If the Fed cuts rates to zero like markets believe it will, that will put the U.S. in the same boat as the rest of the world. | Source: AP Photo / Steven Senne

Share

Markets are pricing in near-100% odds the Federal Reserve will drive interest rate targets down to zero percent next week.

If that happens, the Fed will trap itself between a recession and runaway inflation should prices skyrocket while GDP falls.

That is a horrific situation for the economy to be in: stagflation. It happened in the U.S. before, and it could easily happen again.

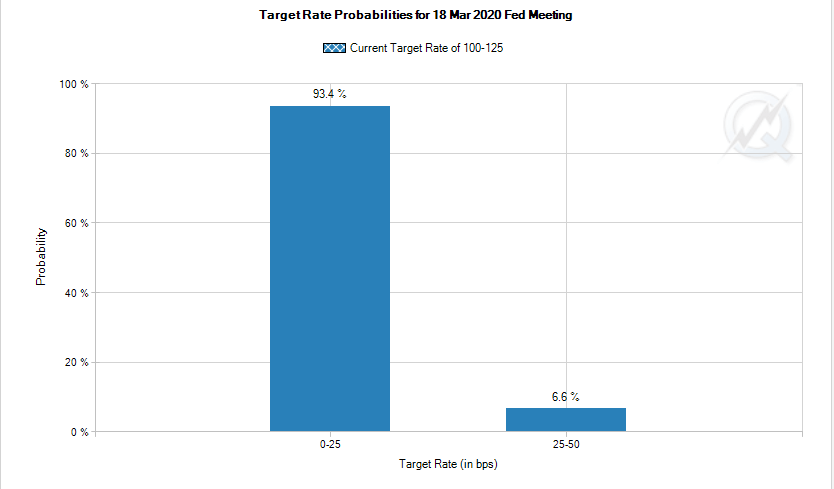

Earlier today, the market’s confidence that the Federal Reserve will slash its benchmark interest rate target to zero by next week temporarily soared to nearly 95%.

But if the Fed cuts interest rates all the way to zero, there’s a real danger of inflation making the financial crisis worse

The market briefly priced in a 93% probability of a massive interest rate cut that would take the Fed’s target down to zero. | Source: CME

Then the Fed won’t be able to raise rates to whip inflation if prices begin to get out of control. That would make the recession worse.

Yet it won’t able to keep rates low either to fight the recession. That will hurt a lot of people with high prices.

Does the Fed Pass Ben Bernanke’s Firepower Test?

A nagging question that has festered since the financial crisis is whether the Federal Reserve could save the U.S. from another recession.

Would the combination of low interest rates and quantitative easing (buying up massive amounts of bonds with money created out of thin air) work again?

Not every economist is so sure.

But former Federal Reserve chair Ben Bernanke argued it could in a January paper published by the Brookings Institution.

In the paper, “The New Tools of Monetary Policy,” Bernanke addresses the fact that interest rates are much lower now than before the 2008 financial crisis.

Ben Bernanke argues the Fed can still achieve the equivalent of 3% in rate reductions through a combination of more quantitative easing and “forward guidance.”

Forward guidance means simply promising to keep rates low in the future to give markets some confidence. And even teasing markets about possible negative interest rates like they currently have in Japan:

The Fed should also consider maintaining constructive ambiguity about the future use of negative short-term rates, both because situations could arise in which negative short-term rates would provide useful policy space.

But if the Fed bails out the economy one more time using Bernanke’s approach, there won’t be any room left to maneuver away from inflation or recession. That would trap the economy in stagflation, which happened in the 1970s to the surprise of all mainstream economists. It was a very dark time for America.

Markets Contributor for CCN living in Nashville, Tennessee. Bachelor of Business Administration from Belmont University in 2009 (majored in Entrepreneurship). Organized Senator Rand Paul's first and second online fundraisers in 2009. Roving editor for the Independent Voter Network since 2013. Email me | Link up with me on LinkedIn | Follow Me on Twitter (followed by: fmr Rep. Ron Paul (R-TX), Sen. Rand Paul (R-KY), fmr NM Gov. Gary Johnson, and Rep. Thomas Massie (R-KY))