Meta Eyes Stablecoin Payments Across WhatsApp, Instagram, and Facebook — Why It Matters for 3 Billion+ Users

Share

Key Takeaways

In order to avoid the regulatory issues that plagued its previous Libra project, Meta intends to implement dollar-pegged stablecoin payments through third-party companies like Stripe.

By targeting Meta’s over 3.5B daily active users, the integration aims to facilitate cross-border payments and creator compensation.

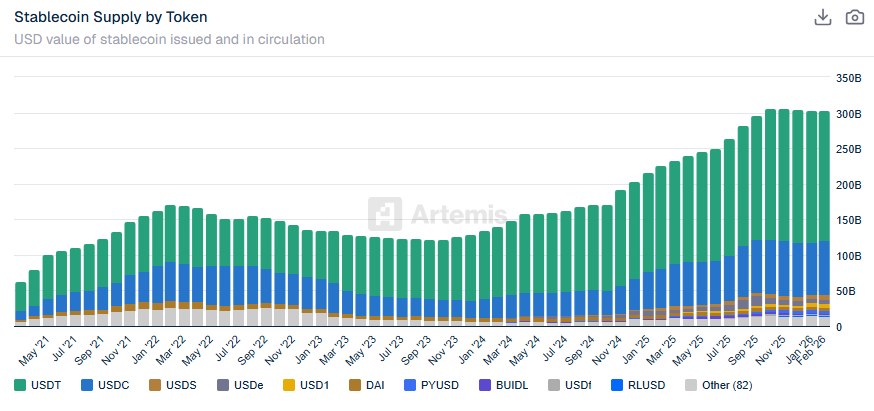

With the industry currently valued at more than $300B, the 2025 GENIUS Act could accelerate the adoption of stablecoins.

Although it promises quicker and less expensive payments, it also raises concerns about financial stability, competition, and privacy in a changing regulatory landscape.

In the second half of 2026, Meta Platforms, the company behind Facebook, Instagram, and WhatsApp, is reportedly planning to include stablecoin payments into all of its apps. This move has the potential to impact how over 3B people transmit money, pay creators, and shop online.

But why now, years after a failed attempt? And how could this adoption affect regular users and the larger crypto community?

What Went Wrong with Meta and Libra?

It’s not the first time Meta has ventured into digital payments. Back in 2019, the business introduced Libra, a blockchain-based stablecoin, with the goal of developing a global payment system that would be connected to its social media platforms. Libra was envisioned as a reserve-backed basket of currencies that would make money transfers as simple as sending a Facebook or WhatsApp message.

But regulators were not on board. Back then, there were several concerns about data privacy, monetary sovereignty, and the possibility of criminal financing that were voiced by lawmakers in the U.S. and Europe. Mark Zuckerberg testified before Congress, answering questions about Facebook’s handling of user data.

Libra, eventually, rebranded as Diem in 2020 and cut back to a single US dollar peg, selling its intellectual property to Silvergate. The project has never launched and Meta appeared to be “out” of the crypto game.

Yet, Meta’s failure boosted innovation in other areas like the development and integration of the Move programming language into the Web3 space.

BREAKING: Meta is said to be bringing stablecoin payments to Instagram, WhatsApp, and Facebook.

They're reported to have just sent out an RFP for stablecoin payment infrastructure.

Translation: they’re quietly shopping for a third-party partner to help launch stablecoin… https://t.co/C4yhH7n5DD

Why dust off this idea after such a setback? Timing is everything.

Stablecoins are now a $300B market, but above all, the GENIUS Act, which President Trump signed into law in July 2025, provides more regulatory clarity. Safer adoption was made possible by this government framework, which defines “payment stablecoins,” mandates 1:1 reserves with premium assets like Treasurys, and establishes AML regulations.

Instead, it is collaborating with other issuers to integrate already-existing stablecoins like USDT or USDC. Stripe enters as a key player, reinforced by its $1.1B acquisition of Bridge in 2024 and the appointment of CEO Patrick Collison to Meta’s board in 2025. The scrutiny that killed Diem is now avoided by adopting this “arm’s length” approach. According to reports, Meta has sent out requests for proposals (RFPs) to vendors, with the goal of developing a new wallet for seamless transactions. The goal? To enable quick cross-border sends and reduce creator payout costs.

Stablecoins supply graph | Source: Artemis

Why Stripe and Third-Parties Matter for Meta

Stripe recently made news by reinstating crypto payments for merchants, with a focus on USDC. By tapping into Stripe’s infrastructure, Meta avoids the need to handle the intricate plumbing of compliance and liquidity on their own. With this “plug-and-play” strategy, Meta can concentrate on the user experience while authorised payment processors and custodians manage the regulatory burden. Could this be the “golden ticket” for wide adoption? Users may not even be aware that they are using a stablecoin when they purchase something on Instagram.

How Stablecoin Payments Could Work on Meta’s Platforms

Although the exact functionalities are still to be announced in detail, the system is expected to operate as a “crypto-lite” experience in which Meta’s apps serve as an intuitive custodial wallet interface. Users are likely to send stablecoins as simply as a text message rather than having to manage complicated private keys, with a partner like Stripe taking care of the conversion from physical cash to tokens.

Implications for Users and the Crypto Market

For users, this implies faster and cheaper money transfers that settle in seconds and avoid wire fees or foreign exchange rates. Meta’s scale has the potential to introduce billions of people to crypto without their knowledge, hence increasing acceptance.

Stablecoins are already used 67% for DeFi/trading, 15% for remittances. Here, Meta’s entry competes with X (formerly Twitter) and Telegram, turning social apps into “super apps.” It might fuel AI-driven commerce, where bots transact autonomously. But benefits come with trade-offs. Who wins? Users in high-inflation areas hedging with dollar-pegged assets. Who loses? Traditional banks facing deposit outflows.

Regulatory Hurdles: Can Meta Avoid Past Mistakes?

The route isn’t totally obvious, despite the excitement. Meta’s data privacy record has continued to raise concerns among regulators in the EU and the United States. Many privacy advocates consider the combination of financial and social media data to be a “red flag”.

In addition, the Markets in Crypto-Assets (MiCA) framework in Europe has established strict requirements for stablecoin issuers. Overall, Meta describes this as an “integration” of modern fintech, not a “relaunch” of a failed crypto project.

Will regulators play ball this time? By using third-party partners like Stripe or Paxos, Meta can argue that they aren’t the ones “issuing” the money, merely providing the “browser” to view and move it. This distinction could be their saving grace.

According to current reports, the launch is expected in the second half (H2) of 2026.

Which stablecoin will Meta use?

Through partners like Stripe, Meta is anticipated to support well-known, regulated stablecoins, though the details have not been confirmed.

What is the GENIUS Act?

A federal framework for stablecoins is provided under the 2025 law, which mandates reserves and AML compliance to promote safe growth.

Why did Meta's previous project fail?

Libra, rebranded as Diem, was halted due to regulatory pushback over privacy and financial stability concerns, resulting in its termination in 2022.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Curious about how technology and crypto reshape global finance, Elizaveta Savenko explores blockchain, AI, decentralized systems, their applications, and regulatory requirements. She contributes to research, educational initiatives, and industry collaborations, examining trends in digital assets and fintech innovation, increasing awareness of the crypto space and its impact on financial systems.

Easy

Easy