Real estate activity faces several underlying risks from the pandemic. The next domino to fall could be home values. | Image: REUTERS/Christinne Muschi

Share

The U.S. housing market has avoided the economic upheaval so far.

The recent spike in infections poses a cause for concern.

Dwindling home buyer confidence could weigh on the market.

The U.S. housing market has remained immune to the pandemic thanks to a short supply of residential properties and rising demand from people working from home.

Still, the housing market may not be out of the woods yet as the pandemic continues to surge across the country.

Ominous signs for the housing market emerge as virus cases spike

Low mortgage rates should ideally lead to an increase in mortgage applications, but that has not been the case over the past two weeks. For the week ending June 26, mortgage applications fell 1.8%, according to data from the Mortgage Bankers Association. This was the second consecutive weekly decline in mortgage applications even though rates were at an all-time low of 3.29%.

Mortgage applications have moved south for two weeks. | Source: TradingEconomics/Mortgage Bankers Association of America

This does not bode well for the U.S. housing market, which may have gotten ahead of itself despite the economic upheaval caused by the pandemic. Economists now believe that the fall in home prices may have been delayed instead of averted as the recent spike in infections is forcing potential buyers to have second thoughts.

Zillow reports that monthly home price growth slowed in May. The value of homes increased 4.3% year-over-year, a slight increase from April’s growth of 4.2%.

Prices rose even as the for-sale inventory of homes plunged 9.6% annually in May. Zillow estimates that home value growth could weaken further once the initial pent-up demand wanes and unemployment remains high.

Zillow’s senior principal economist Skylar Olsen pointed out that:

The next question housing will face is whether this growth can continue after demand built up during housing’s brief pause in the pandemic’s early days runs its course,” Zillow senior principal economist Skylar Olsen said in the report. “It’s likely housing will feel the broader economy’s downturn eventually, though to a mild degree, and home values will fall in the coming months.

More uncertainty ahead for home sales

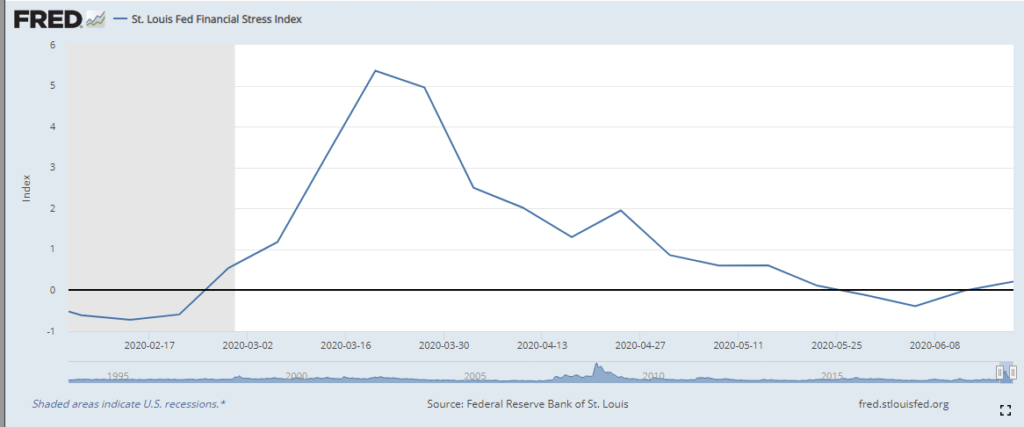

Uncertainty hovers over the housing market as several states reconsider their decision to reopen amid the new wave of infections. This could hurt home buying sentiment. The economy may take longer to get back on track in such a scenario.

Increasing financial stress could cause headwinds for the housing market. | Source: St. Louis Fed

The potential of mortgage defaults next year also remains high as 8.8% of all active mortgages have entered forbearance.

Actual defaults could lead to higher foreclosure activity, which would increase the housing market supply. If that happens and demand remains low, then the price gains seen of late could evaporate quickly.

Disclaimer: The opinions expressed in this article do not necessarily reflect the views of CCN.com.