Coinbase Global has had ups and downs since its Nasdaq listing in April 2021. The company quickly became the largest publicly traded crypto exchange, catering to retail and institutional investors.

In 2024, Coinbase reported impressive revenues of $6.3 billion, more than double the amount from 2023.

Most of these revenues stemmed from transaction fees ($4 billion), with the remainder coming from subscriptions and services, including offerings like stablecoins and crypto staking.

Coinbase stock dropped by 50% in March only. | Credit: Yahoo! Finance

However, the crypto market has been through a rough patch recently, contributing to a significant decline in Coinbase’s valuation.

As a result, its stock is now trading at a relatively lower price-to-earnings (P/E) ratio of 24 times and an enterprise value to EBITDA (EV/EBITDA) multiple of 11.7 times, based on 2026 earnings estimates.

Yet, as with many crypto companies, Coinbase’s earnings are highly unpredictable, mainly because they depend on the volatile prices and trading volumes of crypto assets.

A key factor in determining the firm’s long-term value will be its ability to diversify its revenue streams, mainly by reducing its dependence on transaction fees tied to the fluctuating market.

While Coinbase has potential for growth, it will need to adapt to make its revenue model more stable.

Coinbase’s Current Value

Coinbase is currently trading at a 24 times price-to-earnings (P/E) ratio and an EV/EBITDA multiple of 11.7 times, based on 2026 earnings estimates. This is a significant drop from a month ago when its share price was nearly 50% higher at $298.

The current multiple is lower than that of key exchanges like Nasdaq, ICE, and CBOE, reflecting the volatility of Coinbase’s profits. However, the company holds $4 billion in net cash and is expected to remain cash-generative.

Consensus estimates around $2 billion annually for the next two years. This steady cash flow makes it a good candidate for estimating its fair value using a discounted cash flow (DCF) model.

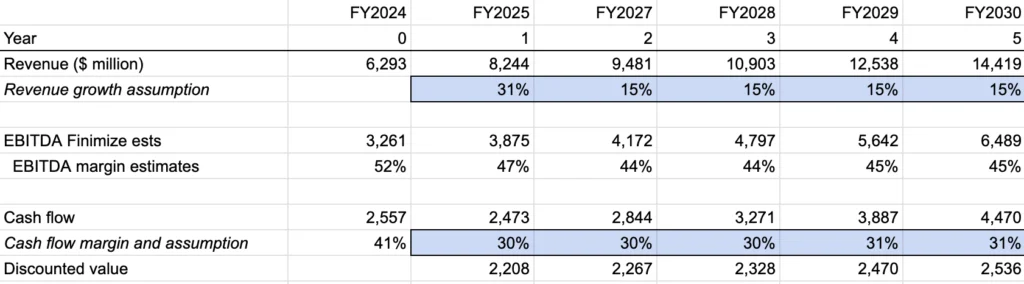

Coinbase bull case based on DCF valuations. | Credit: Finimize

DCF valuations are sensitive to assumptions like revenue growth, volumes, pricing, and competition. Finimize analyst Russell Burns mapped out three potential scenarios for Coinbase’s future: a base case, a bull case, and a bear case.

The base case assumes 29% revenue growth this year, followed by 15% growth through 2026 and slower growth thereafter. This scenario suggests Coinbase’s fair value is around $197, which is near its current trading price.

In the bear case, with stagnant growth and regulatory challenges, fair value could drop to $80. This highlights the importance of the volatile crypto market in determining Coinbase’s valuation.

Is COIN Stock a Buy Opportunity?

Despite these variations, Coinbase’s stock is heavily influenced by crypto prices, particularly Bitcoin. The company’s stock has historically moved in sync with Bitcoin, which will likely continue.

However, due to high expectations, Coinbase’s stock has underperformed this year despite increasing crypto volatility. Factors like lower rewards and custodial fees and missed expectations for inclusion in the S&P 500 have also contributed to its recent struggles.

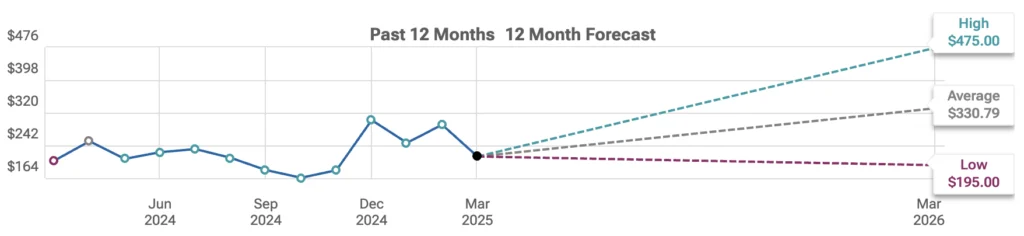

In the best-case scenario, COIN stock could rise by 81% from its current value. | Credit: TipRanks

Over the past three months, 20 Wall Street analysts have provided 12-month price targets for Coinbase Global. The average price target is $330.79, with a high forecast of $475.00 and a low of $195.00. This average target implies an 81% potential increase from the current price of $182.95.

The most recent long-term forecast predicts that Coinbase’s price will reach $200 by mid-2025, followed by $300 by mid-2026. In 2028, the price is expected to rise to $350, $450 in 2029, $500 in 2030, $600 in 2033, and $700 by 2036.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.