. Crypto has often been sold as the future of finance, yet many holders still had to return to the old financial rails the moment they wanted to buy something in the real world. Housing is a clear example, but if crypto can help someone qualify for a home purchase without being sold first, it’s being given a more practical role than simple speculation.

The US director of Federal Housing on ordering Fannie Mae to accept crypto. Source: @pulte on X

Note that the FHFA did not say “bring your Bitcoin wallet and use it as direct mortgage collateral.” The change was about how lenders may look at borrower assets and reserves during your risk review.

With this implementation, think of your Bitcoin reserves as a bit of a backup cushion. They help show that you, as a borrower, can still make your mortgage payments after closing. Even if something goes wrong later, your reserves can help out.

Crypto-Backed Mortgages Offer Flexibility but Introduce New Risks

If you’re the right borrower, the benefits here are clear. You’ll be able to keep your crypto exposure instead of selling the moment you want to buy a home. This can help with taxes, timing, and peace of mind. In a market where buying a house has become harder, one where the median age of a first-time homebuyer went from 32 in 2000 to 40 in 2025, this kind of flexibility is vital.

But know that this change means you’re taking on more leverage than otherwise in the form of two loans. Managing two loans is no joke, and even if Better and Coinbase say there are no margin calls or top-up demands if Bitcoin falls, removing a common crypto-lending risk, the danger does not simply disappear.

If your payments go bad for long enough, the companies can liquidate your crypto, meaning you’re forced to sell later if you can’t uphold your side of the deal.

That risk is why this product will likely remain niche for now. Still, it offers a preview of how crypto may enter mainstream finance in the years ahead: not by replacing old systems, but by slowly fitting inside them.

What makes this crypto mortgage different from a normal mortgage?

It adds a second loan backed by crypto for the down payment, while the main mortgage stays a normal conforming home loan.

Does this mean buyers can use Bitcoin as direct mortgage collateral?

Not exactly. The draft makes clear that this is not a direct “bring your Bitcoin wallet” mortgage. Crypto is being considered within a more traditional lending structure.

Who is this product best suited for?

It appears aimed at long-time Bitcoin holders with high income, good credit, and enough crypto to support a home purchase without selling their position.

What is the biggest risk for buyers?

The main risk is taking on two loans at once. If payments go bad for long enough, the borrower’s pledged crypto can be liquidated.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Max Moeller is a Chicago‑based writer and video editor passionate about games, tech, and crypto. Whether it’s crafting clear, insightful articles or piecing together engaging video retrospectives, he’s driven by curiosity and takes pride in keeping things human. Since 2017, Max has been published in a variety of notable crypto magazines.

Easy

Easy