Real interest rates hold the key to gold's future trajectory. | Image: shutterstock.com

Share

Geopolitics, monetary policy and a slowing economy have all been cited as primary factors behind gold’s bullish breakout in 2019. While these catalysts cannot be discounted, the real reason gold is surging and why it will continue to do so is the trend in real interest rates relative to inflation.

Only by understanding this relationship can one make sense of gold’s rock-solid performance in the face of a rising dollar.

Gold and the U.S. Dollar: A Complicated Relationship

Gold’s bull market has surprised some investors who believe that bullion’s fate is intricately tied to the U.S. dollar. After all, gold futures are priced in greenbacks, so the performance of the world’s favorite reserve currency has a direct impact on foreign demand for precious metals.

This thesis has been put to the test in 2019 as gold and the dollar have risen in lockstep with one another. Gold is in the midst of a bull market – its first in six years – while the U.S. dollar has touched multi-year highs against a basket of competitor currencies.

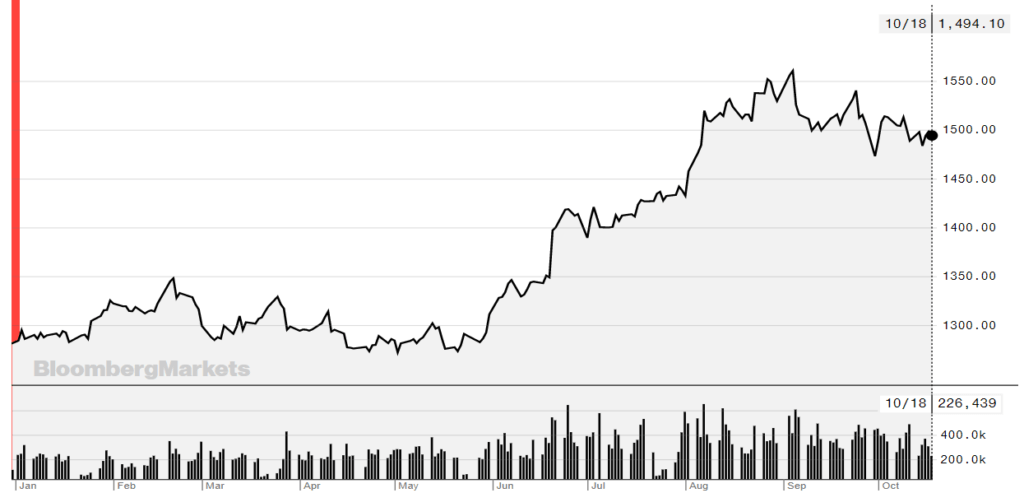

Gold peaked at $1,566.20 a troy ounce in September, its highest in over six years. Year-to-date, the precious metal has returned nearly 17%. | Chart: Bloomberg

The U.S. dollar index (DXY), a measure of the greenback’s value against a basket of six rival currencies, has taken a breather over the past three weeks, but remains in a steady uptrend since the year began. DXY peaked at 99.67 on Sept. 30, the highest since April 2017.

