Poland’s Bill 1424: Strengthening Oversight and Innovation in the Crypto Market| Credit: Veronica Cestari /CCN

Share

Key Takeaways

Bill 1424 introduces stricter national measures than the EU’s MiCA, shifting Poland’s crypto sector under KNF control.

The law replaces simple registration with full licensing, supervision, and penalties for non-compliance.

Exchanges face higher costs, while users gain more protection and transparency.

Political debate continues over whether the bill promotes stability or limits innovation.

Europe might appear to be a unified region regarding regulation, especially under the framework of the European Union.

However, crypto laws are not always harmonized across borders. While many countries adopt similar principles, some, such as Germany and France, have added national requirements, and others, like Poland, are choosing to expand or tighten certain provisions to address local market conditions.

Poland’s crypto landscape is reaching a turning point. By 2026, it is expected to have more than 7.67 million users and market revenue of around $1.3 billion, positioning the country as a major player in Europe’s digital asset space.

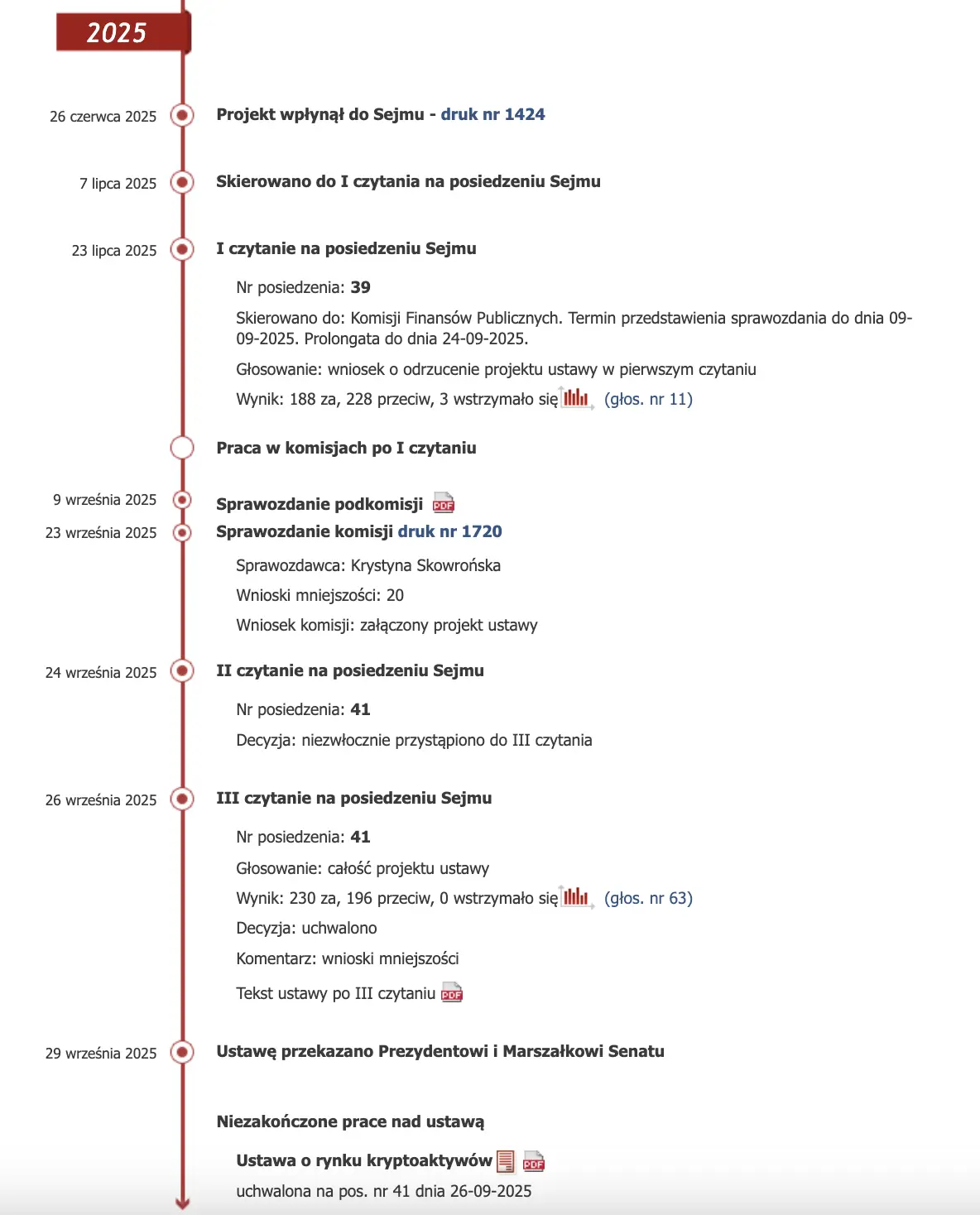

Yet, the recent passage of Bill 1424, known as the Crypto-Asset Market Act, threatens to add complexity and new restrictions. Poland’s lower house, the Sejm, approved it on September 26, 2025, with a narrow 230–196 vote.

