‘Bitcoin Is Not Crypto’: Jack Dorsey’s Bold Claim and What It Really Means

Share

Key Takeaways

Bitcoin’s design targets money, while most other cryptocurrencies focus on programmable applications.

BTC meets parts of the monetary definition today but still falls short in others.

In policy terms, the IRS classifies Bitcoin as property, and central banks remain skeptical of its monetary role.

Meanwhile, real-world payments are expanding through the Lightning Network and instant fiat conversion tools, rather than direct on-chain transactions.

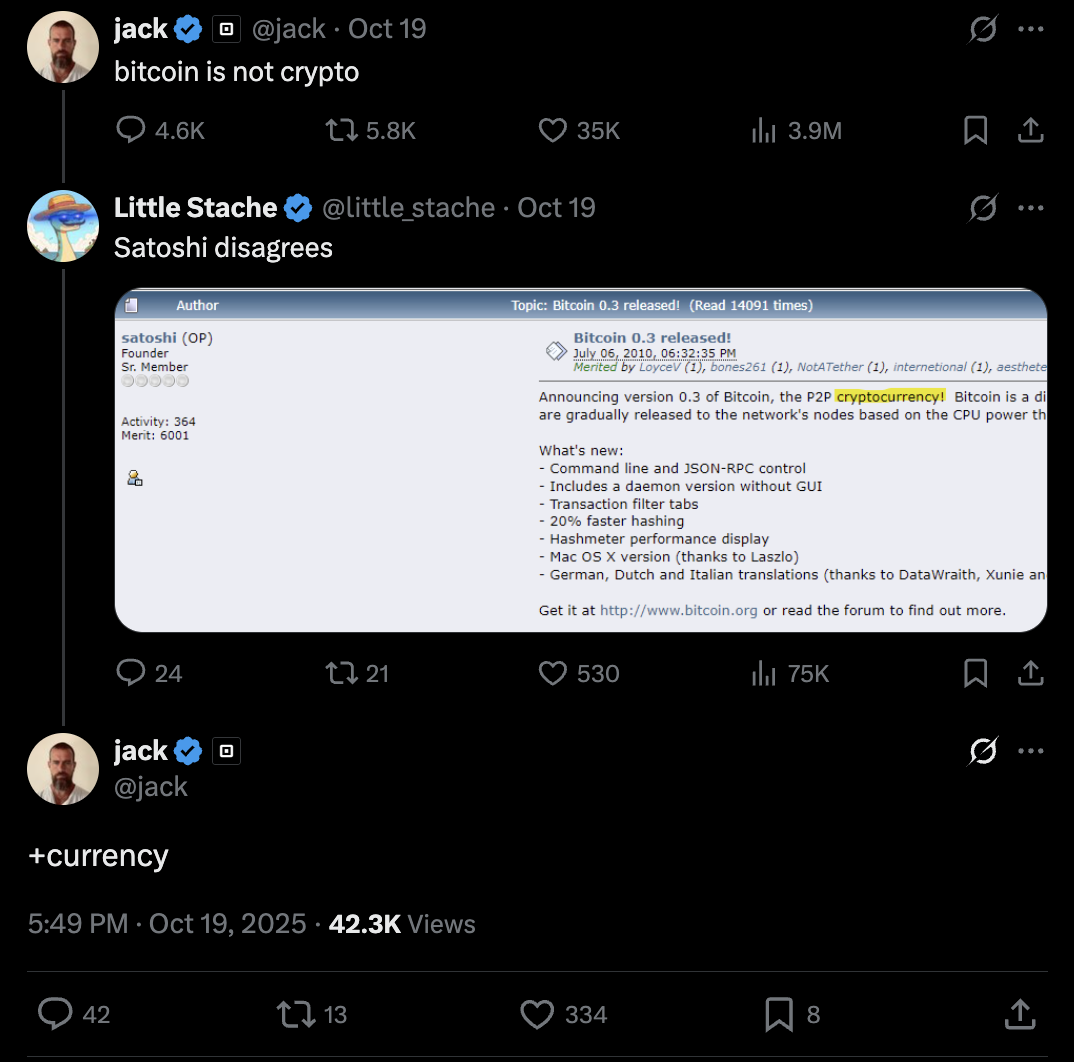

On Oct. 19, 2025, Twitter (now X) and Block (formerly Square) co-founder Jack Dorsey, the rumored Satoshi, posted a blunt phrase on X: “bitcoin is money.” Dorsey posted this in response to a post about a Bitcoin-powered ice cream sale, and the merchant’s note about potential zero processing fees.

