Solana (BSOL) vs. Litecoin (LTCC) ETFs: Which One Could Supercharge Your Crypto Portfolio?

Share

Key Takeaways

USDe hits $5.7B with adoption growing as liquidity spreads across 23 chains via LayerZero.

USDe uses a delta-neutral strategy, maintaining parity and generating yield compared to DAI and FRAX.

It is resilient and avoids Luna’s collapse model but still relies on Ethereum’s liquidity.

Backed by institutions and cross-chain reach, USDe is rising as a competitor to DAI and FRAX.

Stablecoins have become a core part of decentralized finance, serving as digital dollars that anchor liquidity across exchanges, lending platforms and cross-chain protocols. Among them, a new category known as synthetic stablecoins has emerged, designed to maintain dollar value through financial engineering rather than fiat reserves.

Ethena is a blockchain protocol and development team focused on building synthetic stablecoins. Ethena’s synthetic dollar USDe has recorded $5.7 billion in total cross-chain volume (as of early August 2025), marking a large moment in the stablecoin sector.

ETHENA’S USDe SURPASSES $5.7B CROSS-CHAIN VOLUME, THIRD AMONG SYNTHETIC DOLLARS

Ethena’s USDe has reached $5.7 billion in total cross-chain transaction volume, securing the third spot by market cap among synthetic dollar assets.

This article focuses on what the milestone means for USDe and how it compares to other synthetic stablecoins such as DAI and FRAX.

What is USDe? The Rise of Synthetic Stablecoins

Synthetic stablecoins are digital assets designed to maintain parity with the US dollar without relying on fiat collateral reserves.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Unlike fiat-backed stablecoins such as USDt or USDC, synthetic stablecoins use derivatives, on-chain collateral and algorithmic strategies to stabilize value.

The appeal of synthetic stablecoins comes from the stablecoin’s ability to address limitations of fiat-backed models, including reliance on centralized custodians and banks, limited transparency around reserves, scalability constraints due to the need for fiat deposits, and vulnerability to regulatory restrictions or censorship.

Synthetic stablecoins address these issues by using on-chain collateral and decentralized mechanisms to maintain stability without depending on traditional financial institutions.

Key advantages include:

Capital efficiency: Value can be minted with less collateral locked compared to over-collateralized designs.

Decentralization: Stability is maintained through on-chain mechanisms rather than reliance on centralized banks.

Hedging strategies: Tools like derivatives and delta-neutral positions help sustain dollar parity.

The $5.7B cross-chain volume highlights the expanding reach of USDe across DeFi ecosystems. In practical terms, cross-chain volume refers to the total value of USDe transferred between different blockchains, a key indicator of both adoption and liquidity flow.

The $5.7B cross-chain volume figure demonstrates broad liquidity and transactional demand across multiple chains, underpinned by LayerZero interoperability, which connects USDe to 23 blockchain networks.

