The Dow swung 400 points on Thursday because the awful economy could force Trump to prioritize a trade deal with China. | Source: REUTERS / Kevin Lamarque

Share

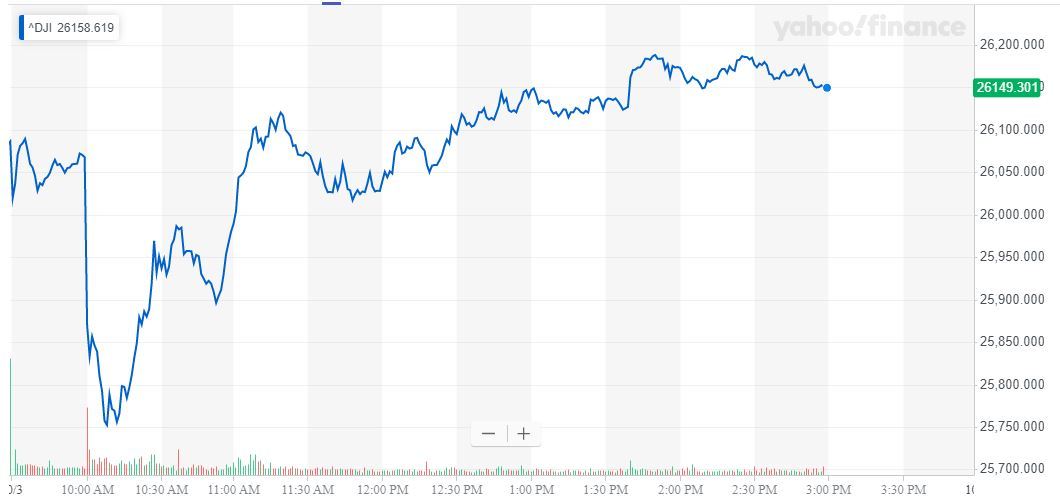

The Dow Jones recovered from a sharp 300-point plunge following the release of a troubling ISM Non-Manufacturing Index report to record a gain of nearly 125 points on Thursday.

Expectations for a Fed rate cut in October rose for the third straight day, helping boost the fragile stock market.

Dow Jones Rallies as Rate Cut Expectations Hit 90%

The Dow Jones Industrial Average closed with gains of 122.42 points or 0.47% to settle at 26,201.04. The Dow had dropped as low as 25,743.46 during the morning session.

The Dow Jones recovered from more bad data on Thursday as rate cut expectations soared and Donald Trump announced a Chinese delegation was coming to the US for trade talks. | Source: Yahoo Finance

The Nasdaq outperformed with a 1.12% rally t0 7,872.27, while the S&P 500 rose 0.8% to 2,910.63.

Commodity markets were mixed again. Oil sold off (-0.61%), but gold (+0.21%) continued to press toward record highs.

The benefits of a weaker US dollar were clearly seen on Thursday. The DXY declined 0.06% as Federal Reserve rate cut expectations for October hit 90%. The weak USD helped reverse daily losses for the Dow after a cavernous decline earlier in the week.

ING: Dismal Economic Data Could Force Trump to Prioritize Trade Deal

More miserable data hung heavy over the US stock market, as another ISM reading (non-manufacturing employment) missed big. Chief International Economist James Knightley believes that risks are rising for a very weak non-farm payrolls figure on Friday, stating:

“This is the worst employment reading since early 2014 and given the ISM manufacturing employment number was already pointing to a sharp fall we are not optimistic for tomorrow’s all-important jobs number. The consensus is still for employment growth of 147,000, but the labour surveys (including yesterday’s ADP report) suggest 100-120k may be more realistic.”

A bad jobs report could be highly detrimental to the Dow Jones, but Knightley believes there may be a silver lining for stock bulls. The dramatic slide in US economic activity may persuade Trump to make a deal with China, or at least prompt much more aggressive easing from the Federal Reserve.

“The latest developments should add a sense of urgency to talks seeking a resolution to the US-China trade dispute and will keep the pressure on the Fed to ease monetary policy further. We continue to look for a December rate cut and a further move in 1Q20, but the risks are increasingly skewed towards more aggressive action.”

Dow Stocks: Financials Tumble, Apple and Microsoft Rise

The Dow 30 was mixed. Falling Treasury yields hit major banking stocks Goldman Sachs (-0.51%) and J.P. Morgan (-0.14%), as the investment banks continue to struggle.

Elsewhere, things were brighter, as global multinational stocks like Nike, Coca-Cola, and McDonald’s enjoyed the profitability boost from a softer US dollar, with the latter two rising more than 1.4%. These companies offer stable P/E ratios, making them attractive during periods of market stress.

Apple stock rose 0.85%, while Microsoft headlined the DJIA’s tech stock rally with an impressive 1.2% bounce. Boeing was also able to recover nearly 1.3% despite some fresh allegations of safety mismanagement among its executives.

Click here for a live Dow Jones Industrial Average chart.

Financial speculator & author living in the hills in Los Angeles. J.D. but very much not a lawyer. Favorite trading books are anything written by Jack Schwager. | Follow Me On Twitter | Email Me