The S&P 500’s 12-month P/E ratio has reached its highest point in at least 18 years and is quickly approaching record levels. | Image: Johannes EISELE / AFP

Share

With a forward P/E ratio close to 22, the S&P 500 looks very expensive.

Many reasons seem to justify high market valuations.

But many factors could derail the stock market rally.

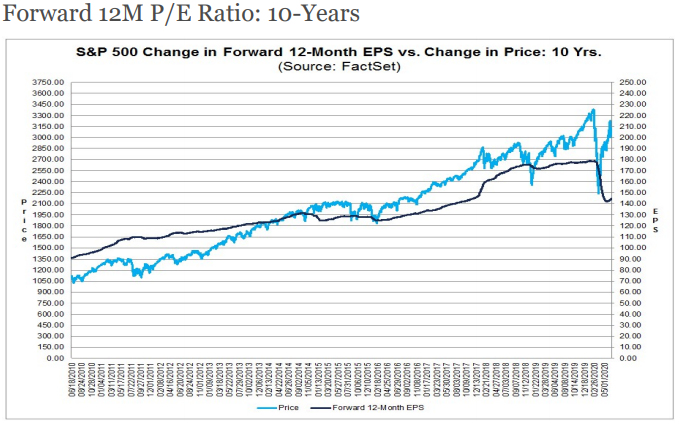

This widely followed measure is now well above its five-year average of 16.9 and its 10-year average of 15.2. The forward P/E hasn’t been that high in at least 18 years and is close to the record 24.4 on March 24, 2000, when the dotcom bubble was about to implode.

The stock market has never been this disconnected from forward earnings in ten years. | Source: FactSet

While the stock market looks incredibly expensive, many reasons can explain this high valuation.

Stock multiples have increased dramatically over the past year from 16.6x to 21.7x today. At the same time, 10-year Treasury yields and investment-grade corporate bond yields have collapsed from 2.1% to 0.7%, and 4.5% to 3.6%. Not surprisingly, investors are making the case that current, elevated stock valuations are justified given the collapse in rates.

Economic numbers are better than expected

Recent economic data have been surprisingly good. Key indicators such as retail sales and payrolls have increased by much more than any economist could have expected last month.

These data suggest the economy is in better shape than previously thought, at least in the short term. Better-than-expected economic numbers have contributed to strengthening investors’ optimism about a sharp recovery, adding fuel to the stock market rally.

Big tech companies have boosted the stock market

Dramatic surges in big-tech stocks like Amazon (NASDAQ:AMZN) and Netflix (NASDAQ:NFLX), which are up more than 40% since the start of the year, have boosted the S&P 500.

Amazon saw a massive surge in online shopping, while Netflix had a record number of new subscriptions as people were confined to their homes.

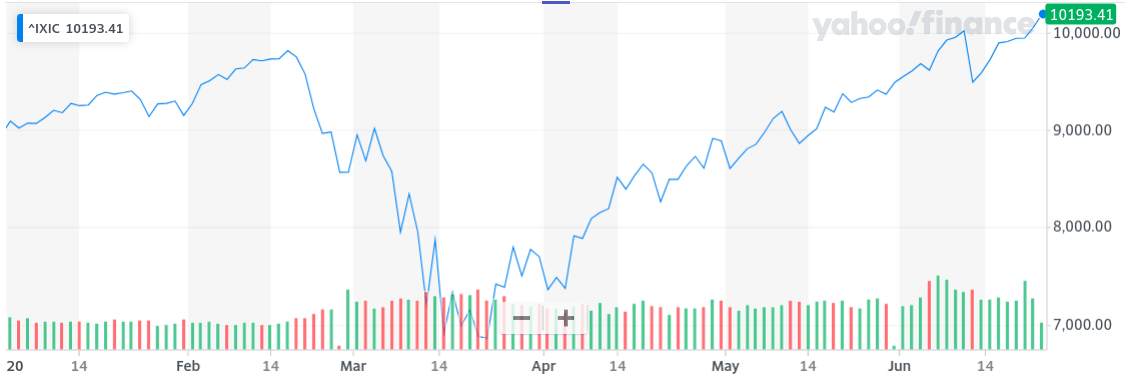

The NASDAQ has surged about 50% from its March 23 low. | Source: Yahoo Finance

The Nasdaq, which is heavily weighted in tech stocks, is up by 12% this year. The S&P 500 and the Dow Jones are still in the red. Tech stocks generally have better prospects for earnings growth, so they have higher P/Es.

The Stock Market Has Many Downside Risks

The stock market seems to be pricing in a fast recovery. But many risks could send equities lower.

John Normand, head of cross-asset fundamental strategy at JPMorgan, has identified six “wildcards” that could derail the stock market rally: a second significant wave; the expiration of temporary fiscal stimulus measures; the end of monetary stimulus; U.S. sanctions against China “before November to increase Trump’s rating or after November on Trump’s re-election;” a U.S. electoral result which leads to increases in corporate tax; and a hard Brexit.

As such, it seems to me that the potential for further gains from things turning out better than expected or valuations continuing to expand doesn’t fully compensate for the risk of decline from events disappointing or multiples contracting. In other words, the fundamental outlook may be positive on balance, but with listed security prices where they are, the odds aren’t in investors’ favor.

So, while high valuations don’t seem to matter now, the stock market won’t stay at those high levels forever. A big bubble is forming and could pop anytime.

Disclaimer: This article represents the author’s opinion and should not be considered investment or trading advice from CCN.com. The author holds no investment position in the above-mentioned companies.

Stephanie has been writing about stocks and financial markets for several years. Based in Canada, she has written for The Motley Fool and Seeking Alpha. She received an MBA in finance and worked for the National Bank of Canada. Check out more of her experience on LinkedIn + and follow her on Twitter. Reach her at stephanie.chateauneuf (at) gmail.com.