The Reserve Bank of Australia is exploring the potential benefits of a wholesale central bank digital currency (CBDC) through Project Acacia. l Credit: Brendon Thorne/Getty Images

Share

Key Takeaways

The Reserve Bank of Australia (RBA) is prioritizing the development of a wholesale CBDC over a retail version.

The project aims to explore the benefits of tokenizing assets and using a CBDC for their settlement.

The RBA estimates significant transaction cost savings from tokenizing Australian financial markets.

The Reserve Bank of Australia (RBA) is exploring the potential benefits of a wholesale central bank digital currency (CBDC). This shift in focus comes after the RBA determined that a retail CBDC would offer limited advantages to the Australian public.

The RBA believes that a wholesale CBDC can significantly improve the efficiency, transparency, and resilience of wholesale markets.

By focusing on wholesale CBDCs, the RBA aims to reduce counterparty and operational risks, enhance transparency and auditability, and lower costs associated with intermediaries and compliance.

What’s Project Acacia?

The Reserve Bank of Australia is set to embark on a three-year project called Project Acacia to explore the potential benefits of a wholesale central bank digital currency.

The RBA and DFCRC’s Project Acacia aims to explore how digital money and infrastructure can facilitate the settlement of tokenized assets in wholesale markets.

Building on their 2023 CBDC pilot, the project seeks to understand the potential benefits of tokenized assets and a CBDC for atomic settlement.

The pilot explored tokenizing various assets, including traditional securities and emerging classes like carbon credits.

“Globally, there’s significant interest in asset tokenization, with banks and firms launching DLT platforms and issuing billions in tokenized bonds. Tokenization can benefit markets by reducing risks, costs, and increasing liquidity,” the Australian central bank said.

Assistant Governor Brad Jones Jones estimates potential transaction cost savings from tokenizing Australian financial markets in the range of $1-4 billion per year.

The project also focuses on the role of digital money in facilitating tokenized asset settlement.

The RBA and DFCRC aim to determine whether a wholesale CBDC is necessary. Or if existing infrastructure can support settlement using ESA balances or privately issued tokenized money. The project is expected to conclude in the second half of 2025.

“By committing to a forward work plan covering the next three years, the RBA and Treasury will work closely together in progressing understanding of key policy issues related to retail CBDC. And support any future deliberation on related issues by the Australian Government,” the RBA said.

Improving Cross-Border Payments

The central bank added that CBDCs can potentially improve domestic and cross-border payments.

It argued that the current correspondent banking system for cross-border payments is complex and inefficient. CBDCs could streamline this process by reducing reliance on intermediaries and simplifying settlement.

The RBA participated in Project Dunbar, which explored a multi-CBDC platform using DLT for cross-border payments.

While the project demonstrated the feasibility and benefits of such a platform, it also highlighted challenges in managing a shared platform across multiple jurisdictions.

Other projects, like mBridge and Project Agorá, are also exploring multi-CBDC solutions. However, the BIS assesses that these solutions are unlikely to arrive in the near term.

In the meantime, efforts to improve existing cross-border payment processes and infrastructures, such as harmonizing standards and interlinking fast payment systems, are more likely to yield near-term progress. The RBA has been involved in several of these initiatives, including Project Mandala.

Delaying Retail Version

The RBA has abandoned plans for a retail CBDC in favor of a wholesale CBDC. The RBA’s research suggests that a wholesale CBDC could offer significant benefits, including reduced risks, improved transparency, and lower costs for financial institutions and their customers.

Governor Jones said: “First, and with the strong endorsement of the Payments System Board, I can confirm that the RBA is making a strategic commitment to prioritise its work agenda on wholesale digital money and infrastructure – including wholesale CBDC – rather than retail CBDC. At the present time, we assess the benefits to the economy as more promising, and the challenges less problematic, for a wholesale CBDC compared to a retail version.”

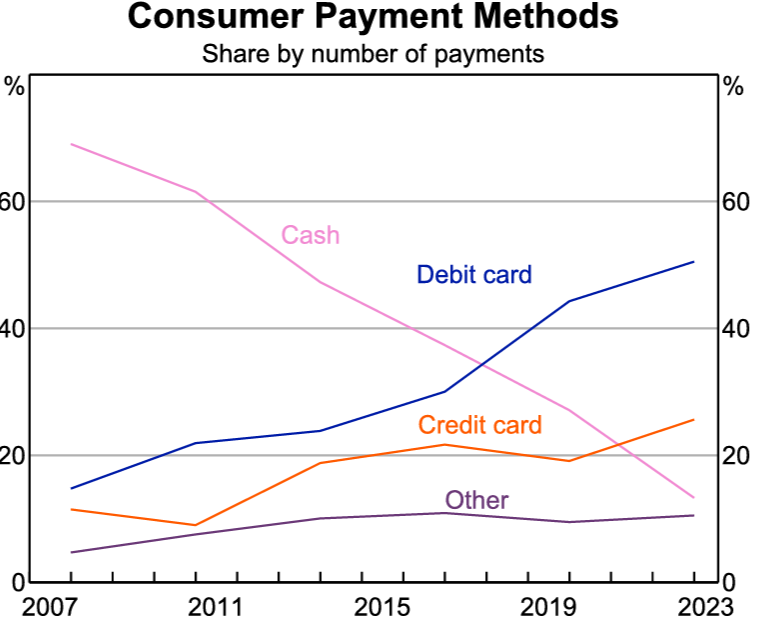

Consumer payment methods in Australia. l Credit: Reserve Bank of Australia

Governor Jones added that, unlike a retail CBDC that would be issued for use among the public, a wholesale CBDC would represent more an evolution than a revolution in the Australian monetary arrangements.

“It also recognises the stabilising role of central bank money in the settlement of wholesale market transactions, particularly in markets that are (or could be) systemically important – a point emphasized in international standards.”

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.