If everything goes right for the Elon Musk-led Tesla, its share price could be worth $15,000 in just a few years, according to ARK Invest. That’s an absurd target, even under the most optimistic scenarios. | Image: REUTERS / Hannibal Hanschke

Share

ARK Invest holds a 25% probability that Tesla will hit $15,000 in 2024.

The investment fund assumes Tesla’s largest revenue driver in 2024 will be robotaxis.

The Elon Musk-led firm stands to gain from an EV boom. But traditional car makers are catching up.

Tesla’s (NASDAQ:TSLA) market cap now stands at nearly $120 billion, exceeding that of fellow U.S. automakers General Motors (NYSE:GM) and Ford (NYSE:F). The best is yet to come, according to ARK Investment Management, which has assigned an astronomical price target for the electric vehicle manufacturer.

A bull case presented by the thematic investment fund values Tesla shares at $15,000 by 2024 [ARK Invest]. That would give Tesla a market cap of $2.7 trillion!

While the quadrupling of Tesla’s share price in less than a year could be blamed for over-optimism, it’s no reason to lose sight of reality.

Here are three reasons why Tesla investors shouldn’t get their hopes up for such lofty valuations.

Tesla autonomous taxi network is not a sure thing

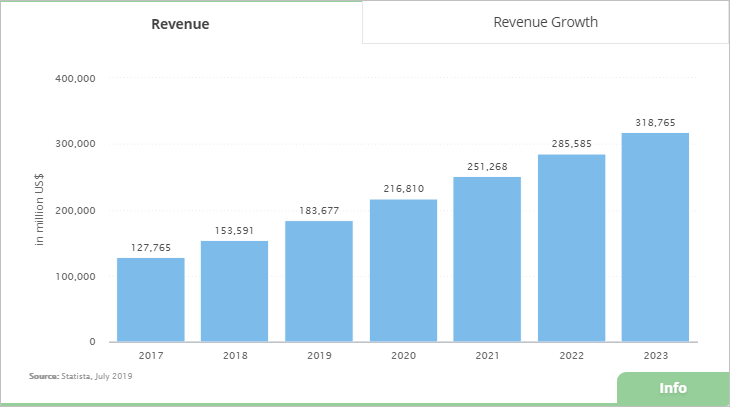

ARK’s bull case hinges on Tesla introducing robotaxis – basically autonomous Tesla vehicles operating as taxis. From the autonomous cab network, ARK expects Tesla to generate $351 billion in revenues in 2024. Even assuming that the fully-self driving cars will be road-legal and operational by 2024, that’s a generous figure. By 2023 revenues from the ride-hailing sector are estimated to reach $318 billion at a compounded annual growth rate of 13.7% [Statista].

For Tesla to reach such figures, it would mean completely vanquishing all other competitors in ride-hailing.

Other hurdles await Tesla’s self-driving vision too. For one, Tesla’s self-driving technology is not ready for prime time. The need for human intervention remains apparent, not to mention the regulatory hurdles of fully self-driving cars.

Additionally, Tesla CEO Elon Musk has himself walked back an assertion that the company would be launching a million robotaxis this year. Instead, Musk last month stated that Tesla will have a million “robotaxi-capable” vehicles on the road this year. That’s a big difference.

Legacy carmakers are fighting back

In projecting a stock price of $15,000, ARK assumes that the electric vehicle firm will retain its market share of around 20%. That’s unlikely as traditional car makers with more reach and scale launch their own EVs. Already, General Motors, Ford, Volkswagen and other manufacturers have proven that the excitement over electric vehicles is not limited to Tesla cars alone.

General Motors is also expected to launch an electric version of the Hummer, which should trigger similar excitement among die-hard fans.

There are other U.S. EV firms coming up, such as Rivian. So while Tesla’s sales could rise, the market share will be under severe strain in the face of new and established competition.

Tesla’s gross margins set to rise

For Tesla to hit $15,000 a share, ARK expects the firm’s gross margins to reach 40%, double the Q4 2019 figure of 20.9%. The forecast is based on Wright’s Law, which predicts declines in costs as a technology matures.

While the law may hold true, it ignores all sorts of unexpected scenarios. With increased competition, Tesla will be forced to lower prices. Growing competition could also force Tesla to change tact and start spending on marketing. It could also force the EV manufacturer to invest more in after-sales services and open stores in less-profitable places. All this will eat into the margins.

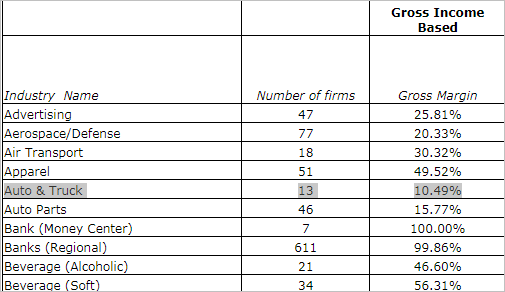

Additionally, Tesla doesn’t operate in a vacuum. It will soon find itself having to align its gross margins with the rest of the car sector. Currently, gross margins among car manufacturers stand at just under 11% [NYU Stern School of Business].

To be fair, ARK has also presented another extreme scenario where the share price goes to zero after Tesla goes bankrupt. The most likely outcome probably lies somewhere in between.

Disclaimer: The opinions expressed in this article do not necessarily reflect the views of CCN.com.