Billon, a former Polish based now London-headquartered start-up, has raised $2 million to “further investment in its UK and Polish partnerships,” according to a press release.

Somewhat uniquely, the start-up claims they have implemented a “proprietary blockchain technology,” which turns fiat into digital cash. They state they are “interconnected to 2 banks, 6,000 ATMs and 18,000 kiosks through partnerships in Poland.”

We found it difficult to learn more about its underlying infrastructure. There is no code to analyze, no technical whitepaper, any public information appears very general, and in reply to our specific questions we received no more than was publicly available:

“Billon developed its own proprietary payments platform, optimized for peer-to-peer mobile transfer and for automated and seamless compliance and control.”

There appears to be at least three servers from any information we can gather. One at each of the two partnering banks and another at Billon. Banks initially convert fiat into digital tokens at a 1:1 ratio, presumably through special nodes, and, as Billon users can withdraw at a cash machine or send tokens to a normal bank account, the partnering banks can also, presumably, convert the tokens back to fiat.

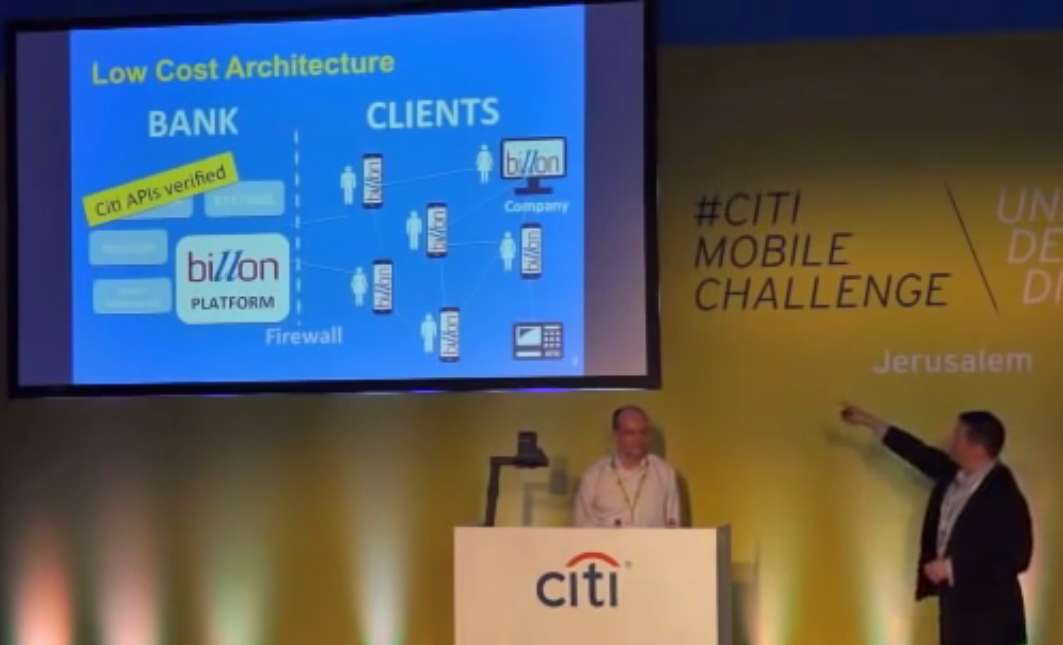

Billon, Presented at the Citi Mobile Challenge

Then, according to a presentation at Citi Mobile Challenge where Billion was awarded the winning prize, David Putts, Billon’s Chairman and Chief Commercial Officer, states they “have a distributed network architecture that sits on mobile phones and PCs, completely scalable, as the customer base grows, you still have one server.”

There clearly are at least three servers (or, more correctly, nodes), one at each bank and one at Billon. What Putts may have meant is that there is one validating server which, presumably, ensures there are no double spends. Everyone else then connects to that node through SPV wallets. As such, it appears we have to trust Billon, it’s administrator, or the software, with no verification. We further have to trust the two partnering banks, or, more specifically, the operator of their node.

The start-up claims they can provide a bank account at a cost of $1, as opposed to, according to Billon, an average cost of $100 for traditional banks, but where such savings come from is not clear. They claim to be fully regulated by two European authorities and are taking part in FCA’s sandbox. As such, accounts are AML/KYC verified. The partnering banks require special and presumably manual administrators who constantly must convert back and forth, with increased use increasing the number of such administrators, and costs. In between, transactions presumably do not require a clearing house, but why an intermediary would not be required to ensure the 1:1 conversion has actually occurred and someone did not just give himself $1 billion, or to ensure there are no double spends unless there are at least ten nodes operated by ten different owners, is not clear.

The Blockchain Paradox

The transformation of fiat into digital, shares many of the same qualities as the transformation of land registry entries, IDs, highly valuable assets, birth certificates, and other records, into blockchain entries. There are two main problems. Firstly, the creation of the entry or the issuing of tokens and, secondly, the transfer of ownership of records or, for money, their conversion back to fiat.

It is easy to have distributed software which holds the same information making it difficult, if at all possible, to change records, but it is non-trivial to ensure that the issuing, creation, or transfer of ownership is correct, to begin with. How these entry bottlenecks can be improved is difficult to see for necessarily there must be an individual who enters ownership details and changes them where required. That individual, or a hacker, or a mistake, can also abuse the exact same entry rights, making necessary the overseeing intermediaries, such as clearinghouses or centralized land registries.

For fiat transformation, the same bottleneck applies as the creation and issuing of tokens needs third party oversight and many layers to ensure someone did not award themselves or their family and friends one trillion dollars. However, once the validity of the issuing and destruction of tokens is established through traditional means, nodes, distributed in many banks, institutions, individuals or other entities, (at the very least ten of them, but preferably 100 or more,) can allow the transfers system to operate very much automatically.

In many ways, therefore, the current system can be incrementally improved, but a centralized approach, just as a decentralized approach, has its advantages and disadvantages.

Public Blockchains vs Private Transformation of Money

Public blockchains have two main benefits. They lack any bottleneck regarding the creation of money as they have no single individual or many such individuals that can simply create tokens with the software alone dictating. Allowing them to require no trust of any administrator with the process, combined with many nodes validating and ensuring any creation or transfer follows the rules, fully automated.

Verification and security are other added benefits as all are open source. Anyone can see if any rule is breached with any bugs highly valuable to exploit, ensuring they are used at the first opportunity as someone else might exploit them first.

Private blockchains have the benefit of security through obscurity. You need to find the code first, then exploit it, which limits the pool. When it comes to money, they have the added benefit, from some perspective, of simply upgrading current fiat, reducing barriers to adoption.

Both of them can share many similarities. Transfers, for example, would not need intermediaries after creation for transformed fiat. In both cases, one could easily incorporate a just one-click button for online commerce. As they both would be, in some ways, programmable money, there could be more complex innovation applicable to both.

If we think more futuristically, even where access to transformed fiat is no different than opening a bank account, one can imagine an individual asking a bank to provide a machine with a smart contract address, allowing machines to exchange value. DAO like entities could also be created, although by centralized administrators who would need to approve and create the DAO smart contract.

Therefore, the competition between public blockchains and transformed fiat is about to begin. They both have their advantages and disadvantages, thus may co-exist, but, eventually, one will become irrelevant. That is why so many vigorously argued for bitcoin to move faster, but, at this point, which will prevail is difficult to predict.