Source: @jack on X

The Bitcoin enthusiast continued in a later post, “bitcoin is not crypto.” Dorsey’s bluntness predictably generated a slew of discourse on either side of the matter, but his core claim is clear: Bitcoin stands apart from the rest of the digital asset space because of its design, governance, and real-world, prevalent use case as a form of money.

This article translates Dorsey’s provocations into plain English, then tests them against real-world evidence.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Jack Dorsey’s Bitcoin Argument: The Only True Form of Digital Money?

When people say “crypto,” they’re often describing a universe of digital assets with diverse purposes: smart-contract platforms like Ethereum or Solana, stablecoins, governance tokens, memecoins, and everything in between.

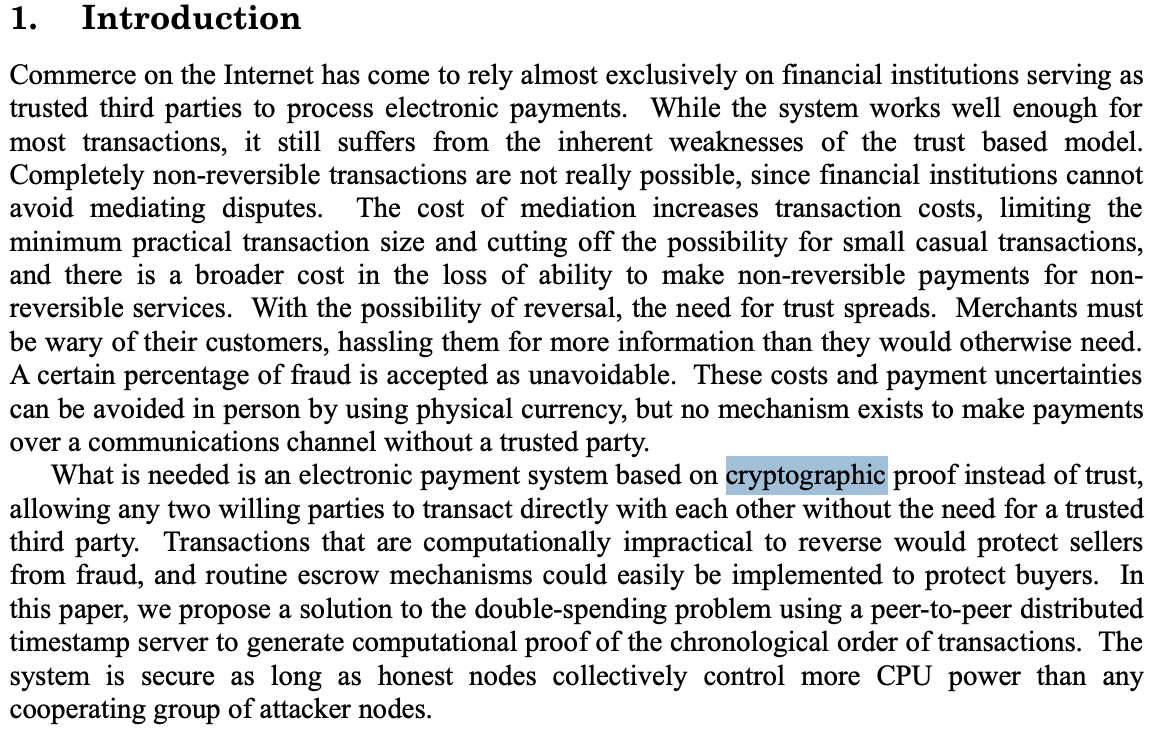

Bitcoin, in contrast, is the world’s first cryptocurrency, launched in 2009 with one job description: peer-to-peer electronic cash, or money you can send online without a central intermediary. In fact, the whitepaper’s first sentence describes just that.

Pair this with the Federal Reserve’s definition of money, as detailed in then-Governor Lael Brainard’s speech on digital currencies and stablecoins back in 2019.

Brainard defined money as serving three functions:

As a medium of exchange

As a store of value, and

As a common unit of account

Dorsey seems to imply that Bitcoin hits those core functions more cleanly than the rest of crypto, due to its fixed supply, rule-based issuance, and majority-based ruleset. That regardless of where you stand, Bitcoin is arguably the closest digital asset to functioning as money that exists.

Source: @jack on X

Bitcoin’s policy is famously simple: a maximum of 21 million BTC, and an issuance schedule that halves around every four years. No entity can “mint” more Bitcoin as it wishes. That 21 million cap is integral to Bitcoin’s code and culture.