The bill largely mirrors the EU’s Markets in Crypto-Assets (MiCA) regulation. Still, it includes 118 pages of stricter domestic measures, aiming to “in particular in the field of effective supervision and investor protection.”

The Polish Senate will review the crypto regulation proposal in the coming weeks. In the meantime, it has raised concerns in Poland’s crypto community about potential overregulation, which could stifle market growth.

Zondacrypto CEO, Przemysław Kral described Bill 1424 as “a major step backwards, and a prime example of overregulation.” He warned that while the EU’s MiCA offers “a clear and balanced rulebook for crypto,” Poland’s interpretation “has taken it too far” and risks “treating crypto as a threat rather than an opportunity.”

According to Kral, the legislation could “criminalise basic activities like smart contract development,” forcing companies to relocate abroad and taking jobs and tax revenue with them.

This article explains Bill 1424’s core provisions, its potential impact on exchanges, users, and blockchain innovation, and why it could either end Poland’s so-called “Wild West” crypto era or trigger an exodus of local developers and startups.

What Bill 1424 Says About Poland’s Crypto Regulation

The Polish Bill 1424 expands on the MiCA regulation and related EU laws. It aims to ensure full application while adding stricter national measures.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Before this law, oversight was limited to the Register of Virtual Currency Activities, managed by the Tax Administration Chamber in Katowice. Created in 2021, it served as Poland’s first step toward identifying businesses involved in virtual currency services.

Bill 1424 replaces the basic registry model with full supervision by the Polish Financial Supervision Authority (KNF, Komisja Nadzoru Finansowego), turning simple registration into a licensing and enforcement system.

The main elements include the following:

Centralized regulatory oversight: The KNF becomes the main body supervising the entire crypto market.

Licensing requirements: To operate legally in Poland, all crypto-asset service providers (CASPs) must obtain a KNF-issued license.

Detailed operational and AML requirements: Licensing depends on submitting complete documentation that outlines a company’s corporate structure, capital adequacy, internal controls, risk management policies, and Anti-Money Laundering (AML) procedures.

Mandatory supervisory fee: CASPs will be required to pay the KNF an annual supervisory fee, estimated at around 0.4% to 0.5% of annual revenue from crypto services. Critics say the fee creates a serious barrier for smaller operators.

Sanctions for non-compliance: Fines can reach PLN 10 million (about $2.5 million USD) for unlicensed activity or illegal token issuance, with up to two years of imprisonment in severe cases.

Register of dishonest domains: The KNF can create a list of websites and IP addresses linked to illegal crypto activities and block access to them.

Extension to traditional currency exchanges: Online exchange offices, known as kantory internetowe, now fall under KNF supervision. They must maintain separate client accounts to protect users’ funds.

Short transitional period: Once the law takes effect, existing CASPs have a six-month window to apply for the new KNF license.

Together, these measures reshape Poland’s crypto landscape, setting a new framework that could redefine how exchanges and users interact with digital assets.

How Poland’s New Crypto Rules Impact Exchanges and Users

Bill 1424 framework reshapes how exchanges operate and users engage with digital assets, tightening oversight while changing the market’s balance between innovation and protection.

Impact on Exchanges and Service Providers

The law raises entry barriers and legitimizes compliant firms, creating pressure and opportunity within Poland’s market.

Fewer players, stronger survivors: The combined effect of licensing costs and annual supervisory fees could force smaller exchanges to exit, leaving a landscape dominated by larger, better-funded companies.

Operational transformation: To meet KNF standards, firms must upgrade internal governance, cybersecurity systems, and financial transparency, replacing the simpler procedures that existed before.

Pathway to EU expansion: Businesses that secure KNF approval can operate across the European Union under MiCA, offering a route to cross-border growth and partnership.

Restored credibility: Meeting KNF’s AML expectations may help exchanges rebuild relationships with Polish banks, improving access to traditional financial services.

Kral argued that such costs and procedures “make it much harder for new crypto companies to launch in Poland, meaning the existing giants will continue to dominate the market.” He added that even established exchanges are reconsidering expansion plans under the new framework.

Impact on Users and Investors

For users, Bill 1424 means more security and transparency, but it can also mean less variety in trading options.

Higher protection standards: Only licensed platforms can serve users, which minimizes fraud risks and ensures the separation of client and company funds.

Stronger accountability: Every new token launch requires a transparent white paper outlining risks, with clear legal responsibility for misinformation.

Proactive anti-fraud defense: The KNF’s authority to block fraudulent domains curbs scam exposure and builds user confidence in the regulated market.

Limited choice, higher trust: The disappearance of smaller exchanges may reduce options, but investors gain access to a safer, more transparent environment.

