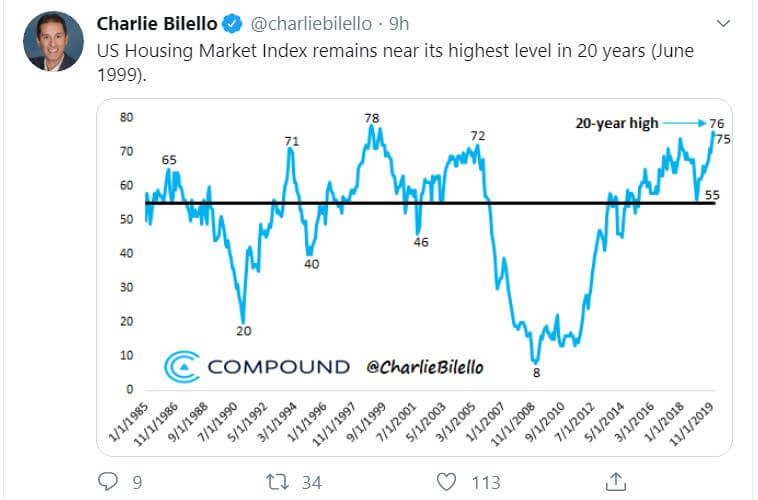

U.S Housing Market Looks Strong As Mortgage Applications Spike

It isn’t surprising that home prices remain strong when you consider that supply continues to dwindle. Baby boomers are slow to sell, and millennials are desperate to buy. Throw into this mix that the U.S. economy continues to drive decent wage growth in the low inflation, low-interest-rate environment, and young people are making the leap in great numbers.

It’s quite common to hear people talk about waiting for house prices to collapse so they can afford a home. The problem is that so many young people are in that same boat. When prices start to come down slightly, there is a feeding frenzy, and the limited supply is going to dry up even further.

It’s frightening to think of a scenario where a U.S. housing market crash could materialize with a whole generation on the sidelines clamoring for the perceived stability of homeownership.

If you take this point of view, then all of the positive housing index readings make the situation look more ominous than encouraging. If the majority of Millennials can’t buy homes, they will desperately wait to inherit, and in that wealth transfer increased sales could mix with lessening demand as they dump their parents’ homes en-masse – an obvious trigger for a housing market crash.

Millennials Desperately Want To Get On The Housing Ladder

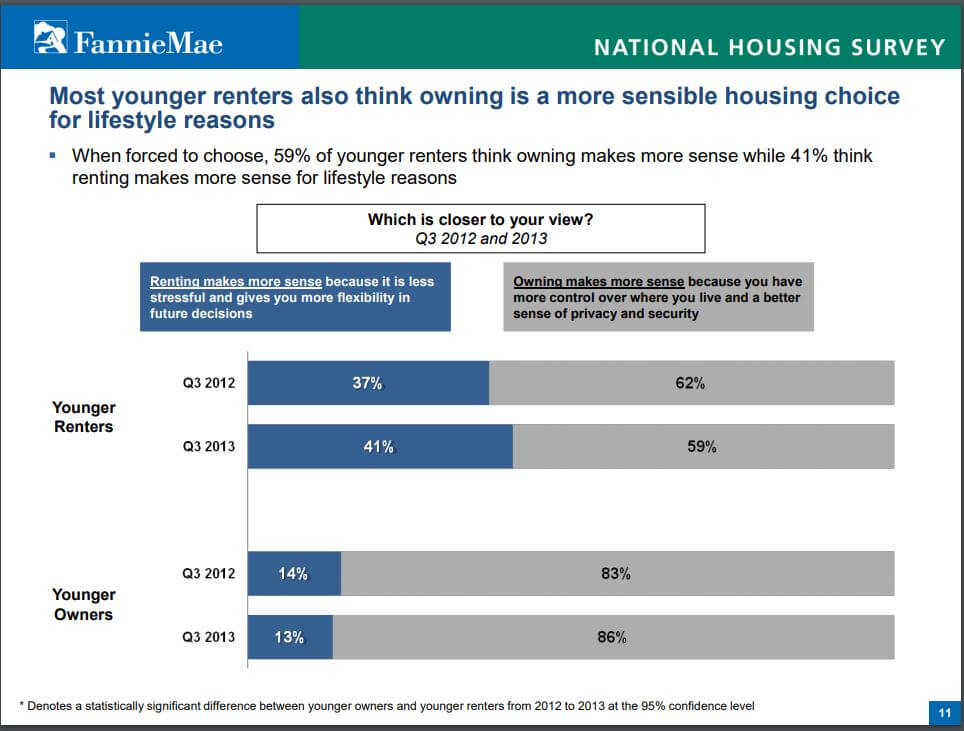

What’s most interesting given the perception about this free-spirited, supposedly fiscally unsavvy generation is that they still desire to own a home. That’s according to a Fannie Mae study more than five years ago. This information makes the spike in mortgage applications seem totally predictable.

Fannie Mae predicted future housing demand with a study that showed most millennials believe homeownership is a preferred lifestyle to renting. | Source- Fannie Mae- National Housing Survey

The reality is that higher prices and lower relative wages have slowed, not deterred, millennials in their quest.

A large portion of young people’s desperation to buy comes from the pressure from their parents and grandparents who grew up expecting, not dreaming, to own their own home. The problem is that globalization and decades of stagnant wage growth have made this much more difficult, even for the generation that revels in thrift.

A Housing Market Crash Looks Likely, Just Not Right Now

Ultimately, the U.S. Housing Market is two things, both healthy and a crisis, depending on whether you own a home, or cannot afford one. One thing remains clear: While economic conditions remain steady, millennials are going to buy any dips aggressively given their desire to own a home. Loose monetary policy helps, too.

Longer-term, the economic outlook darkens considerably as what are the young people buying their houses with? Their retirement savings.

Disclaimer: The opinions expressed in this article do not necessarily reflect the views of CCN.com.

Financial speculator & author living in the hills in Los Angeles. J.D. but very much not a lawyer. Favorite trading books are anything written by Jack Schwager. | Follow Me On Twitter | Email Me