Essentially, Dorsey claims that Bitcoin, and Bitcoin alone, is the direct evolution of money as you know it, not just another cryptocurrency as the rest of the world defines it.

The Bitcoin whitepaper seems to reinforce this, not even using the term “cryptocurrency.” The word “crypto” only appears once in the entire document, as part of “cryptographic proof.”

Source: The Bitcoin Whitepaper

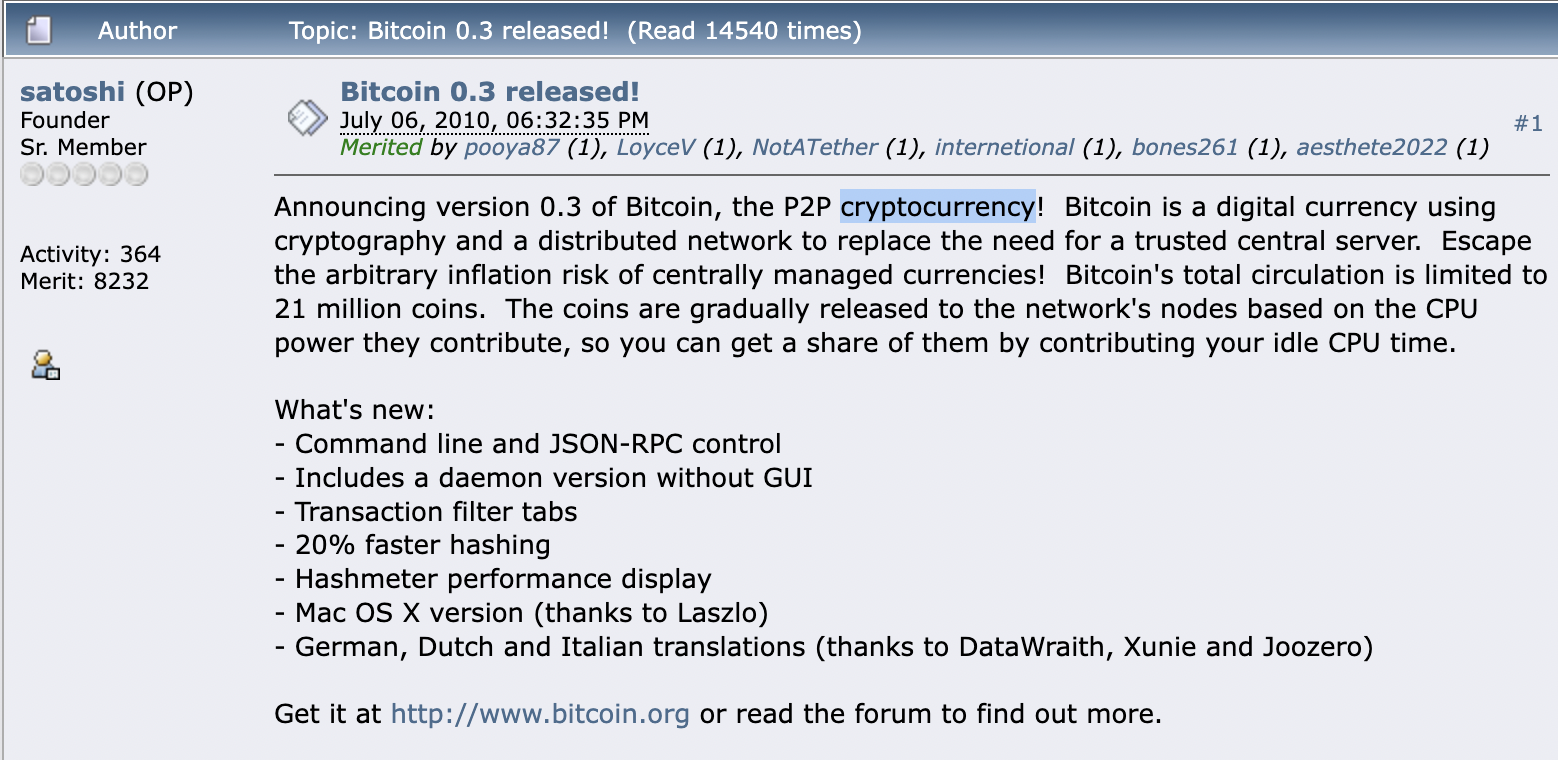

However, Satoshi refers to Bitcoin as a cryptocurrency in a 2010 Bitcointalk post, so it’s possible they apply the term retroactively. Some even argue that Dorsey himself is the rumoured Satoshi Nakamoto, though inconsistencies arise if you dig beyond the theory’s surface.

