Normally, 10-year U.S. Treasuries set the tone for 30-year mortgages, but the spread between them is now 2.9 percentage points, close to levels last seen in late 2008 and early 2009. | Source: AP Photo / Steve Helber

Share

In a spooky financial crisis echo, the gap between mortgage rates and Treasury bond yields is at its widest mark since 2009.

Mortgage rates are low, but they should be even lower by historical standards.

Here’s why the housing market will continue to recover anyway.

Treasury bond yields and mortgage rates typically move in tandem, but the gap between them has ballooned to its widest point since 2009. That’s an eerie parallel to the Great Recession. But don’t expect it to stop the housing market from snapping back quickly.

Mortgage Rates Are Doing Something the Housing Market Hasn’t Seen Since 2009

The coronavirus pandemic has damaged the global economy. This has driven a massive amount of investment capital toward the relative safety of U.S. Treasuries, whose yields fall as prices rise.

The interest rate on the 30-year fixed-rate mortgage tends to move up and down in tandem with these yields. And these yields are currently near their lowest levels in history.

While mortgage rates have fallen, there is a large spread between the cost of borrowing from the U.S. government and the rates offered to homeowners.

The spread between mortgage rates and benchmark Treasuries is at its widest since 2009. | Source: Bloomberg

Despite the wide gap between mortgage rates and Treasury yields, house-hunters may not care. With rates as low as they already are, it’s unlikely this particular cost is pricing too many would-be buyers out of the market.

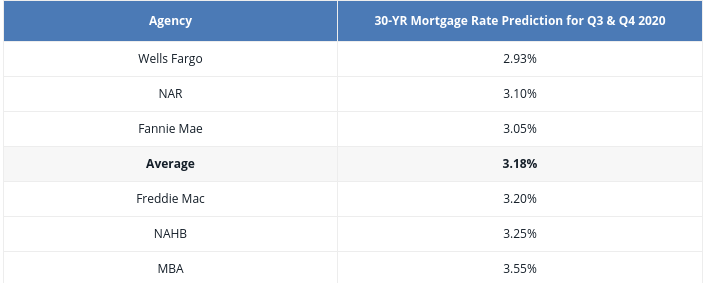

Plus, the gap could begin to close soon. Analysts believe mortgage rates will continue to drop and could go lower than 3% through 2021.

The average 30-year mortgage rate prediction for Q3 and Q4 2020 is 3.18%. | Source: The Mortgage Reports

There’s a significantly lower demand for loans, declining inflation, and 10-year Treasury Notes approaching zero. These factors will cause rates to decrease. The economy has taken its hardest hit in decades. And the prognosis for a significant recovery post-COVID-19 is weak.

If the average 30-year rate breaks records and falls below 3%, it will create a solid buying and refinancing environment throughout the year. Before 2020, the lowest rate recorded for a 30-year fixed-rate mortgage was 3.31%, reached at the end of 2012.

Real estate should become attractive again when the virus panic subsides and more states restart their economies. Lower mortgage rates will likely encourage people to buy a home or refinance. But whether or not they do may depend on the economy.

Stephanie has been writing about stocks and financial markets for several years. Based in Canada, she has written for The Motley Fool and Seeking Alpha. She received an MBA in finance and worked for the National Bank of Canada. Check out more of her experience on LinkedIn + and follow her on Twitter. Reach her at stephanie.chateauneuf (at) gmail.com.