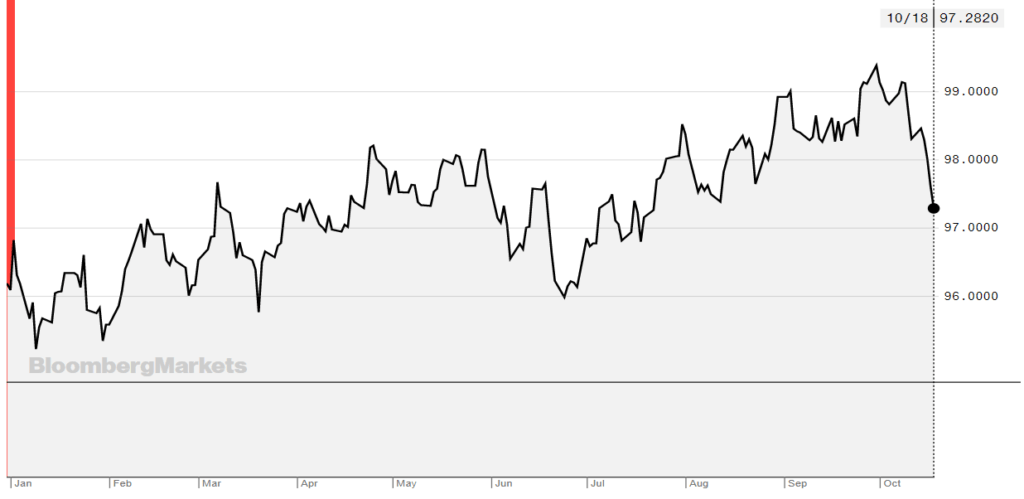

At its peak this year, the DXY dollar index was up 3.6% for 2019. | Chart: Bloomberg

So, while there’s no denying that the dollar influences gold demand, the relationship is much more complicated.

Real Interest Rates are the Key to Understanding Gold

To understand why gold has performed so well this year, one has to go beyond the dollar and look at real interest rates. According to money manager Michael Pento, gold’s primary bull market is set to continue so long as U.S. Treasury yields undershoot inflation.

Pento appeared on a recent segment of the Keiser Report, where he said “the primary factor that determines the price of gold is the level of real interest rates.”

He added:

“Interest rates in a nominal sense could be rising but as long as inflation is rising faster, real rates are going down, gold is in a primary bull market…”

Of course, even nominal interest rates have been falling, and doing so in dramatic fashion. In the last 12 months, the yield on the benchmark 10-year U.S. Treasury note has plunged from around 3.20% to 1.75%. The latter figure excludes the three-year low of 1.441% reached in early September.

Yields have been in perpetual decline for the past year. Yields fall as bond prices rise. | Chart: CNBC

The bond market is coming off a highly volatile third quarter that saw yields on shorter-term debt exceed those of longer-term Treasurys. This so-called inverted yield curve is one of the most reliable bellwethers of recession. An inverted yield curve has predicted the last five recessions with razor point accuracy.

Nominal rates are not only crashing, they’ve fallen way below the most commonly cited inflation metrics. As Pento noted, the U.S. core consumer price index (CPI) reached an annual rate of 2.4% in August, the highest since July 2018. The September rate was unchanged.

Even the core personal consumption expenditure (PCE) index, the Federal Reserve’s preferred and even more flawed measure of inflation, is trending just above the 10-year Treasury yield.

Real Rates are Going Lower

Bond yields have recovered slightly in recent months, but the downtrend is likely to continue as investors look to government debt to shield against many of the aforementioned risks – namely economics, monetary policy and geopolitics. Analysts aren’t convinced that bonds will save investors from the next recession.

Last month, Michael Schumacher of Wells Fargo warned investors not to be bullish on bond yields given their tendency to “overshoot in both directions.” He argued that the same factors that drove bond prices higher in the first place – trade, Brexit, Hong Kong, etc. – haven’t been fully resolved.

Against this backdrop, there’s a good chance that yields are headed even lower. With the Federal Reserve slashing interest rates and conducting new rounds of quantitative easing under a different name, the differential between real interest rates and inflation is unlikely to narrow significantly.

President Trump’s recently announced trade truce with China has quelled some of the market’s risk aversion, sending stock prices higher and bond prices lower. But the pressure on the Trump administration is immense.

Global growth is faltering, and US GDP growth has shrunk from over 4% last year, to under 2% in Q3, according to the Atlanta Fed. The most important part of the yield curve remains inverted. There is illiquidity in the Repo market. D.C. is in utter turmoil and annual deficits have vaulted over the trillion dollar mark. The Q3 earnings report card is about to arrive, and it will receive an “F.” And global central banks are virtually out of ammo. Meanwhile, the stock market sits at all-time record high valuations.

Financial Editor of CCN.com, Sam Bourgi has spent the past decade focused on economics, markets, and cryptocurrencies. His work has been featured in and cited by some of the world's leading newscasts, including Barron's, CBOE, Yahoo Finance, and Forbes. Sam is based in Ontario, Canada and can be contacted at [email protected] or at LinkedIn.