Source: Bitcointalk

Examples: Does Bitcoin Currently Function as Money?

Of course, you can test Bitcoin’s existence as money against Brainard’s definition.

Medium of Exchange

El Salvador controversially declared Bitcoin as legal tender in 2021, requiring all entities to accept the digital asset as a method of transaction alongside the U.S. dollar. Citizens could even pay taxes using the digital asset.

However, El Salvador’s Congress modified the framework in February 2025 due to troubled adoption and pressure from the International Money Fund (IMF). Bitcoin is still legal tender, but the government lightened mandatory acceptance and taxes are no longer payable in BTC. It still seeks to buy and hold Bitcoin.

Dorsey’s Cash App, on the other hand, facilitates Bitcoin transactions, with about 62% of its 2024 revenue tied to Bitcoin transactions.

Store of Value

Bitcoin’s potential as a store of value is continuously under debate. While the asset’s fixed supply and predictable halvings lend credence to the “digital gold” narrative, its volatile nature and the continued push toward spending avenues say otherwise.

If you can’t buy groceries with physical gold, why should you with its digital counterpart?

Even so, the Securities and Exchange Commission’s (SEC) approval of spot Bitcoin ETFs in 2024 helped legitimize the asset in the eyes of the mainstream.

Furthermore, a report by Fidelity Digital Assets titled “Bitcoin as an Aspirational Store of Value Revisited” argues that Bitcoin has many of the ingredients to be considered a store of value: fixed supply, predictable issuance schedule, digital, decentralized.

However, a study on Bitcoin’s volatility finds that its price swings are “extreme and almost 10 times higher than the volatility of major exchange rates”, and this excess volatility “adversely affects its potential role … as a store of value.”

Unit of Account

Understandably, most prices worldwide are set in fiat. Even in El Salvador, pricing habits remain dollar-centric. It’s hard to set price points for a volatile currency, after all.

However, there’s a growing amount of purchasing options that instantly convert Bitcoin to fiat at checkout, including PayPal.

The unit of account is certainly Bitcoin’s “weakest” money function, at least for now.

Researchers note that until Bitcoin achieves relative price stability and broader accounting integration, it will remain a speculative asset and medium of exchange, not a consistent unit of account.

Bitcoin’s Ongoing Identity Debate: Is It Crypto, Money, Property, or Philosophy?

All this to say, Dorsey’s argument is functionally correct. Bitcoin is money in the sense that it can function as a way to exchange value between two parties.

But if regulators fail to treat Bitcoin as such, does it really matter if the world views it as traditional money or an evolution of it?

Even as the SEC validated Bitcoin via its approval of spot ETFs, the European Central Bank denounced the asset, stating: “the latest approval of an ETF doesn’t change the fact that Bitcoin is not suitable as means of payment or as an investment.”

There’s also the fact that the Internal Revenue Service (IRS) classifies digital assets, including Bitcoin, as property, not a currency. Spending Bitcoin requires you to calculate a gain or a loss, unlike spending dollars.

