Major U.S. banks, including Morgan Stanley, JPMorgan, and Citigroup, reported strong results, driven by investment banking and fixed income. | Credit: Mario Tama/Getty Images

Share

Key Takeaways

Morgan Stanley, Goldman Sachs, Bank of America, Citi, Wells Fargo, and JPMorgan Chase all reported strong fourth-quarter results.

Many banks, such as Bank of America, Citi, and JPMorgan, are optimistic about growth in 2025.

While the U.S. economy remains strong, analysts note concerns over inflationary pressures and geopolitical risks.

As major U.S. banks reported strong quarterly results, the financial sector remains a focal point of investor attention.

Morgan Stanley, Goldman Sachs, Bank of America, Citigroup, Wells Fargo, and JPMorgan Chase all performed impressively.

With robust earnings and revenue figures, these banks have set a positive tone for the year ahead despite inflationary pressures and regulatory uncertainties.

Morgan Stanley reported strong quarterly results, surpassing market expectations due to growth in its investment banking, fixed income, and equity units. Fourth-quarter revenue rose 26% to $16.22 billion, exceeding the $15.03 billion forecast, while net income more than doubled to $3.71 billion. Earnings per share increased to $2.22, beating the $1.70 consensus.

CEO Ted Pick called it an “excellent” quarter, capping one of the firm’s strongest years.

Institutional Securities revenue rose 47% to $7.27 billion, driven by higher investment banking, fixed income, and equity performance. Wealth Management revenue increased 12% to $7.48 billion, while Investment Management revenue grew 12% to $1.64 billion. Return on equity reached 15.2%, with a return on tangible equity of over 20%, up from 6.2% and 8.4% last year.

For 2024, revenue rose 14% to $61.76 billion, net income grew 47% to $13.39 billion, and EPS increased 54% to $7.95. The Common Equity Tier 1 capital ratio stood at 15.9%.

Investment Banking Boosts Goldman Sachs’ Results

Goldman Sachs reported a strong fourth quarter, with net earnings more than doubling to $4.11 billion and revenue up 23% to $13.87 billion.

CEO David Solomon highlighted the firm’s progress in meeting strategic growth targets, with revenues up nearly 50% over five years.

For 2024, net earnings surged 68% to $14.28 billion, while revenue grew 16% to $53.51 billion.

Q4 Global Banking & Markets revenue climbed 33% to $8.48 billion, driven by a 24% rise in investment banking fees, a 35% jump in Fixed Income, Currency & Commodities revenue, and a 32% increase in Equities revenue.

Asset & Wealth Management revenue grew 7.6%, and Platform Solutions saw a 16% revenue increase to $669 million.

Solomon also expressed confidence in the firm’s momentum heading into 2025.

CEO Brian Moynihan highlighted “broad momentum” in 2024, setting the stage for further growth in 2025.

The Consumer Banking division saw steady growth, while Global Wealth & Investment Management posted a 15% Q4 revenue increase, boosted by a 23% rise in asset management fees. Global Markets revenue grew 18%, driven by higher sales and trading income.

BofA expects first-quarter 2025 NII to reach $14.5–$14.6 billion, up from $14.03 billion a year ago, with sequential growth through the year culminating in $15.5–$15.7 billion in the fourth quarter, surpassing $14.36 billion in Q4 2024.

Non-interest expenses are projected to rise 2%–3% from 2024’s $66.81 billion.

Citi Back To Profit

Citigroup reported a Q4 profit of $2.86 billion, reversing a $1.84 billion loss a year earlier due to one-off costs in 2023.

Revenue rose 12% to $19.58 billion, driven by strong performance in Markets, which saw a 36% revenue surge, and Services, which grew 15%.

For 2024, revenue increased 3.4% to $81.14 billion, with net income up 37% to $12.68 billion.

CEO Jane Fraser highlighted record years in Services, Wealth, and U.S. Personal Banking, alongside a completed reorganization and $7 billion returned to shareholders.

Citi enters 2025 with momentum and aims to exceed its 10%-11% 2026 return on tangible common equity target over the long term.

For 2024, net income rose 3% to $19.72 billion, while revenue dipped 0.4% to $82.30 billion, with net interest income falling 9% due to lower rates and deposit changes.

CEO Charlie Scharf highlighted strong fee-based revenue growth, up 15% in Q4, and double-digit gains in trading and investment banking revenue for the year, driven by investments in talent and technology.

Scharf called 2024 a year of “significant progress,” with $25 billion returned to shareholders and improved growth, customer service, and risk controls.