Despite being founded in Poland, Zondacrypto operates under Estonian regulation, where it “pays over €6 million in VAT annually.” Kral pointed to this as evidence that “friendlier markets attract sustainable growth,” suggesting that Poland’s policies could drive businesses and talent elsewhere.

Poland’s Crypto Law vs. MiCA: Key Differences Explained

The table below outlines how Poland’s domestic version compares with MiCA, which addresses why it might be considered a restrictive interpretation of the EU framework.

Features

MiCA (EU Regulation)

Polish Act on the Crypto-Asset Market (Draft)

Nature of law

Directly applicable EU regulation (baseline)

National law implementing and exceeding MiCA standards

Maximum fines

Administrative fines set by national laws

Administrative fines up to €15 million ($17.5 million)

Criminal liability

Permitted but not mandatory

Explicitly introduces criminal penalties for breaches

Prison sentences

Not specified in MiCA

Up to two years for serious violations

Enforcement powers

National competent authority (e.g., KNF)

Extended powers to freeze assets and block domains

Liability scope

Covers actual losses from misrepresentation

Expands to include lost profits and indirect damage

These differences highlight how Poland’s version of MiCA adds extra layers of control that could either stabilize the market or discourage smaller players from operating locally.

Kral’s criticism echoes broader fears in the industry that “overregulation will push innovation abroad.” He emphasized that while “regulation is necessary for consumer protection, it can be counterproductive” when taken too far.

As lawmakers and industry groups debate these changes, attention has shifted from technical compliance to broader questions about Poland’s direction in digital innovation.

The next stage of discussion centers on how politics, regulation, and market confidence will shape the country’s crypto future.

The debate over Poland’s digital future has intensified following Bill 1424’s approval. Opposition figures, including MP Janusz Kowalski, accuse the government of pushing an excessively restrictive framework that could undermine the country’s role in Europe’s crypto economy.

In a post shared on X, Kowalski warned that the Civic Platform’s policy risks “destroying” the domestic market and penalizing innovators, arguing that Poland’s 118-page proposal far exceeds the length and scope of MiCA implementations in other EU states.

He said the opposition plans to introduce an alternative bill aimed at promoting innovation while keeping Poland aligned with European standards.

Janusz Kowalski statement | Source: X

This sentiment is shared by several industry voices. As Kral summarized, “Poland has taken it too far and its domestic crypto industry will suffer as a result.” His remarks capture a growing divide between policymakers seeking strict control and innovators warning of a lost opportunity for leadership in the European market.

The coming months will determine whether Poland positions itself as a competitive force in Europe’s regulated digital economy or risks falling behind more innovation-friendly neighbors.

Much will depend on how the Senate approaches Bill 1424, whether amendments address market concerns, and how effectively authorities balance supervision with growth.

For Poland’s crypto holders, the outcome could redefine many of the main elements that shape the future of the country’s digital finance sector.

Conclusion

Poland’s Crypto-Asset Market Act reflects a decisive shift toward regulatory control in a sector that has long operated with minimal oversight. By bringing exchanges and service providers under the KNF, the government aims to strengthen supervision and investor protection, aligning with the European Union’s MiCA framework.

However, the law’s extensive requirements have divided opinion. Supporters argue that it will enhance trust and attract institutional confidence, while critics warn it could stifle competition and push innovation abroad. The balance between compliance and growth will depend on how the Senate refines the legislation and how quickly businesses can adapt.

As Poland positions itself within Europe’s digital economy, the coming months will reveal whether Bill 1424 can secure a safer crypto market in comparison to other jurisdictions.

After Senate approval, exchanges will have six months to apply for a KNF license once the law becomes effective.

Who oversees crypto activities under the new law?

The Polish Financial Supervision Authority (KNF) is now the main regulator overseeing all crypto operations in Poland.

What happens to unlicensed crypto operators?

Firms operating without KNF authorization risk fines up to PLN 10 million and potential imprisonment for serious breaches.

How could Bill 1424 impact Polish crypto users?

Users may see fewer exchange options but gain stronger protections, clearer accountability, and reduced exposure to fraud.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Lorena Nessi is an award-winning journalist and media technology expert with 15 years of experience in digital culture and communication. Based in Oxfordshire, UK, she combines academic insight with hands-on media practice.

She holds a PhD in Communication, Sociology, and Digital Cultures, and an MA in Globalization, Identity, and Technology.

Lorena has taught at Fairleigh Dickinson University, Nottingham Trent University, and the University of Oxford. She is a former producer for the BBC in London, with additional experience creating television content in Mexico and Japan.

Her research focuses on digital cultures, social media, technology, capitalism, and the societal impact of blockchain innovation.

She has written extensively on digital media and emerging technologies, with her work featured in both academic and media platforms. Her Web3 expertise explores how blockchain technologies shape culture, economics, and decentralized systems.

Outside of work, Lorena enjoys reading science fiction, playing strategic board games, traveling, and chasing adventures that get her heart racing. A perfect day ends with a relaxing spa and a good family meal.

Easy

Easy