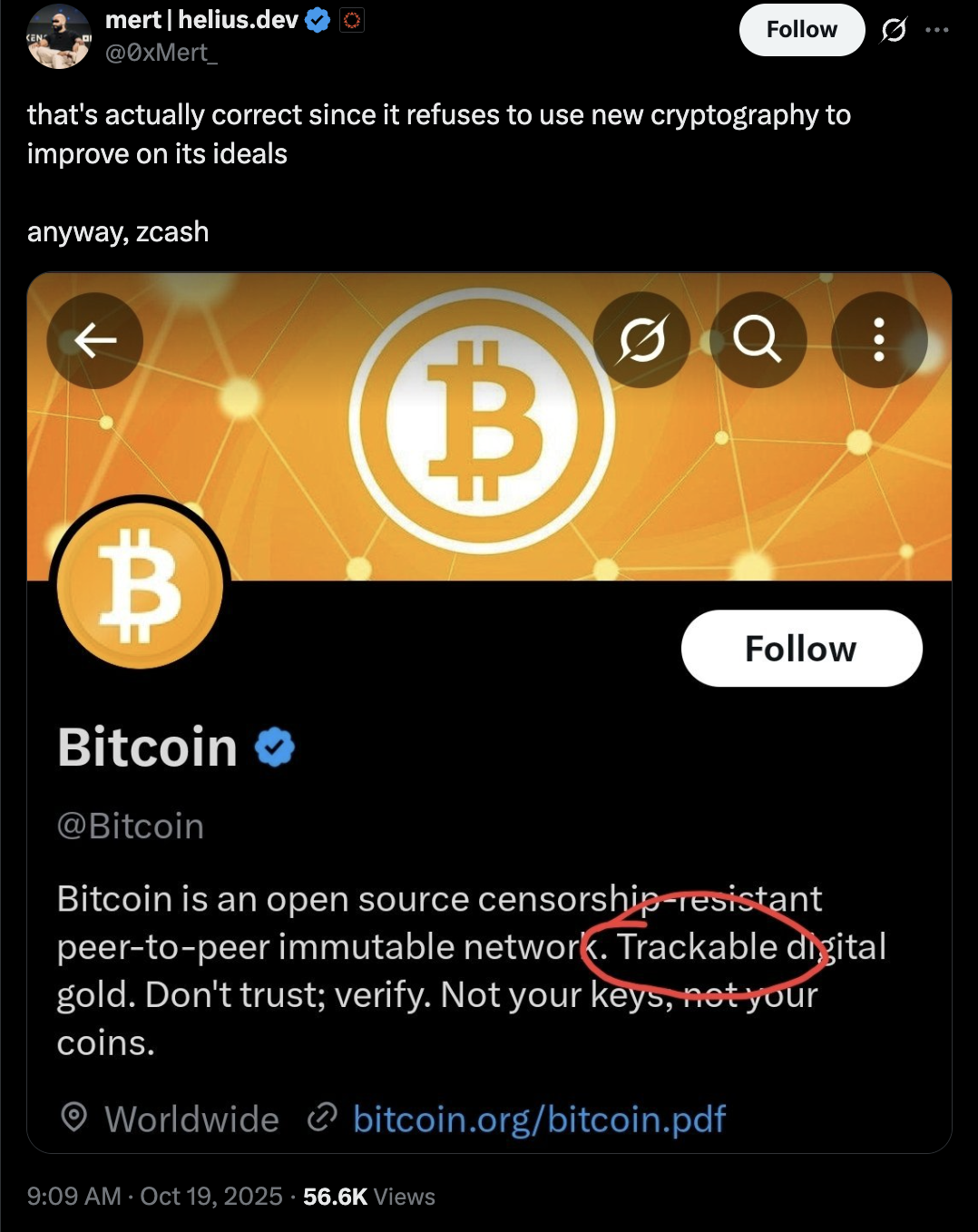

But if you consider the technical aspect, is Bitcoin crypto if it doesn’t build upon its cryptographic nature?

Helius Labs CEO @0xMert notes that Bitcoin actually is money “since it refuses to use new cryptography to improve on its ideals,” implying that Bitcoin’s trackable nature prevents it from being a true “crypto”currency. He’s likely poking fun at Dorsey’s post, but the conversation matters.

Source: 0xMert_ on X

For an asset that never intended for central management, the argument is ongoing.

Dorsey’s lines aren’t just wordplay. They’re defining claims in his eyes. Bitcoin’s hard-cap supply, predictable issuance, and conservative upgrades give it monetary traits that many programmable tokens do not prioritize.

The counterpoints remain real, but if you focus purely on Dorsey’s intent, the takeaway is simple: treat Bitcoin and crypto as different risk categories. Policies surrounding Bitcoin seem to pursue an evolution of traditional finance, while most other digital assets pursue programmable finance and app-layer experimentation.

Whether you agree with Dorsey or not, the smart approach is an analytical one. Evaluate Bitcoin by money’s three functions, and watch how policy evolves around them.

That’s where the “is it money?” question gets answered.

FAQs

Does Bitcoin’s 21 million cap truly make it different from other tokens?

Yes. The cap and the schedule are deeply embedded both in Bitcoin’s code and culture. Could this change? Only with overwhelming voluntary adoption across its userbase.

If Bitcoin became a unit of account, what would merchants actually gain?

More predictable margins on cross-border sales, instant settlement, and reduced chargeback risk.

How would CBDCs or stablecoins impact the “Bitcoin is money” claim?

Stablecoins may dominate day-to-day pricing and payroll, while Bitcoin competes as a reserve asset. It would exist alongside stablecoins, not replace them.

What metrics best track Bitcoin’s progress as “money?”

Merchant volume routed through BTC, payroll/settlement use, and custody behavior. Are users spending or holding the asset?

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Max Moeller is a Chicago‑based writer and video editor passionate about games, tech, and crypto. Whether it’s crafting clear, insightful articles or piecing together engaging video retrospectives, he’s driven by curiosity and takes pride in keeping things human. Since 2017, Max has been published in a variety of notable crypto magazines.

Easy

Easy