JPMorgan Shares Optimistic View

JPMorgan Chase reported a strong Q4, with net income up 50% to $14.01 billion and revenue rising 11% to $42.77 billion. For 2024, net income increased 18% to $58.47 billion, while revenue grew 12% to $177.56 billion. CEO Jamie Dimon emphasized solid results across all divisions.

Q4 Commercial & Investment Bank revenue jumped 18%, including a 49% rise in investment banking fees and a 20% increase in Markets & Securities Services revenue.

Asset and wealth Management revenue grew 13%, supported by higher management fees and strong net inflows. Consumer and community Bank revenue edged up 1.5% despite a 7% drop in Banking and Wealth Management revenue.

Looking ahead, JPMorgan expects 2025 net interest income of around $94 billion, slightly up from $92.58 billion in 2024, with growth driven by balance sheet expansion despite lower rates.

Dimon noted a resilient U.S. economy but flagged risks from inflationary pressures and geopolitical uncertainties.

What To Expect?

The outlook isn’t all bleak. According to Charles Schwab analysts, while high interest rates persist, they reflect a resilient U.S. economy, with Q4 GDP growth estimated above 3%, following strong Q3 results.

A robust economy traditionally supports banking through increased lending and activity, particularly if pro-business tax and regulatory policies from the new administration ease M&A and foster growth.

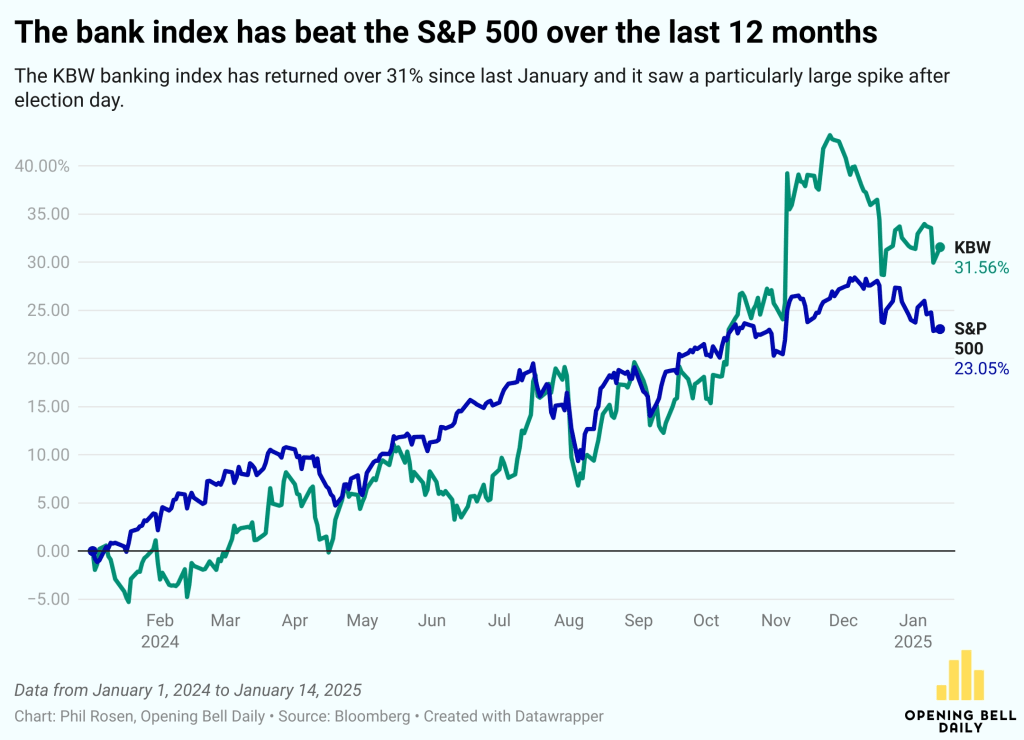

Banks beat the S&P 500 last year. | Credit: Opening Bell Daily

However, uncertainty around new tariff and immigration policies and their inflationary effects has unsettled markets.

After an initial post-election rally, bank stocks, including the Nasdaq Bank Index, declined due to inflation fears and a cautious Fed stance. The BANK index, up 18% year-to-date by Christmas, lagged the S&P 500‘s 25% gain.

“One thing that might spark worries is the timing of policy changes. It’s relatively easy for a president to toughen tariff policy with the stroke of a pen, as Trump often did in his first term and as President Biden continued to the last four years,” analysts said.

“Reducing corporate taxes, though, requires Congress, and December’s budget battle shows that Trump can’t necessarily count on his own party to support every fiscal move. Tariffs are easier to change and less helpful to banks than lower taxes, which take longer to push through.”

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.