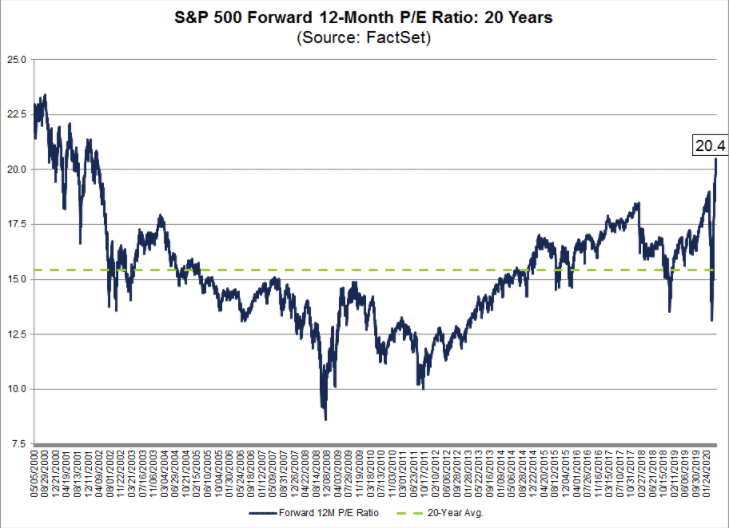

The S&P 500 forward 12-month P/E ratio is close to its 20-year peak. | Source: FactSet

This forward P/E ratio of 20.4 beat the five-year (16.7), the 10-year (15.1), the 15-year (14.6), and the 20-year (15.4) S&P 500 historical averages. The S&P 500 is not far from its 20-year peak of 23.4 recorded on September 1, 2000 (during the dot-com bubble).

The forward P/E ratio was only 13.1 on March 23, when the stock market hit bottom.

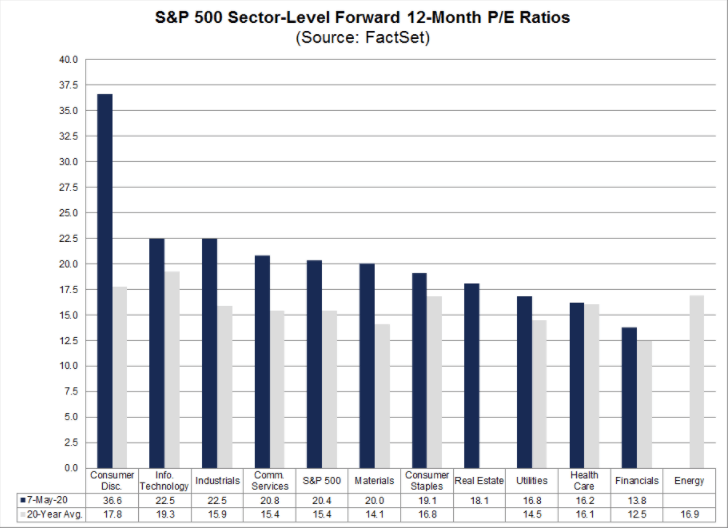

Nine sectors of the S&P 500 had forward 12-month P/E ratios exceeding their 20-year averages on May 7. | Source: FactSet

Nine of the S&P 500 sectors have forward P/E ratios above their 20-year averages. The forward P/E ratio of the Consumer Discretionary sector is the one that has the largest difference with its 20-year average (36.6 vs. 17.8).

Stocks Are Rising But Earnings Are Falling

Why has the forward P/E ratio risen so much? Since March 23, the price of the S&P 500 has increased by about 30%, while the forward 12-month EPS (earnings per share) estimate has decreased by 16%.

Thus, the P/E ratio has increased sharply because the “P” has increased while the “E” has decreased. This wide gap between price and earnings isn’t normal.

The price of the S&P 500 and future earnings estimates usually move in the same direction.

The Consumer Discretionary sector, with its forward P/E of 36.4, is the largest contributor to the S&P 500 high P/E ratio. This sector is only down about 3% year-to-date while the S&P 500 is down 10%.

Amazon (NASDAQ:AMZN) is the largest component in the Consumer Discretionary sector. This stock has a return of 27% year-to-date.

But companies are facing an uncertain outlook due to the COVID-19 impact.

Amazon’s revenue surged in Q1 as more customers shopped online, but earnings were lower than expected. In the second quarter, Amazon expects to spend about $4 billion on COVID-19 related expenses. This will hurt profit.

Many companies, including Facebook (NASDAQ:FB) and Apple (NASDAQ:AAPL), haven’t provided guidance for the second quarter or full-year 2020.

Investors Are Too Optimistic

No one knows how devastating COVID-19 will be for business, except that things will be ugly.

Companies are in a totally different environment than they were in three months ago when they gave full-year guidance. Management teams need to take the time to figure out what the impact will be. Even if they say earnings will be down 30%, that’s not really helping if it’s not right. They need to take a step back and assess the situation.

Companies’ earnings will drop in the coming months. We just don’t know to what extent.

In uncertain times like these, higher earnings expectations or lower valuations may be needed to keep equity markets supported. We err towards the latter.

It’s unlikely that profitability will surpass pre-coronavirus crisis levels in 2021. The impact of coronavirus on people’s behavior and the economy could last longer than we expect.

That optimism will cause another market crash, as stocks are just too expensive. The bubble is about to pop.

Disclaimer: This article represents the author’s opinion and should not be considered investment or trading advice from CCN.com. The author holds no investment position in any of the companies mentioned.

Stephanie has been writing about stocks and financial markets for several years. Based in Canada, she has written for The Motley Fool and Seeking Alpha. She received an MBA in finance and worked for the National Bank of Canada. Check out more of her experience on LinkedIn + and follow her on Twitter. Reach her at stephanie.chateauneuf (at) gmail.com.