In August, Upbit listings sparked sharp rallies in several small-cap cryptocurrencies, fueling what many now call the “Upbit pump.”

Not long after, FLOCK was also listed on Coinbase’s decentralized exchange (DEX), giving traders the ability to move tokens from Base to Coinbase and trade them directly.

Historically, the Upbit pump has faded quickly. The question now is whether FLOCK can break that pattern and sustain its momentum.

FLOCK Price Analysis

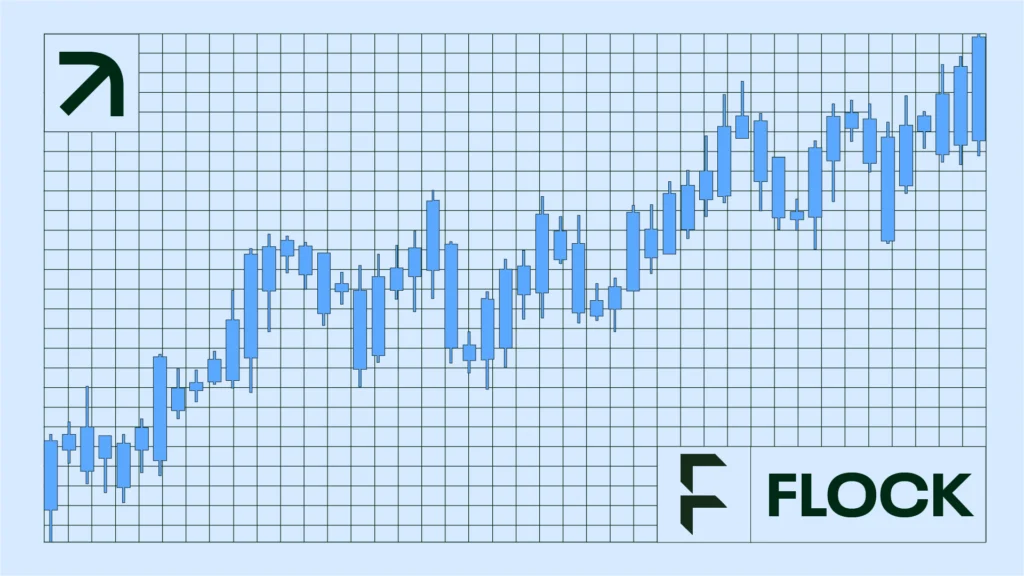

FLOCK has been in a steady uptrend since April 7, forming a series of higher highs and higher lows.

That momentum culminated today with a 120% rally, pushing the token to $0.68, just shy of its all-time high of $0.76.

Get These Top Crypto Casino Offers Now!

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

However, the rally didn’t hold. FLOCK quickly slipped back to $0.50, leaving behind a long upper wick on the daily chart and failing to break through its diagonal resistance trend line.

With resistance at both diagonal and horizontal levels, FLOCK now faces a critical test of whether it can sustain its uptrend or give way to a deeper pullback.

On top of this, there are possible bearish divergences brewing (orange) in the Relative Strength Index (RSI) and Moving Average Convergence/Divergence (MACD).

So, FLOCK may follow the same path as other cryptocurrencies that failed to sustain their Upbit listing pumps, such as Hyperlane, Treehouse, or CYBER.

If a decline follows, FLOCK could return to the closest support at $0.27, reaching the wedge’s support trend line.

Short-Lived Pump

FLOCK pumped today but could not sustain the increase. Similar pumps have been seen in other small cryptocurrencies on the day Upbit listed them.

However, they failed to sustain the increases, creating lower highs since the pump. FLOCK risks going the same way if the technical patterns play out and the price fails to close above $0.70.

A decline to $0.27 could be the next if that happens.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Valdrin Tahiri is a cryptocurrency analyst and reporter at CCN, specializing in technical analysis with a focus on Elliott Wave theory, on-chain metrics, and fundamental research. He brings over seven years of experience in the crypto space as both a trader and writer.

He discovered cryptocurrencies in 2017 while earning his MSc in Financial Markets at the Barcelona School of Economics, which sparked a deep interest in blockchain and market dynamics. Since then, he’s contributed to top crypto outlets like BeInCrypto and CoinGape.

Valdrin also served as Community Manager of BeInCrypto’s Telegram group for three years, helping grow it into one of the largest crypto communities worldwide. His expertise in market structure and price patterns allows him to break down complex trends into clear, actionable insights.

He’s published thousands of articles covering altcoins, Bitcoin cycles, and macro trends.