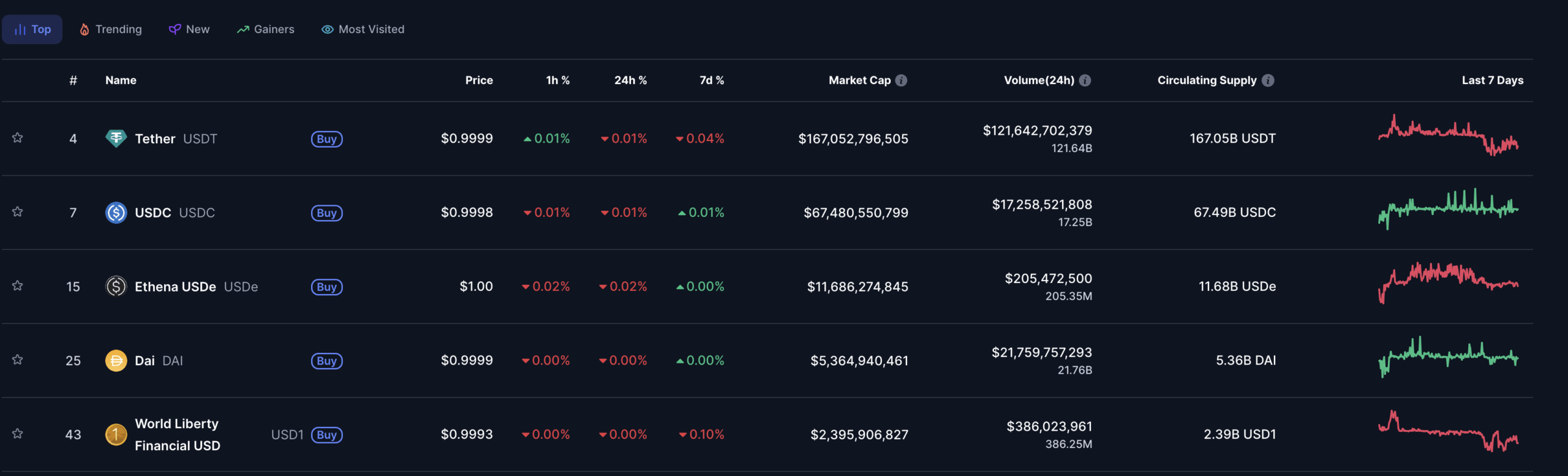

Largest Stablecoins by Market Cap | Source: Coinmarketcap

The market capitalization is of USDe is valued at $11.68 billion. Among synthetic stablecoins USDe presence stretches across numerous blockchains strengthening its utility on decentralized exchanges, lending protocols and liquidity pools. As of August 21, 2025, the top five stablecoins by market capitalization are:

Tether (USDT): Price $0.9999, Market Cap $167B, Volume (24h) $121.64B.

USDC (USDC): Price $0.9998, Market Cap $67.48B, Volume (24h) $17.25B.

Dai (DAI): Price $0.9999, Market Cap $5.36B, Volume (24h) $21.76B.

World Liberty Financial USD (USD1): Price $0.9993, Market Cap $2.39B, Volume (24h) $386.25M.

What Powers USDe’s Momentum

USDe is driven by a delta-neutral model, which uses long and short positions in crypto derivatives to offset volatility. In practice, being delta-neutral means the portfolio’s value doesn’t move much if the underlying crypto price rises or falls, since gains on one side (long or short) offset losses on the other.

This strategy preserves dollar parity while generating yield from market inefficiencies, a feature that separates USDe from traditional stablecoin models.

Institutional investment has also played a key role. Dragonfly Capital and Binance Labs have supported the ecosystem, providing credibility and access to liquidity networks. Recent inflows, including a $3.1 billion increase in circulating supply, illustrate rapid adoption that in some cases has outpaced traditional financial products such as ETFs.

DAI vs. FRAX vs. USDe: Key Differences Explained

Among the most discussed decentralized stablecoins today are DAI, FRAX and the newer USDe, each built on distinct mechanisms to maintain stability.

DAI: Launched by Sky (previously MakerDAO), DAI is backed by over-collateralized crypto assets, predominantly Ethereum. Its governance model allows decentralized risk management and it remains deeply integrated into lending protocols and liquidity pools.

FRAX: Built on a hybrid model, FRAX combines collateral with algorithmic adjustments to maintain its parity. This structure provides flexibility and efficiency but adds complexity compared to fully collateralized designs.

USDe: Positioned as a synthetic stablecoin, USDe’s delta-neutral hedging strategy offers broad cross-chain integration. USDe’s newer model contrasts with DAI’s established collateral base and FRAX’s hybrid mechanisms.

