Crypto tax can be complex. Photo by Kelly Sikkema on Unsplash

Share

Key Takeaways

In 2023, the OECD introduced a new framework for crypto asset tax reporting.

As countries around the world implement the new standards, crypto firms’ tax reporting burden is set to increase.

This creates a challenge for brokers and other intermediaries which will have to collect and organize huge volumes of data.

In 2023, the Organization for Economic Cooperation and Development (OECD) introduced a new framework for crypto asset tax reporting designed to enable better information-sharing between countries. As national authorities act to enforce the new standards by 2027, crypto brokers around the world have found that their reporting obligations are increasing.

According to PwC’s 2024 Crypto Tax Report, the OECD guidelines could incur billions of dollars of additional costs annually as tax reporting requirements expand to a greater range of transactions.

OECD Crypto Tax Rules

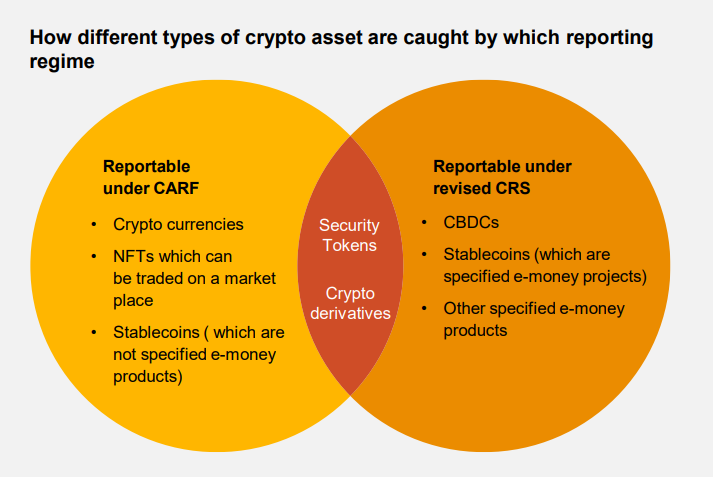

The OECD’s crypto asset reporting framework (CARF) requires exchanges, brokers, custodians and wallet providers to collect and report to local tax authorities information concerning the identity and transactions of their users.

The framework covers cryptocurrencies, tokenized real-world assets, stablecoins and some NFTs. Reportable transactions include crypto-for-crypto swaps, fiat on- and off-ramps, and transactions where crypto is used to pay for goods or services valued at more than $50,000.

Source: PwC Global Crypto Tax Report 2024

Jurisdictions that have already moved to implement the new rules include the US, where the Treasury proposed regulations last August, and the EU, where the council adopted a directive amending the bloc’s tax code in October.

In both cases, the new reporting requirements are expected to come into force by the 2025/2026 tax year.

Crypto Firms Brace for Increased Reporting Burden

With crypto firms reporting burden set to increase significantly, the PwC report notes that

“the volume of data that will need to be gathered, organized and reported can only be managed via new technology solutions.”

Given the digital and often on-chain nature of much of the information that needs to be reported, there are significant opportunities for automation.

[OUT NOW] New global #tax transparency framework to provide for the reporting and exchange of information with respect to #crypto-assets.

For both individual and corporate taxpayers, platforms like Coinledger and Bitwave promise to optimize the process of crypto tax management by integrating with different wallets to help calculate tax bills.

However, things get even more complicated when it comes to international transactions.

Cross-Border Complexity

Although the CARF framework is intended to make it easier to share information across borders, it can’t erase the friction between tax regimes.

Consider, for example, 2 neighboring countries that have very different tax systems: France and Belgium.

In France, investors must pay capital gains tax on any profit they make selling crypto. On the other hand, Belgium doesn’t distinguish between capital gains and income, taxing each person’s earnings from employment or investments together.

Traditionally, capital gains tax is paid in the country where a sale occurs while income tax is paid in your country of residence.

So what about someone who resides in Belgium but sells crypto through a French exchange? In theory, they should be able to pay capital gains tax in France and then deduct that from their Belgian liability to avoid double taxation. But this requires complex reporting in both jurisdictions.

The Crypto Tax Gap

Cryptocurrencies like Bitcoin are borderless by nature. But exchanges, brokers and other intermediaries aren’t, and when the ultimate liquid asset meets rigid tax regimes, it often slips through the gaps.

Calculating the crypto tax gap is difficult, but by most accounts, evasion is fairly commonplace

Consider, for example, that although only 1% of 2020 US tax returns declared cryptocurrency sales, yet surveys suggest that between 10% and 20% of the population own digital assets.

This discrepancy is one of the primary motivations for the OECD’s new reporting guidelines, which will help tax authorities keep better track of who owns what.

In the modern world of Bitcoin ETFs and institutional crypto adoption, off-the-books transactions and casual underreporting will likely become less prevalent, at least as a proportion of the overall market.

After all, from the perspective of tax revenues, large institutions and massive crypto funds are much more important than retail investors dipping their toes in DeFi.

James Morales is CCN’s blockchain and crypto policy reporter. He has been working in the news media since 2020, writing about topics such as payments, banking and financial technology. These days, he likes to explore the latest blockchain innovations and the evolving landscape of global crypto regulation.

With an educational background in social anthropology and media studies, James uses his platform as a journalist to explore how new technologies work, why they matter and how they might shape our future.