Features

DAI

FRAX

USDe

Launch

2017 (Sky)

2020 (Frax Finance)

2023 (Ethena)

Stability mechanism

Over-collateralized with crypto (mainly ETH)

Hybrid: partial collateral + algorithmic

Synthetic via delta-neutral hedging

Collateral base

Predominantly ETH, also USDC/other assets

Mix of USDC, crypto assets, and algorithmic

Crypto + derivatives (hedged positions)

Governance

MakerDAO decentralized governance

Frax governance (DAO with active treasury policies)

Protocol-driven with delta-neutral strategies

Strengths

Proven, transparent, DeFi deeply integrated

Flexible, capital-efficient, innovative hybrid

Scalable, cross-chain integration, reduces reliance on fiat

How USDe Differs From Terra Luna’s Failed Stablecoin Model

Terra’s UST failed because its peg was maintained solely through an algorithmic mint-and-burn mechanism with LUNA. When confidence in UST slipped, redemptions of UST for LUNA triggered hyperinflation in LUNA’s supply, collapsing the price and destroying the system’s ability to back UST, a reflexive “death spiral.”

USDe’s stability model stands apart from past failed experiments like Terra’s UST. Rather than relying on speculation, USDe is structured to remain market-neutral.

Why USDe avoids Luna’s pitfalls because:

No dependency on a paired token: Stability doesn’t hinge on continuous demand for a sister coin.

Delta-neutral hedging: Every long exposure is offset by an equal short in derivatives markets.

Resilience in volatility: The model is designed to hold stability even during sharp market swings.

Caveat – Ethereum dependency: Its effectiveness still relies on Ethereum’s deep liquidity and derivatives infrastructure. As long as Ethereum has deep spot and derivatives liquidity, the model should keep balance.

DeFi Impact: What USDe’s $5.7B Milestone Means for Liquidity

The expansion of USDe’s cross-chain activity is reshaping DeFi liquidity dynamics. By facilitating seamless transfers across 23 networks, USDe addresses liquidity fragmentation and improves capital efficiency for decentralized markets.

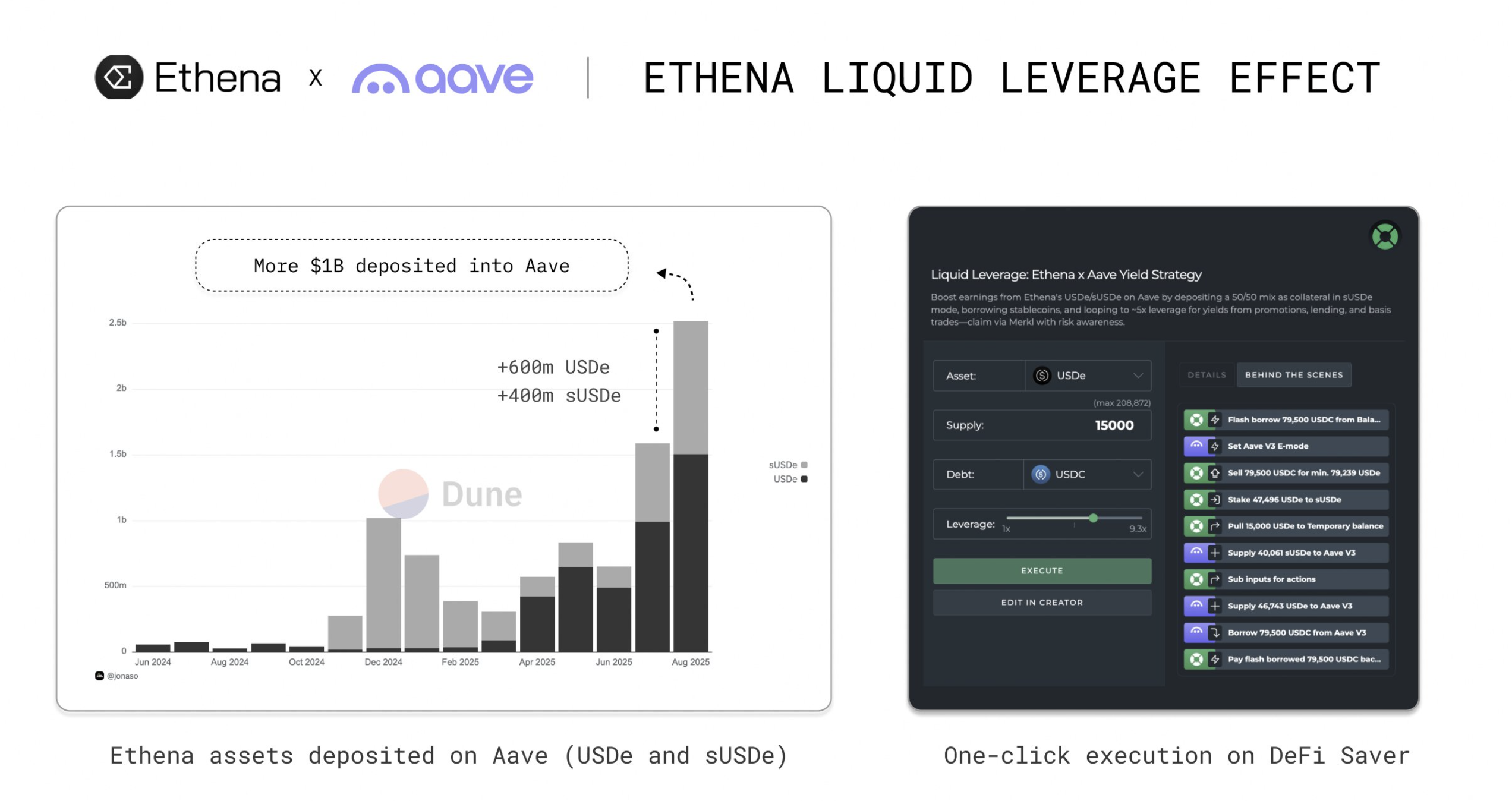

Ethena – Aave

Growing presence across major protocols such as Aave, Curve, and Uniswap highlights its composability, while increasing adoption may influence liquidity distribution traditionally dominated by DAI and FRAX. The milestone reinforces the competitive role of synthetic stablecoins in multi-chain DeFi ecosystems.

Challenges Ahead for USDe in 2025 and Beyond

Despite strong momentum, synthetic stablecoins are likely to face mounting regulatory pressure in both the United States and Europe. Regulations such as the GENIUS Act and MiCA are setting stricter standards around transparency, reserve management and governance.

For USDe, long-term sustainability will hinge on strengthening smart contract security, driving steady adoption and expanding utility through features like yield generation and deeper DeFi integrations.

As the broader stablecoin sector matures, USDe’s ability to remain resilient in the face of regulatory shifts and market volatility will be a defining test.

GENIUS Act (U.S.) – Passed in 2025

The U.S. has introduced its first federal stablecoin law, reshaping how issuers can operate:

Issuer restrictions: Only licensed banks or OCC-approved entities can issue stablecoins.

Reserve rules: Coins must be fully backed 1:1 with cash or high-quality liquid assets such as U.S. Treasuries.

Ban on yield: Stablecoin issuers cannot pay interest or offer yield on holdings.

Consumer protection: In insolvency, stablecoin holders are prioritized in recovery.

Impact on USDe:

Its synthetic, delta-neutral design doesn’t match the 1:1 reserve rule.

Yield mechanisms, one of USDe’s growth drivers, would not be allowed.

Without a licensed issuer, USDe risks exclusion from the U.S. market

MiCA (EU) – In Force Since Late 2024

Europe’s MiCA framework sets out clear rules for stablecoin providers:

Reserve requirement: Stablecoins must hold equivalent fiat reserves with strict disclosure.

Governance standards: Issuers must maintain robust risk, compliance, and complaints systems.

Significance tests: Large or widely used tokens face extra obligations, including stress testing.

Its synthetic model may not qualify as a compliant stablecoin under MiCA.

Without fiat reserves, it could be barred from operating in the EU.

European adoption will likely remain limited unless the model adapts.

Can USDe Outpace DAI and FRAX?

DAI remains a battle-tested stablecoin with deep DeFi integration.

FRAX, a stablecoin that uses a hybrid model of partial collateralization and algorithmic mechanisms to maintain its dollar parity innovates through a hybrid design and dynamic collateral mechanisms.

USDe, brings a synthetic, delta-neutral model combined with cross-chain reach and institutional partnerships.

However, USDe’s fast growth has positioned it as a strong contender among decentralized stablecoins, but whether it can surpass established players like DAI and FRAX depends on several factors.

Innovation edge: USDe’s delta-neutral synthetic model allows it to scale beyond the collateral constraints of DAI and offers broader cross-chain reach compared to FRAX’s hybrid system. This gives it a potential efficiency and flexibility advantage.

Regulatory headwinds: Unlike DAI’s over-collateralized model or FRAX’s partially fiat-backed reserves, USDe faces steeper challenges aligning with new rules such as the GENIUS Act and MiCA, which heavily favor fiat-backed stablecoins.

Trust & adoption: DAI has the longest track record and deep DeFi integrations, while FRAX has proven its adaptability through its hybrid design. USDe, as a newcomer, must build similar trust while expanding integrations and proving resilience under stress.

Yield & utility: One of USDe’s unique draws has been yield opportunities through hedging strategies. If regulatory restrictions ban yield, USDe will need to pivot toward other value propositions like liquidity depth, cross-chain usage, or novel DeFi features.

USDe could outpace DAI and FRAX in growth if it successfully scales and adapts to regulation, but its long-term lead will depend on whether it can combine innovation with compliance and sustain user trust.

Conclusion

USDe’s $5.7B cross-chain volume milestone underscores the rapid ascent of synthetic stablecoins within DeFi. With a delta-neutral structure, multi-chain reach, and institutional support, it has emerged as a competitive player next to DAI and FRAX.

The trajectory of synthetic stablecoins will continue to shape how DeFi manages liquidity, capital efficiency, and decentralized access to stable dollar exposure.

However, users should approach with caution. Synthetic models remain less battle-tested than over-collateralized or hybrid designs, and their reliance on derivatives and hedging strategies introduces layers of counterparty and market risk.

Regulatory frameworks like the GENIUS Act in the U.S. and MiCA in Europe further raise uncertainty around long-term viability, particularly if yield and synthetic structures are restricted. So thor resilience under stress and compliance with evolving regulation will ultimately determine whether USDe’s growth is sustainable.

How does USDe maintain price stability compared to DAI and FRAX?

USDe uses a delta-neutral derivatives strategy, hedging against volatility to keep its peg, while DAI relies on crypto-collateral reserves and FRAX on a hybrid algorithmic-collateral model. This distinction affects their resilience under market stress.

Why is USDe’s $5.7B cross-chain volume a critical milestone for DeFi?

Cross-chain volume reflects real adoption and liquidity mobility. With USDe available on 23 blockchain networks, it showcases unmatched interoperability, positioning it as a serious competitor to DAI and FRAX in DeFi liquidity markets.

Can USDe’s synthetic model handle black swan events better than traditional stablecoins?

Unlike fiat-backed coins, USDe’s derivatives-based design may either absorb shocks effectively or amplify risks if derivative markets destabilize. This is a key debate compared to DAI’s overcollateralization and FRAX’s partial collateral approach.

What makes USDe’s interoperability across 23 chains more significant than DAI or FRAX integrations?

USDe’s LayerZero cross-chain infrastructure allows near-instant movement of value across blockchains, while DAI and FRAX often face liquidity fragmentation. This interoperability boosts capital efficiency and trading opportunities.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Andrew Kamsky is a chart analyst and writer with a background in economics and ACCA certification. He has held roles at a Big Four firm, a fintech bank, and a listed bank specializing in currency hedging. His work explores Bitcoin, macro trends, and market structure. Outside finance, he's passionate about music, travel, and neon design.

Easy

Easy